10Yr Yield Slips Below 4%

- Questions continue to swirl regarding the ultimate impact of AI on the economy, and that has kept equities from breaking to new highs. Another blowout earnings report from Nvidia wasn’t enough to rekindle animal spirits. Those risk asset struggles continue to aid Treasuries and with geo-political risk looming, there are more Treasury bids waiting in the wings, and we’re seeing that this morning as 10yr yields slip below 4% in overnight trading. Next week brings a slew of first-tier February reports topped by the Friday jobs report, so data will provide some relief from non-financial factors. Currently, the 10yr is yielding 3.99%, down 3bps, while the 2yr is yielding 3.41%, down 3bps on the day.

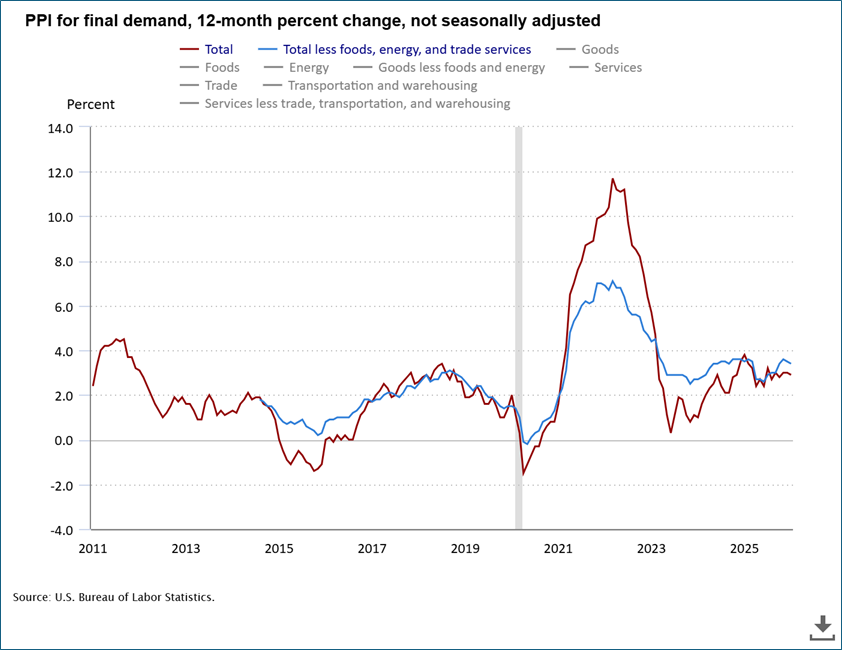

- The gap in missing economic reports is slowly being filled, and this morning we finally received the January PPI Report. Since we’ve had the January CPI numbers in hand for more than a week some of the luster of today’s release is smudged but it provides the last pieces of data needed for the January PCE report that is expected to be released on March 13. That report, important given it’s the Fed’s preferred inflation measure, will arrive two days after February CPI, once again dimming some of its potential impact.

- In any event, Final Demand PPI for January increased 0.5% vs. 0.4% prior month and 0.3% expected. The YoY rate decreased from 3.0% to 2.9%. Consensus expectations were 2.6%. Final Demand PPI ex Food, Energy and Trade increased 0.3% vs. 0.4% prior month and 0.3% expected. The YoY rate dipped to 3.4%, just under the 3.5% expectation and December result. Service costs rose 0.8% with 80% of that coming from wider margins on trade services, which probably doesn’t bode well for the service components feeding into PCE. Goods prices, however, fell 0.3%.

- Looking ahead to PCE, coming off a pair of 0.4% monthly PCE prints (overall and core) in December, expectations are 0.3% for January, pending updates following this PPI release. With a 0.31% and 0.45% monthly print rolling off in January and February any new monthly print under those amounts will lead to a drop YoY PCE. After February, the comps become a string of 0.1% and 0.2% monthly prints so YoY improvement after February through year end will be more challenging. That will play into the inflation hawks’ resistance to cut until inflation trends closer to 2.0%.

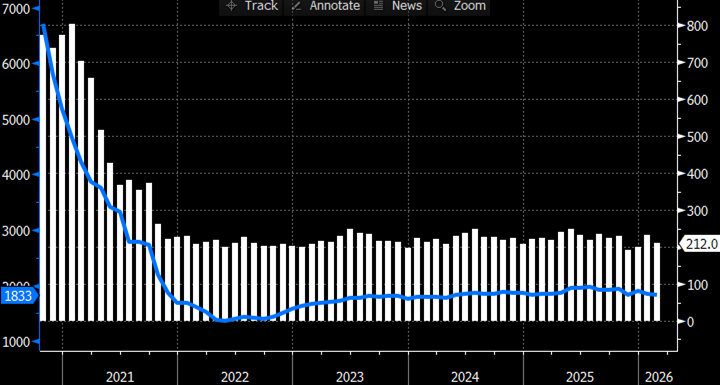

- Yesterday we received the latest update to Initial Jobless Claims and if it seems like Groundhog Day, that’ because the numbers never seem to change much. For the week ending February 21 claims rose to 212 thousand compared to 208 thousand the prior week and expectations for 216 thousand. The four-week moving-average ticked up to 220.25 thousand, the highest since November 2025, but historically speaking still quite low. Continuing Claims for the week ending February 14 came in at 1.833 million, a 4-week low, compared to the prior week at 1.864 million and 1.855 million expected. The relatively static nature of the claims series reflects the low-hire, low-fire environment we’ve been stuck in for nearly a year now. The low-hire piece was confirmed earlier in the week by the Conference Board’s Jobs Hard-to-Get metric hitting a post-pandemic high.

- Next week will be more like the traditional first week of the month with plenty of first-tier February data points, including nonfarm payrolls on Friday. It’s been several months since we could say that given the backup in data output following the October government shutdown. ISM’s will start the week; ADP will arrive on Wednesday with the February jobs report the Friday highlight. Expectations are looking for 60 thousand new jobs which is close to the estimated new equilibrium level but remember that January’s print was nearly double expectations, but it was mostly shrugged off given the issues with BLS and downward revisions countering some of the beat.

- If February’s jobs report beats decisively as well, and January is not materially revised lower, that may begin a repricing of both rate cut expectations (less cuts expected) and longer end yields (upward pressure). The weekly Pulse Report from ADP has seen four consecutive weeks on increasing private sector job gains and the survey week for payrolls coincided with a monthly low print for initial jobless claims. Both of those indicators point to a possible beat of February expectations. That will be more fully explored next week, and ADP and BLS often march to the beat of their own drummer so the intrigue will continue until we see the report, this time next week.

Groundhog Day with Initial and Continuing Jobless Claims – Low-Hire, Low-Fire Continues Source: Dept. of Labor

Source: Dept. of Labor

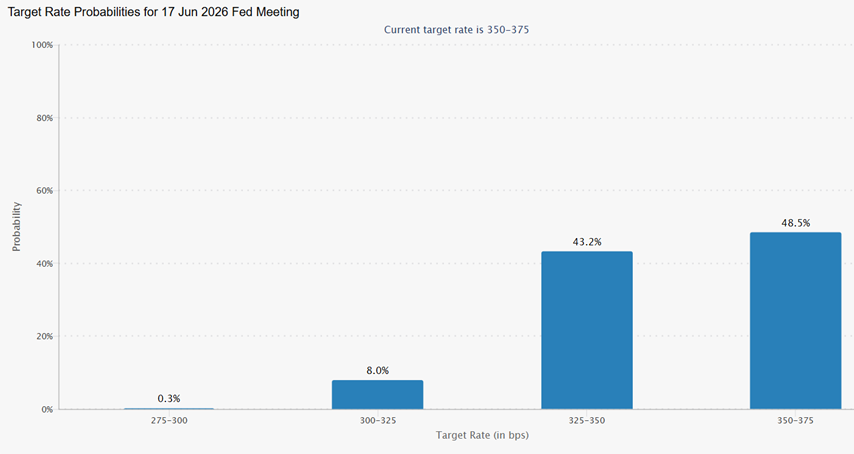

Rate Odds Continue to Decrease for a June Cut – Now Less Than 50% Odds for a Cut

Source: CME Group

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.