2yr Treasury Yield Reaches 4.00%

- The weekend beckons but uncertainty over what may transpire in the Middle East is keeping markets on edge. It’s clear that economic data is taking a backseat to war events, particularly with what that means to energy costs as transits through the Strait of Hormuz remain choked off for the most part. While a risk-off tone prevails, it’s been tempered by memories from last April when a suddenly announced delay in tariffs led to a 10% gain in the S&P500 in a single day, April 9th. Thus, more dramatic moves in oil prices and rates have been attenuated, for now, but for how long that persists is anyone’s guess. We’re already seeing the 2yr yield cross 4% in early trading. Away from gaming out war scenarios, next week brings a bevy of first tier economic reports but how much attention they garner will be conditioned on what has or hasn’t transpired on the war front. Currently, the 10yr is yielding 4.46%, up 5bps, while the 2yr is yielding 4.00%, up 2bps on the day.

- Next week brings the usual first week plethora of first tier reports, highlighted by the March jobs report on Friday. That happens to also be Good Friday with markets closed so any reaction will have to wait until the following Monday. Add to that any weekend war news and Monday morning volatility could be strong! Meanwhile expectations for the March jobs report are for 50 thousand new jobs with the unemployment rate unchanged at 4.4%.

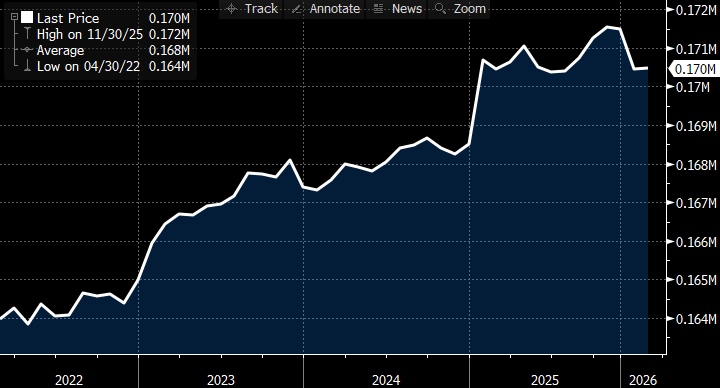

- There remains uncertainty about where the new equilibrium level of job creation is following a slowdown in immigration and upturn in deportations which has shrunk the labor force over the past year by just over 1 million workers (see graph below). It used to be thought that job growth of 150 thousand per month was necessary to maintain a stable unemployment rate when immigration levels, and a growing labor force, were higher. Thus, a lower equilibrium level is expected, but at what level exactly?

- Over the last five months, we’ve had three months with negative job growth for an average loss of 82 thousand per month. Yet the unemployment rate has been unchanged over that time. Obviously, job losses with no change in the unemployment rate cannot persist. What is clear, however, is that minimal job creation will be sufficient to maintain a stable unemployment rate. The Fed has often referred to the stable unemployment rate as reflective of a stable labor market allowing them to indefinitely pause rate cuts until there is further inflation improvement. It’s obvious, however, that labor force declines and net job losses are not ingredients for a growing, robust economy.

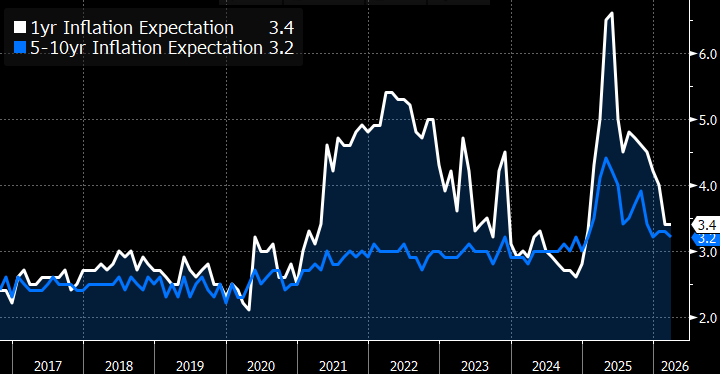

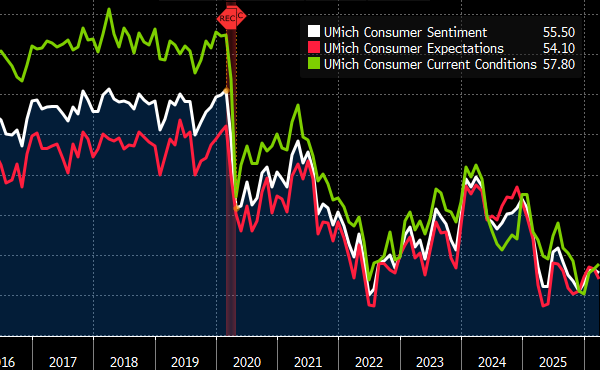

- The last report of the week is due later this morning (10am ET) with the final look at March sentiment from the University of Michigan. With war uncertainty raging, we’ll see if the preliminary numbers from last Friday, which saw some slippage in sentiment along with slightly higher inflation expectations, experience major revisions. Expectations are that there will be a dip in sentiment from 57.8 to 56.9, with 1yr inflation expectations moving higher from 3.4% to 3.9%. 5-10yr inflation expectations are also forecasted to increase from 3.2% to 3.5% (see graph below).

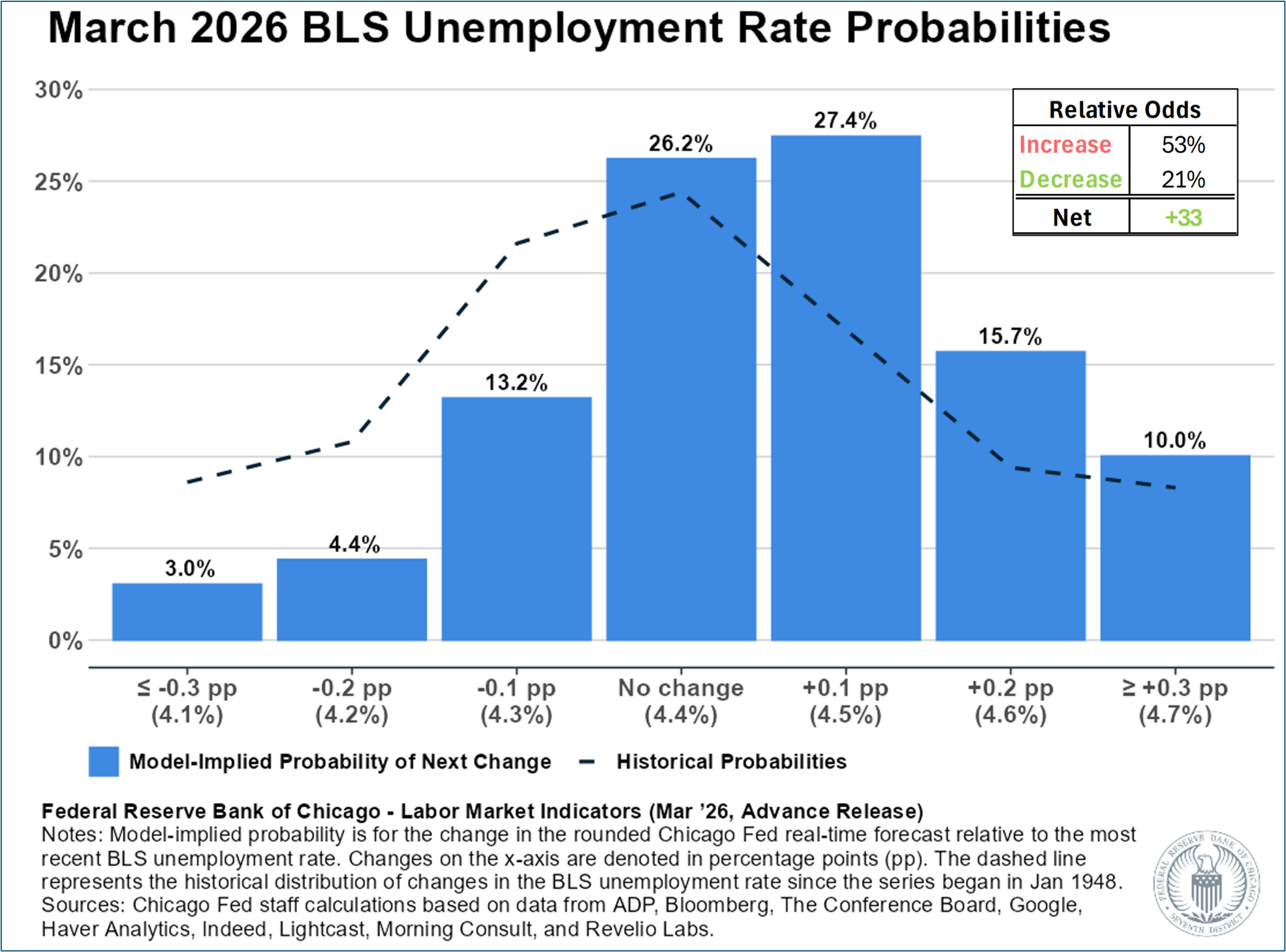

- The Chicago Fed Real-Time Unemployment Rate Forecast for March is 4.46%, up slightly from the BLS 4.4% rate for February. The Chicago Fed Real-Time Unemployment Rate Forecast is a median estimate of the unrounded BLS unemployment rate from a statistical model. The BLS reports the official unemployment rate rounded to the nearest tenth, although many analysts dig into the details for the unrounded figure. The current forecast implies 21% odds of a decrease, 26% odds of no change, and 53% odds of an increase, (see graph below).

- Initial jobless claims continue to roll along with little change and no hint that layoffs are accelerating in any material way. For the week ending March 21, initial jobless claims totaled 210,000, an increase of 5,000 from the previous week’s unrevised level of 205,000. The 4-week moving average was 210,500, a decrease of 250 from the previous week’s unrevised average of 210,750.

- For the week ending March 14, continuing jobless claims totaled 1,819,000, a decrease of 32,000 from the previous week’s revised level. This is the lowest level for continuing claims since May 25, 2024, when it was 1,804,000. The previous week’s level was revised down by 6,000 from 1,857,000 to 1,851,000. The 4-week moving average was 1,847,000, a decrease of 2,000 from the previous week’s revised average. This is the lowest level for this average since October 5, 2024, when it was 1,845,750. Thus, with all the uncertainty in our world now jobless claims continue to be steady with little in the way of improvement or deterioration.

Univ. of Michigan Sentiment – Inflation Expectations Forecast to Move Higher  Source: Univ. of Michigan

Source: Univ. of Michigan

Univ. of Michigan – March Sentiment Reading Due Later This Morning Source: Univ. of Michigan

Source: Univ. of Michigan

Labor Force (Workers and Those Looking for Work) – Declining in 2026 Source: BLS

Source: BLS

Source: Chicago Fed

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.