A No Surprises PCE Boosts Treasury Rally

- We wrote on Wednesday about the sudden heavy selling in some of the darlings of the equity world and whether it marked the beginning of something more ominous. However, with an earnings and forward guidance beat by one of those darlings, Micron Technologies, the rally resumed and combined with a no surprises PCE update yesterday, consumers can apparently breathe a sigh of relief that their nest eggs are safe for now. Ergo, let the consumption continue! We discuss the PCE in more detail below, but our updated economic forecast still sees a rate hike later this year. Currently, the 10yr is yielding 4.39%, unchanged on the day, while the 2yr is yielding 4.10%, down 2bps on the day.

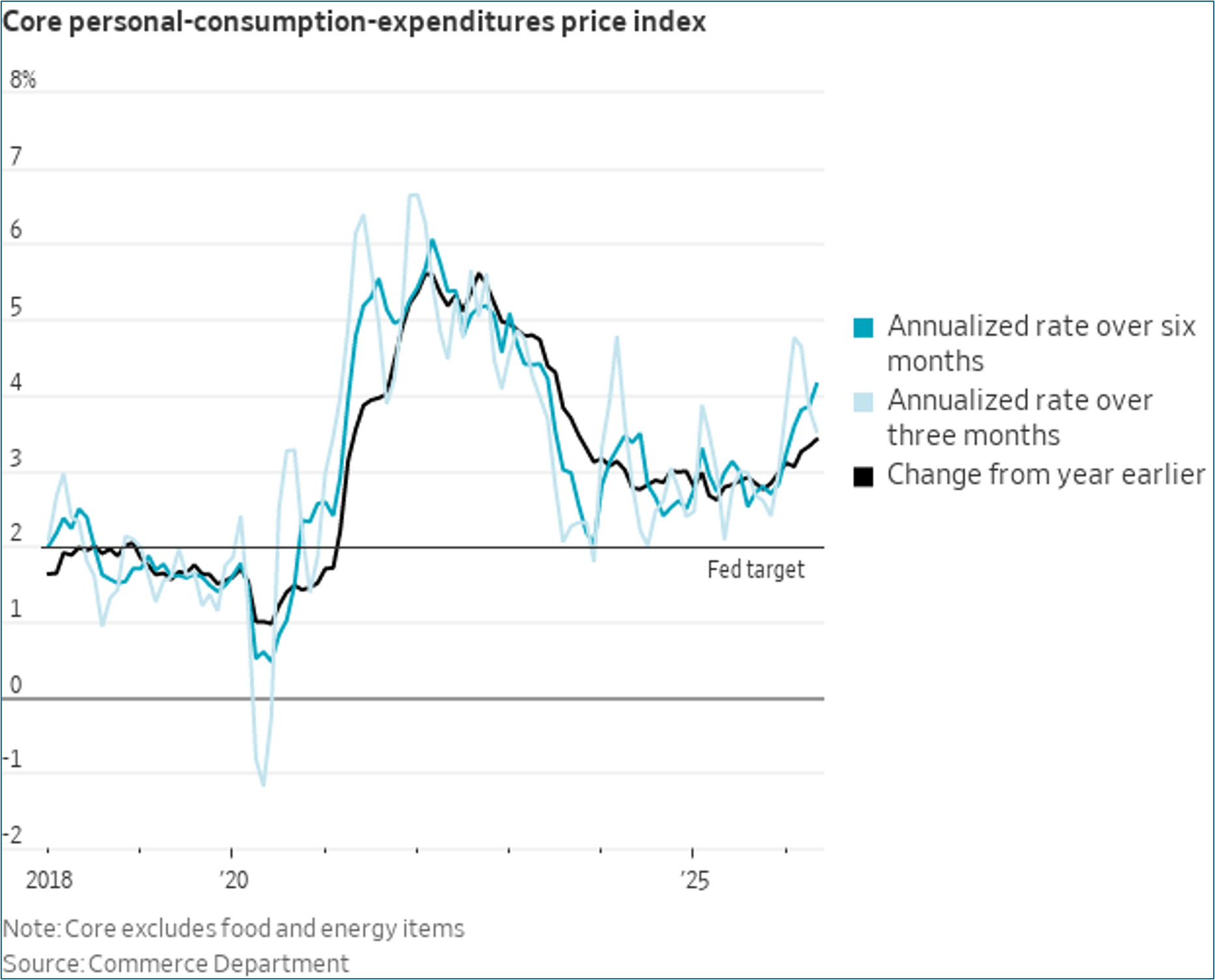

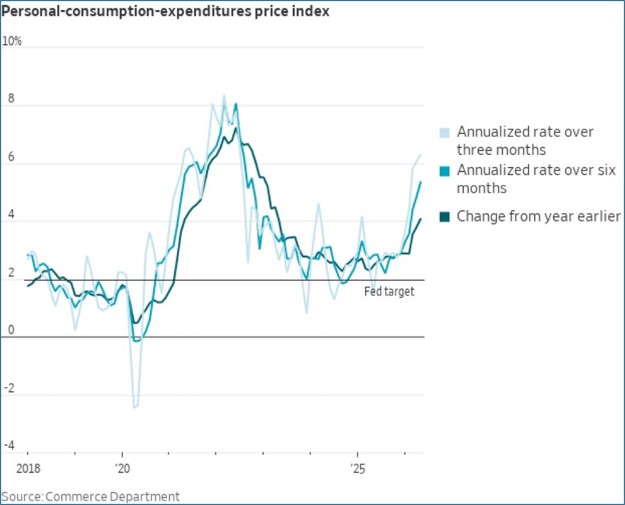

- Yesterday, brought us the May Personal Income and Spending Report with its all-important PCE inflation series. Now to be fair, the subsequent decrease in oil prices in June cast this May inflation report as probably the peak for the year and that reality took some of the potential sting out of the results. The results were, for the most part, as expected. Overall PCE rose 0.4%, slightly better than 0.5% expected but matching the April result. YoY PCE increased from 3.8% to an as expected 4.1%. That’s the highest YoY in three years, but market expectations are that with falling oil prices, May should represent peak inflation for 2026. Ex-food and energy, core PCE increased 0.3%, matching expectations but higher than the 0.2% in April. YoY core PCE increased 3.4%, matching expectations and a tenth higher than April. It’s the highest core YoY rate since October 2023.

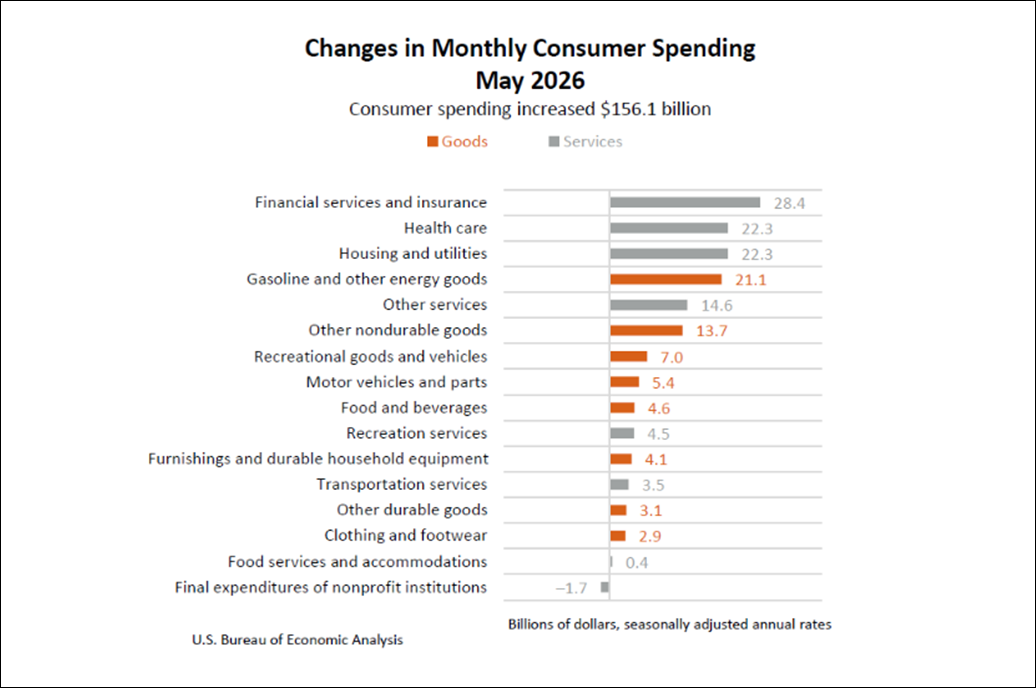

- The top five categories in spending increases, out of 16 total, were essential-type items, but discretionary items also showed up in the top 10 as the consumers in the upper leg of the K-shaped economy continued to spend on recreation items, etc. The spending after adjusting for inflation was up a solid 0.3% vs. 0.2% expected and 0.1% in April. 0.3% is the highest real spending gain since last July’s 0.5%. That’s a plus considering that first quarter GDP’s third revision found consumption in the first quarter at just 0.5% annualized, so, the second quarter looks as though the consumer rebounded after taking a first quarter breather.

- Personal income rebounded as well in May. Recall in April, personal incomes were unchanged as a drop in farm income overwhelmed the typical wage/salary contributions during that month. Farm income rebounded in May, and wages/salaries held up leading to the positive 0.7% increase in incomes. That boosted the personal savings rate that had been declining and leading to some concerns the consumer was losing firepower to continue spending. That doesn’t appear to be the case after the May results.

- On net, it was a positive report on the income, consumption, and inflation fronts. While inflation rates increased, with the subsequent drop in oil prices in June it appears the high-water mark for inflation is in for this year. The question is how quickly will inflation move to the 2% Fed target? We think it will be a grinding move lower and not happen this year, with next year an outside possibility. On a more positive note, the uptick in incomes provides some breathing room for additional consumption, plus the expected drop in gas prices, and that should keep the economy moving ahead at near 2% GDP in the third and fourth quarters of 2026.

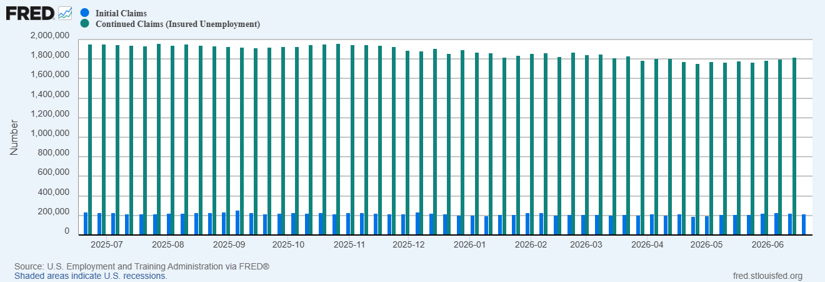

- Initial jobless and continuing claims continued with the low-fire theme, adding another positive anecdote to what should be a solid June jobs report next week. Initial claims for the week ending June 20 decreased from 227 thousand to 215 thousand. The 4-week average, however, increased slightly from 223.50 thousand to 224.25 thousand. Meanwhile, continuing claims for the week ending June 13 increased from 1.800 million to 1.821 million. As the graph below shows, however, little has changed between the two measures for months now as companies have slowed hiring but remain content to hang onto employees through the current war-induced uncertainty.

- Finally, we just released our latest quarterly rate and economic forecast. With a new Fed Chair voicing strong support for hitting the 2% inflation target, along with a tentative peace deal with Iran, we’ve prepared our latest view of rates and the economy based on these events. Our previous forecast had a rate cut expected before year end, but now that’s flipped to rate hike. Find the forecast here.

May Core PCE (YoY) Hits Highest Since October 2023 but Should be the High Rate for 2026

Source: US Commerce Dept.

May PCE (YoY) – Highest in Three Years but Should be Headed Lower from Here

Source: US Commerce Dept.

Essential Categories Led Spending, but Discretionary Items Appear in Top 10 too

Source: US BEA

Initial and Continuing Jobless Claims Reflect the Low-Fire Environment

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.