ADP February Job Growth Largest Since July

- With the war moving into Day 5, and financial markets finally taking notice, we find ourselves with another round of February employment numbers before the big BLS report on Friday. As for today, we have some privately sourced labor market data with the ADP Employment Change Report and a little later the ISM Services Index (more on that below). Currently, the 10yr is yielding 4.07%, up 2bps, while the 2yr is yielding 3.51%, up 1bp on the day.

- The ADP Employment Change Report for February reported 63 thousand new private sector jobs, the largest gain since July and ahead of the 50 thousand expected and 11 thousand in January (revised down from 22 thousand). So, a decent- to-solid read and while the relationship between ADP and BLS is tenuous at best, it does put more attention on the upcoming jobs report which is expecting 65 thousand private sector jobs.

- Job gains were strongest again in healthcare at 58 thousand while manufacturing shed jobs for the 24th straight month, this time 5 thousand jobs were lost. Ironically, the smallest firms (1-19 employees) added 58 thousand jobs while the largest firms (>500 employees) grew just 10 thousand jobs. Annual wage growth for Job Stayers was 4.5%, same as in January. Annual wage growth for Job Leavers was 6.3% vs. 6.4% prior. Wage gains have been steady since peaking at 8% (job stayers) and 16% (job leavers) in 2022. A year ago, annual wage gains for job stayers was 4.6% and for job leavers 6.6%. So, wage growth has been stable for the last year.

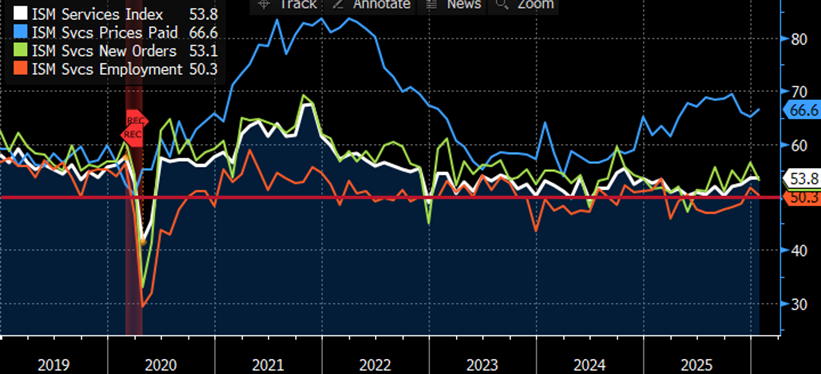

- At 10am ET, the ISM Services Index will be released with a slight dip expected from 53.8 to 53.5. That be in solid expansionary territory but with a slight loss of momentum. Like the ISM Manufacturing release, the readings on Prices Paid, New Orders, and Employment will round out the picture of the dominant service side of the economy.

- On Monday, the ISM Manufacturing surprised to the upside with a big pop in prices and new orders and while the employment metric ticked higher (48.8) it remained in contractionary territory. Prices paid hit a 70.5 reading, the highest since 2022 and an 11.5-point jump from January. And this is before any price uptick coming from the Iran war. As you would expect with the strong beat on orders, there was plenty of commentary from managers that order books were seeing genuinely more activity, but never far away were the comments of ongoing cost pressures with time consumed with tariff mitigation strategies, and good old uncertainty from shifting tariff policies and the legal debate around them. In reading between the lines if trade policy was squared away, new orders would most likely lift again, and cost pressures would likely abate.

- Tomorrow will bring a couple more privately sourced labor market reads with the February Challenger Job Cuts and Revelio Labs read on private sector payroll growth. Last month Revelio reported 13 thousand jobs. Challenger reported 108 thousand job cuts in February vs. 63 thousand average monthly cuts in 2025. Meanwhile, expectations for Thursday’s initial jobless claims point to a continuation of the low-hire, low-fire environment that we know so well at this point.

- Finally, the Fed’s Beige Book of economic conditions will be released this afternoon and will be a part of the economic conversation at the FOMC meeting in two weeks. While the subsequent events from Iran will not be a part of today’s release, the impact from that would probably be waved off at this point as temporary (or could we say, transitory?), so the outlook will still be important for Fed deliberations. Recall, in the January FOMC Powell spoke of an improving economic outlook in that month’s Beige Book so we’ll be looking to see of those same sentiments, or similar, are expressed today.

ADP Wage Gains Stable Over Last Year

February ISM Services Index Due This Morning – Biggest Focus May Be on Prices Paid Source: ISM

Source: ISM

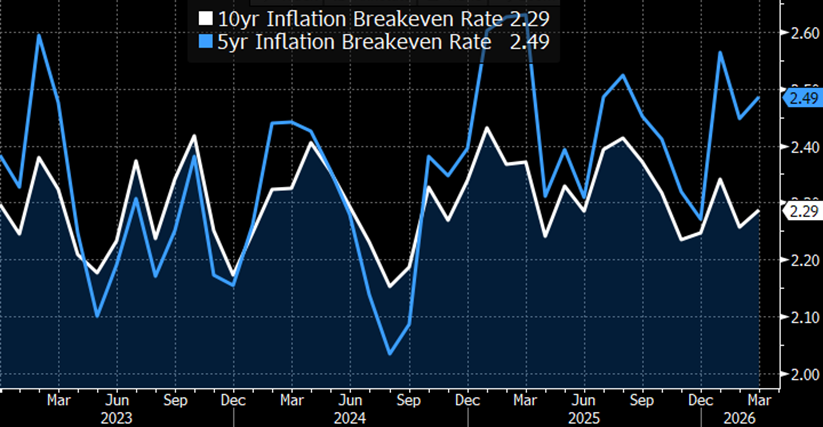

TIPS Inflation Breakevens – Higher but not as Strong as Nominal Coupon Bonds Source: Bloomberg

Source: Bloomberg

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.