ADP January Job Growth Disappoints

- The first government shutdown of 2026 lasted all of three days but that was enough to see the BLS delay its releases this week which included the December JOLTS due yesterday and more importantly the January BLS Nonfarm Payrolls due on Friday. The House passed the bill, which funds an array of agencies through September, and President Trump signed it while the clock ticks on the DHS two-week funding extension. Expect some fireworks on that one! In any event, we find ourselves in familiar territory yet again, but we have some privately sourced labor market data to make do until BLS releases the delayed reports, starting with today’s ADP Employment Change Report (more on that below). Currently, the 10yr is yielding 4.28%, up 1bp, while the 2yr is yielding 3.58%, unchanged on the day.

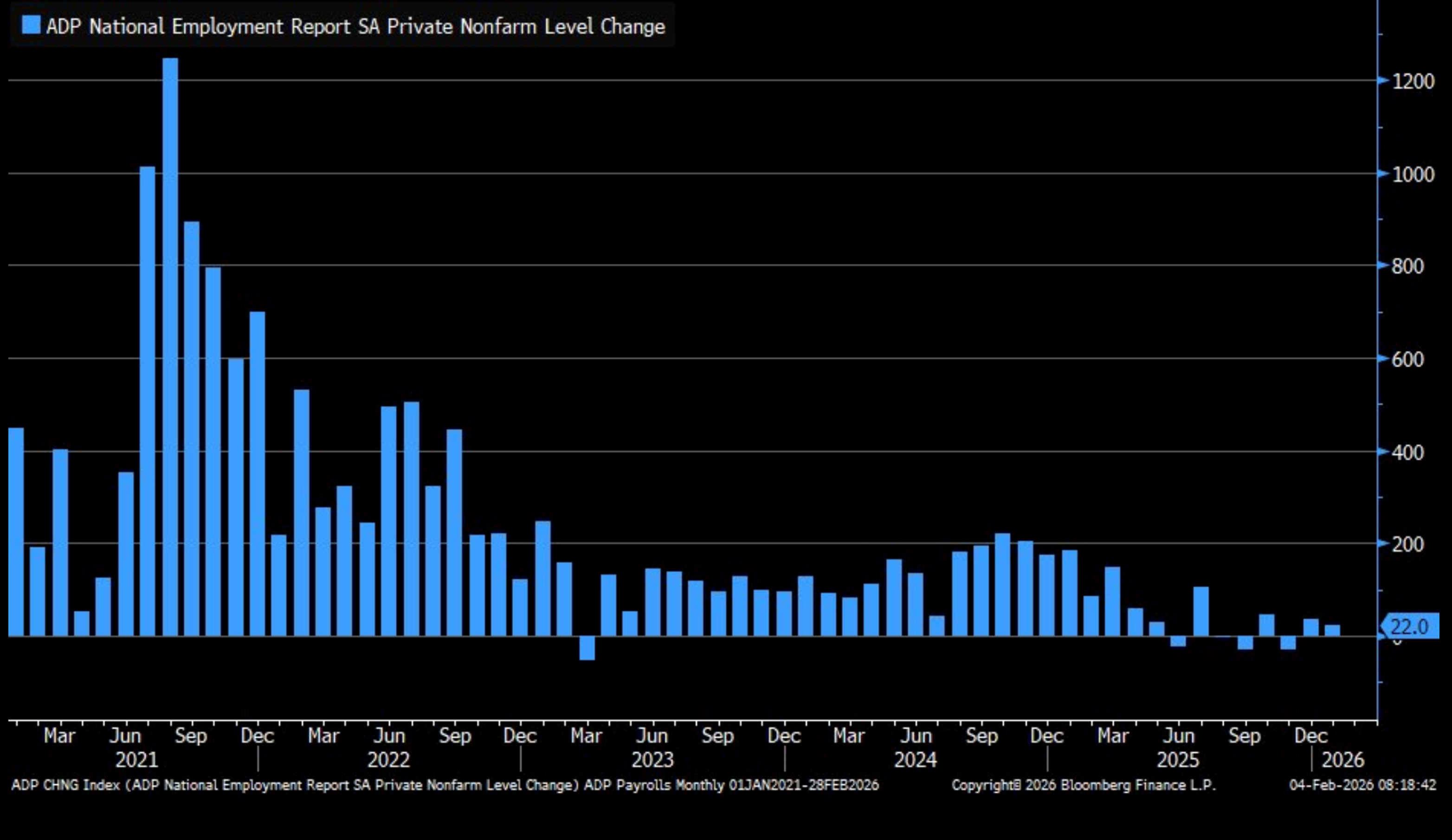

- While the government shutdown is over, the BLS has indicated that the Friday payrolls report will be delayed. No date has been given for the revised release date, but it should be early next week. In any event, we do have some privately sourced labor market data and the first out of the box is today’s ADP Employment Change Report for January. ADP reported 22 thousand new private sector jobs, well short of the 45 thousand expected and 37 thousand in December (revised down from 41 thousand). So, a disappointing read but one that probably lacks sufficient weakness to improve odds of a March cut, which stand at 10% after the release.

- Job gains were strongest again in healthcare at 74 thousand while manufacturing shed jobs for the 23rd straight month. Middle size firms (50-500 employees) added 41 thousand jobs while the largest firms (>500 employees) shed 18 thousand jobs. Perhaps that’s a reflection of several high-profile layoff announcements in the last several months. Also, annual wage growth for Job Stayers was 4.5% vs. 4.4% in December. Annual wage growth for Job Leavers was 6.4% vs. 6.6% prior. Wage gains have been steady since peaking at 8% (job stayers) and 16% (job leavers) in 2022. A year ago, annual wage gains for job stayers was 4.70% and for job leavers 6.80%. So, wage growth has been stable for the last year.

- Later this morning (10am ET), the ISM Services Index will be released with a slight dip expected from 53.8 to 53.5. That would still be in expansion territory but with some loss of momentum, nonetheless. Like the ISM Manufacturing release, the readings on Prices Paid, New Orders, and Employment will round out the picture of the dominant service side of the economy.

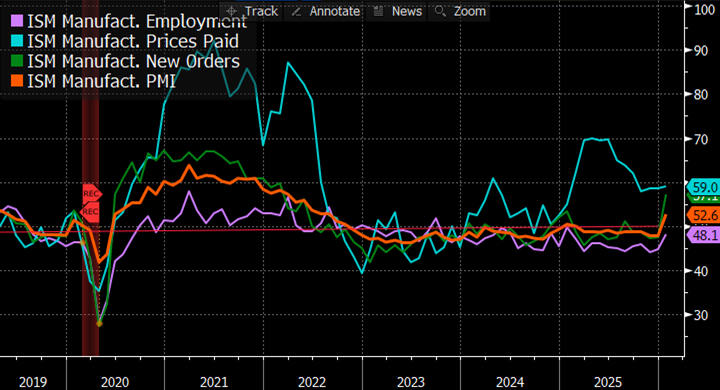

- On Monday, the ISM Manufacturing surprised to the upside with a big pop in new orders with the employment metric ticking higher but it remained in contractionary territory. Prices paid also moved higher but off the peak levels of early 2025. Despite the surprising beat on orders, most of the commentary from managers was pessimistic with continuing uncertainty over ever-shifting trade policies and ongoing price pressure from tariffs the two most frequently cited concerns. Some analysts suspect the pop in orders was more about the latest round of tariff-frontrunning, along with post-holiday restocking, rather than a legitimate turn in the manufacturing sector. It seems the market will need another month or two of similar results before it calls the bottom in.

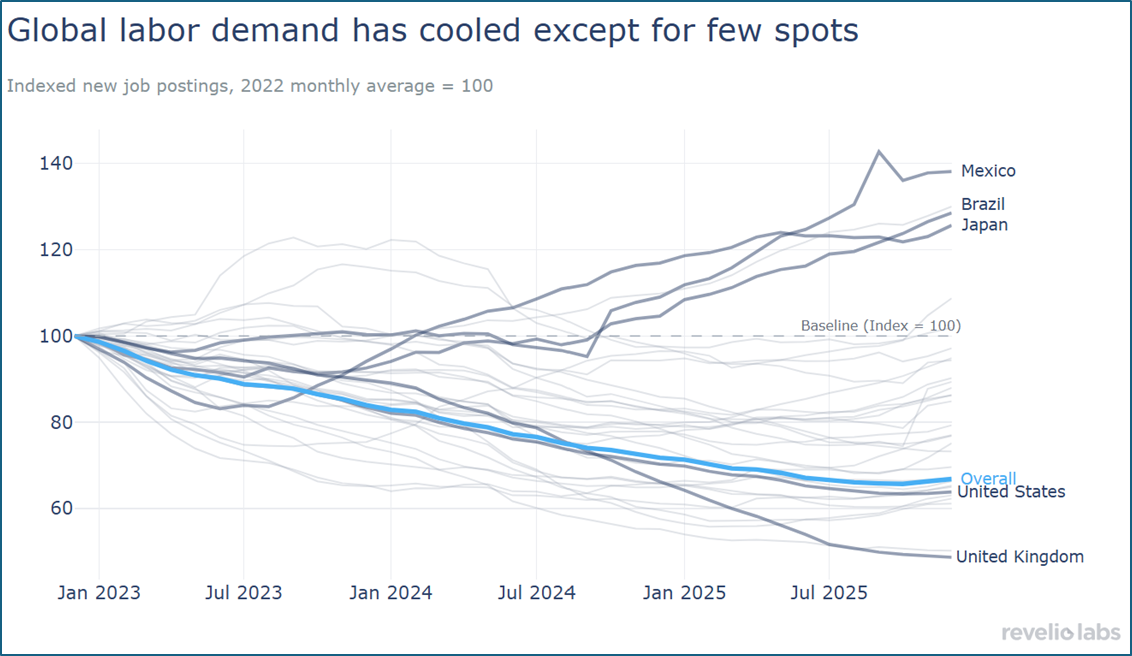

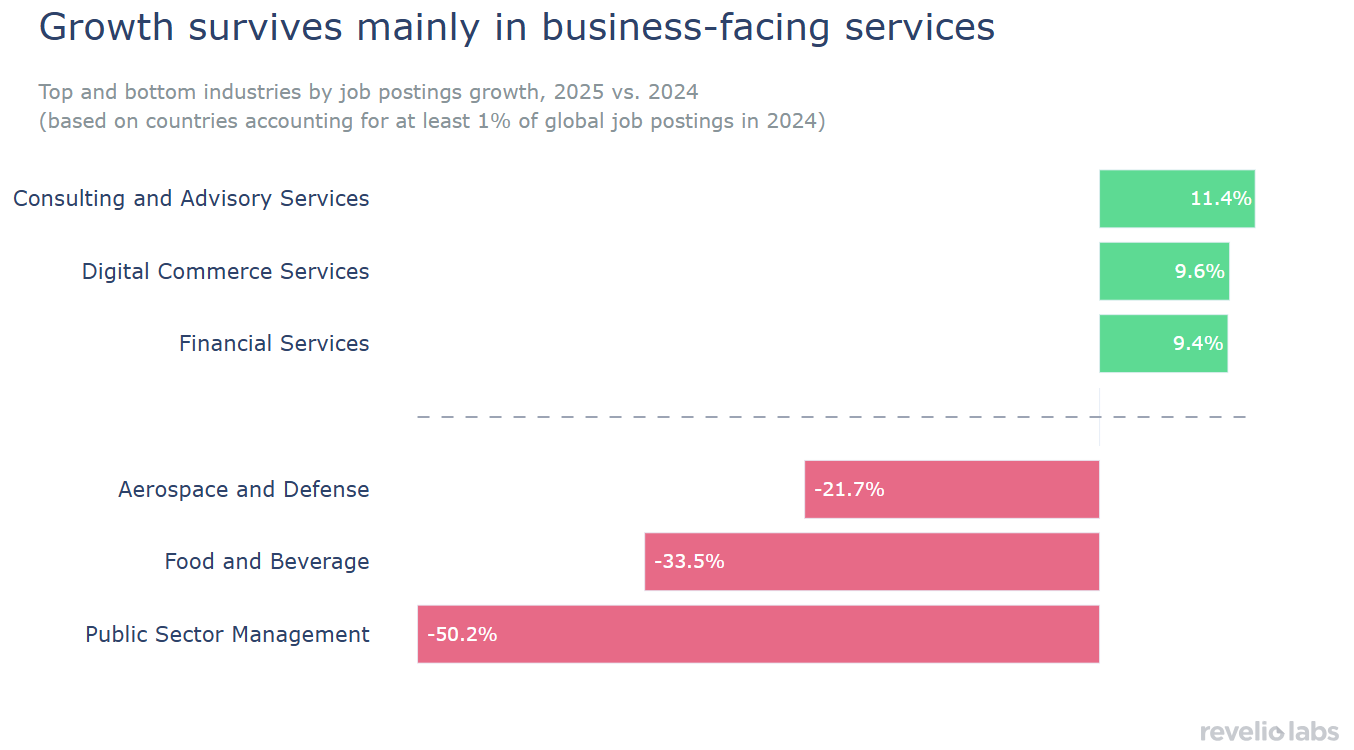

- Tomorrow will bring a couple more privately sourced labor market reads with the January Challenger Job Cuts and Revelio Labs read on private sector payroll growth. Last month Revelio reported 71 thousand new jobs. That was the highest job growth since April 2025 at 72 thousand which was also the highest monthly gain in 2025. Challenger reported 35 thousand job cuts in December vs. 63 thousand average monthly cuts in 2025. Some additional graphics below from Revelio Labs point to a slowing in job postings globally with the US lagging its peers, and another graphic highlights the sectors seeing the most strength globally and those with the greatest weakness.

ADP Employment Report – Private Sector Job Growth Only 22K vs. 45K Expected Source: ADP

Source: ADP

January ISM Manufacturing – Surprising Pop in New Orders

Source: ISM

Revelio Labs – Job Postings are Climbing in a few Countries Source: Revelio Labs

Source: Revelio Labs

Source: Revelio Labs

Source: Revelio Labs

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.