ADP Reports Another Month of Solid Job Growth

- May data is starting to arrive and so far, it looks like another decent month of economic activity. From this point, the reports will focus on the labor market with today’s ADP Employment Change Report and the ISM Services Index with its employment measure for May. We discuss the findings of the reports below. We also have some Fed speak to round out the offerings. Yesterday, a dissenter from the April meeting spoke and Beth Hammack (Cleveland Fed Pres.) was predictably hawkish. The money quote from her address was, “if recent data trends continue, it may soon be appropriate for policy to act to address the growing risks of persistently elevated inflation” (read: rate hike). Expect more Fed rhetoric before the pre-FOMC blackout period hits on Saturday. Currently, the 10yr is yielding 4.50% up 4bps on the day, while the 2yr is yielding 4.09%, also up 4bps on the day.

- The first of several labor market reports for May was released this morning with the ADP Employment Change Report narrowly beating expectations with 122 thousand new private sector jobs vs. 120 thousand expected and 105 thousand in April. While April was the largest monthly gain since January 2025, the May gain exceeded that, so, another solid read on private sector hiring in May. While the relationship between ADP and BLS has been tenuous in the last couple years it adds to the sense that the upcoming jobs report, which is expecting 86 thousand private sector jobs and 85 thousand overall, will be decent as well.

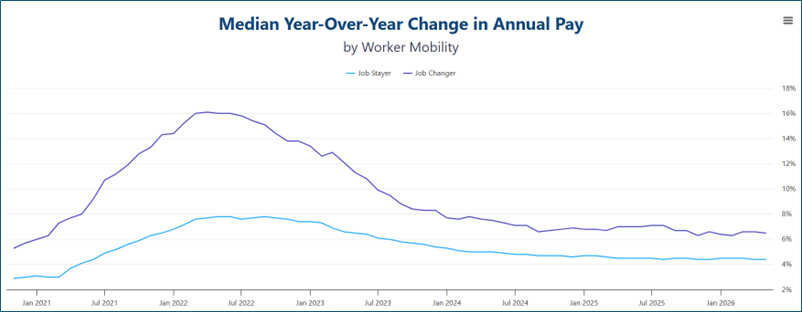

- As usual, job gains were strongest in healthcare at 57 thousand while manufacturing, which halted a 26-month losing streak in April, added another 3 thousand jobs in May. Annual wage growth for Job Stayers was 4.4%, matching the April gain, while annual wage growth for Job Leavers was 6.5% vs. 6.6% in April. Annual wage gains have been trending lower since peaking at 8% (job stayers) and 16% (job leavers) in 2022. Over the past year, however, wage gains have been fairly stable. A year ago, annual wage gains for job stayers were 4.5% and for job leavers 7.0%.

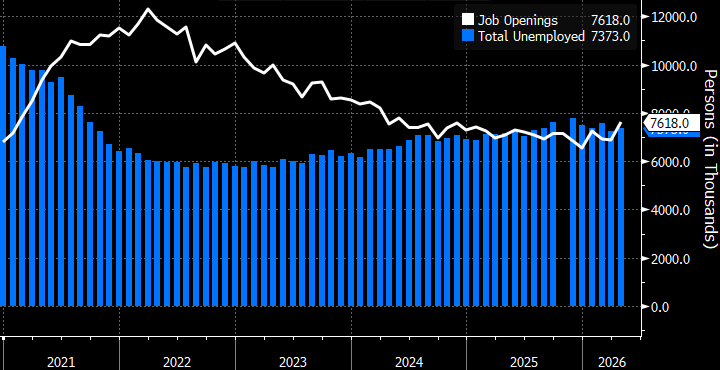

- Yesterday, another labor-related report but for April, the Job Opening and Labor Turnover Survey (JOLTS) reported job openings jump to the highest level in almost two years and layoffs fell, adding to signs the labor market remained resilient as data center buildout and the ongoing strength in healthcare propelled openings. Available positions rose to 7.62 million from 6.89 million. Also signaling strength the Layoff Rate (layoffs to total employed) dipped from 1.2% to 1.1%. It touched a low of 1.0% in January and November in the past year and indicates, much like the rather docile Initial Jobless Claims, that the low-fire environment continued in May.

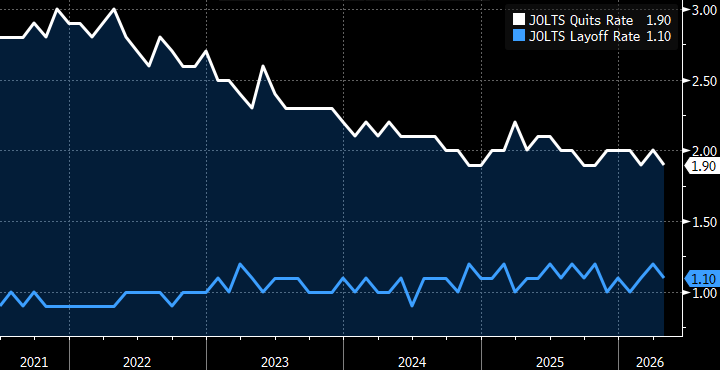

- However, the Quits Rate (voluntary separations to total employed) dipped from 2.0% to 1.9%. That matches the low set in February and last October and November and is the lowest rate since 2020. It’s a measure of worker confidence in finding better/higher paying employment so the downtick indicates a slight reduction in confidence which is opposed to other indicators from an otherwise upbeat report. The one-tenth dip can be written off as statistical noise at this point; however, if it continues it will probably be joined by other signs of weakening which would indicate further slowing in labor market momentum. For now, the story remains one of softer labor force growth, but growth, nonetheless.

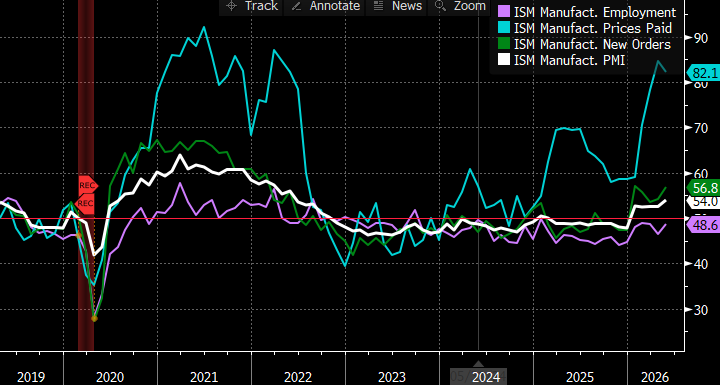

- At 10am ET, the ISM Services Index will be released with expectations for the headline to tick higher from April’s 53.6 to 53.8. If expectations are met, the largest segment of the economy continued in solid expansionary territory for May. Much like the manufacturing sector report from Monday, the Prices Paid Index will get inflation scrutiny with the index expected to increase from 70.7 to 72.3. If that comes to pass, it will be the highest prices paid reading since August 2022 and another indication that inflation pressures continue to move the wrong way.

- New Orders are expected to slip slightly from April’s 53.5 to 53.1, and the Employment Index is expected to improve from 48.0 to 49.0 but still be below the 50 expansion/contraction dividing line but certainly an improvement from March’s 45.2, the lowest since December 2023. Thus, both the manufacturing and services sectors are firmly in expansion territory, with positive movement in employment, but ongoing price pressures. That seems to be a familiar refrain.

- With most of the labor-related reports this week reflecting positive results, the angst over Friday’s Nonfarm Payrolls Report is reduced a bit. Expectations are for 85 thousand new jobs vs. 115 thousand in April. The unemployment rate is expected to remain unchanged at 4.3%, for the third straight month, with hours worked also stable at 34.3 hours. Average Hourly Earnings are expected to improve from 0.2% MoM to 0.3% with but the YoY rate is expected to fall from 3.6% to 3.4%, as a 0.4% gain from last year rolls off. The Labor Force Participation Rate is expected to remain unchanged at 61.8.

ADP Annual Wage Gains Mostly Stable Over the Last Year but Down from 2022 Peak Source: ADP

Source: ADP

April JOLTS – Job Openings Move Unexpectedly Higher, Now Exceeds Unemployed Persons Source: BLS

Source: BLS

JOLTS – Quits Rate Dips but Layoff Rate Dips Too: Low-Hire, Low-Fire Continues Source: BLS

Source: BLS

May ISM Manufacturing – Overall Rate Improves, Along with New Orders and Employment, Prices Paid Elevated Source: ISM

Source: ISM

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.