An Early Close before a Long Memorial Day Weekend

- An abbreviated trading day is all that stands between us and a long Memorial Day weekend, with the only report left being a final look at consumer sentiment from the University of Michigan. Expect confirmation of the record-low sentiment print from last week’s preliminary release. Yesterday, we received the first May-based activity report with the S&P Global Preliminary PMI series. We discuss that in detail below along with the latest on jobless claims (spoiler alert: not much change there). In all, it should be a quiet day into the early 2pm ET close. I hope that’s not famous last words! Currently, the 10yr is yielding 4.54%, down 4bps, while the 2yr is yielding 4.07%, down 1bp on the day.

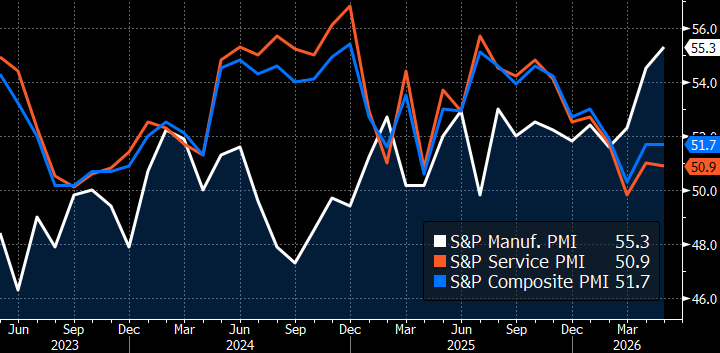

- Yesterday, brought us the first look at May activity with the S&P Global Preliminary PMI readings. While they’re not as influential as the more famous ISM series it is a quality report that warrants attention, and it comes more than a week before the ISMs. US business activity growth held steady in May at a modest rate compared to earlier in the year as improved performance in manufacturing was offset by a slowing in the service sector. The report noted, however, that factory growth was, like the previous month, supported by temporary inventory building and both sectors reported that new orders had been somewhat subdued by the Iran war, most notably in terms of export sales.

- The Services PMI Index slipped from 51.0 to 50.9, a 2-month low. Meanwhile, the Manufacturing Index rose slightly from 54.5 to 55.3, a 48-month high. The US Composite Index, covering both manufacturing and services, held steady at 51.7. The report noted that growth over the past three months since the outbreak of the Iran war has been the weakest since the start of 2024.

- Employment patterns differed between the two sectors. Service sector jobs dropped at the second-fastest pace since May 2020 while manufacturing payrolls rose by the most in 11 months as factories boosted headcount to meet increased orders. Meanwhile, input prices surged to the highest since November 2022, owing to supply constraints and increased energy prices. Manufacturing input costs registered their largest monthly increase since June 2022. While the rise in services costs was muted compared to manufacturing, it was nonetheless the steepest recorded for a year. So, kind of a mixed reading in that price pressures remains the central issue, while a softening in service sector activity was offset with increased manufacturing orders which boosted headcount. The caveat there is that those increased orders were said to be more for building inventories ahead of further price/supply pressures rather than increased end-user demand.

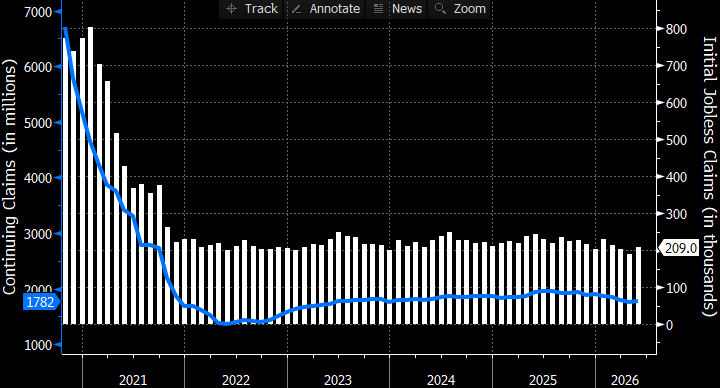

- Stop us if you’ve heard this before, Initial Jobless Claims remained mostly static with initial claims for the week ending May 16 at 209,000, a decrease of 3,000 from the previous week’s revised level. The 4-week moving average was 202,500, a decrease of 1,500 from the previous week’s average of 204,000. Meanwhile, Continuing Claims were quiet as well with the May 9 reading at 1,782,000, an increase of 6,000 from the previous week’s revised level of 1,776,000. Thus, the low-fire environment continued for yet another week, which confirms the Fed’s complacency around its full employment mandate. It’s all about inflation for the Fed as long as the labor market remains stable as indicated in these numbers.

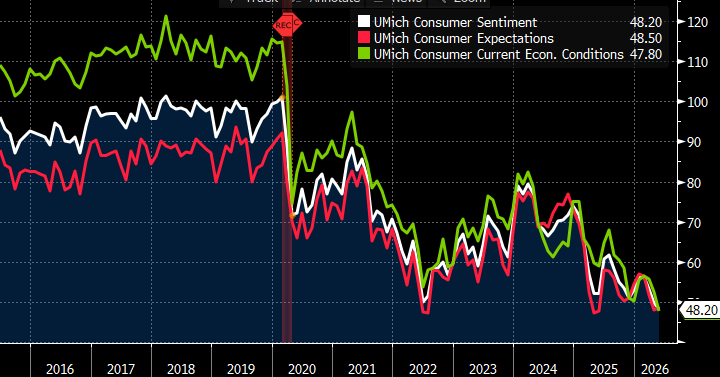

- Finally, later this morning the University of Michigan will issue its final May consumer readings on sentiment, current conditions, expectations, and inflation with little change expected from last week’s preliminary results. The headline Sentiment measure is expected to remain at a record low of 48.2. However, despite these dismal sentiment readings the consumer hasn’t pulled back much on spending, at least not in an aggregate fashion. This is more evidence that the K-shaped economy continues to benefit from the middle-to-upper-income consumer’s robust spending versus the lower income cohort’s more hesitant spending.

S&P Global Preliminary May PMIs – Manufacturing Up on Inventory Building, Services Soften Slightly Source: S&P Global

Source: S&P Global

Initial and Continuing Jobless Claims – Not Much Change in the Low-Fire Environment Source: US Dept. of Labor

Source: US Dept. of Labor

Final University of Michigan Sentiment for May Due Today – Record Low Sentiment Expected to Persist Source: Univ. of Michigan

Source: Univ. of Michigan

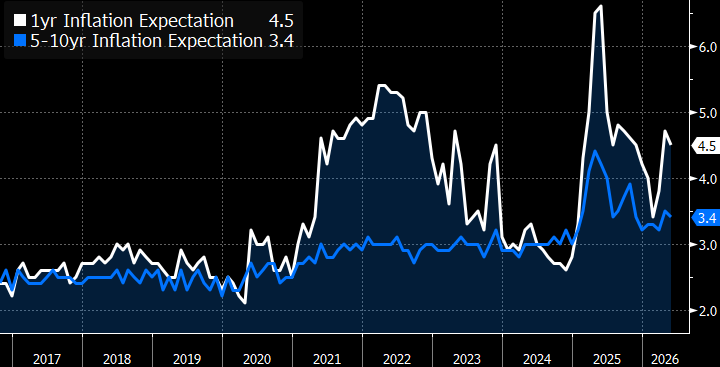

University of Michigan Consumer Inflation Expectations for May Source: Univ. of Michigan

Source: Univ. of Michigan

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.