April CPI Hotter than Expected

- The hotter than expected CPI from April kept Treasuries under pressure yesterday and with more supply and inflation reports yet to come, the bias to higher rates may have more to run. In addition, the CPI report further reduced odds of rate cuts this year. PPI today and Import Prices tomorrow will keep inflation front and center. With some notable leakage into some non-energy areas picked up in April’s CPI report, the market will be looking for more of the same today and tomorrow. Meanwhile, the Senate confirmed Kevin Warsh to the Fed yesterday, but his path to corralling an FOMC majority that supports rate cuts just got more difficult. Finally, President Trump is arriving in China this morning so expect headlines from that meeting to get plenty of airtime. Currently, the 10yr is yielding 4.46%, down 1bp, while the 2yr is yielding 3.99%, also down 1bp on the day.

- Yesterday’s April CPI was close to expectations but the seepage of higher energy costs into other costs has begun, namely in the food category. Overall inflation increased 0.6% for the month matching expectations with the YoY rate increasing from 3.3% to 3.8% vs. 3.7% expected. That’s the highest YoY rate since September 2023. Food costs rose 0.5% vs. 0.0% in March with Food at Home rising 0.7% vs. -0.2% in March. While grocery stores were apparently quick to reprice inventory, restaurants were slower with the Food Away from Home category increasing 0.2% vs. unchanged in March. Expect those menu prices to be more aggressively adjusted in May. Airfares rose 2.8% in April after increasing 2.7% in March. Over the past year airfares have increased over 20%.

- Meanwhile, core CPI came in at 0.4% (0.376% unrounded) MoM, slightly exceeding the 0.3% expectation, with the YoY rate increasing from 2.6% to 2.8%, a tenth more than expected. That’s the highest YoY rate since September 2025. For the next few months, the series will see a string of 0.1% and 0.2%MoM prints from last year roll off, making it difficult for YoY rates to improve given the recent price pressure. Instead, we expect core YoY will soon move over 3%. In addition, the expected refresh to geographic regions skipped back in the lockdown to Owners’ Equivalent Rent (the largest single CPI component) will add more upward pressure, although that will be from measurement issues and not reflective of a true near-term cost increase (explained more below).

- Shelter cost rose 0.6%, doubling the 0.3% increase in March and 3.3% YoY. Meanwhile, Owners’ Equivalent Rent (OER) rose 0.5% vs. 0.3% in March. It had been varying between 0.2% and 0.3% for the past several months which put it squarely in the 3.0% annual range, nearly back to pre-pandemic levels. The uptick in April goes back to the BLS decision coming out of the shutdown to price 2 of the 6 geographic regions that didn’t get refreshed valuations in October and November at their last projections, essentially a 0% change for a third of the OER index. Thus, while OER had been in a slightly downward trajectory, reflecting softer rental prices from the past two years, those missing regions were most likely not really at 0.0% OER. So, the downward trajectory of OER was interrupted as these missing regions were refreshed with updated rates.

- With the concerns over housing cost inflation mentioned above, it puts more emphasis on the core services ex-housing measure, the so-called Super Core measure. This was the “sticky” component to inflation Powell often mentioned that stalled improvement during 2024 and early 2025. For April, the Super Core measure rose 0.45% vs. 0.18% in March. YoY the level is 3.4%. Bottom line, with the renewed price pressure from the energy complex, heavily weighted items like OER and core services will have to drop consistently into the 0.1% to 0.2% range to limit energy price pressures placed on the index. With OER going through a refresh from the lockdown, the Fed will probably be waiting until late this year, if not into 2027, to find inflation once again approaching 2%.

- Today brings the wholesale PPI series with headline Final Demand expected up 0.5%, matching the March increase. The YoY rate is expected to surge from 4.0% to 4.8%. Ex-food, energy and trade the index is expected up 0.3% vs. 0.2% the prior month with the YoY rate increasing from 3.6% to 4.1%. These YoY rates are the highest since early 2023 when rates were retreating after peaking in late 2021/early 2022 at 7.0%. The PPI series has been gradually increasing since mid-2025 and that will work to keep retail inflation elevated as these higher wholesale prices are passed along.

- With CPI, PPI, and Thursday’s Import Prices in hand analysts will be quick to calculate the Fed’s preferred PCE inflation expectation which is due on May 28th. Last month, overall PCE was 3.5% and core PCE 3.2%. Expect both of those rates to move higher with the April numbers.

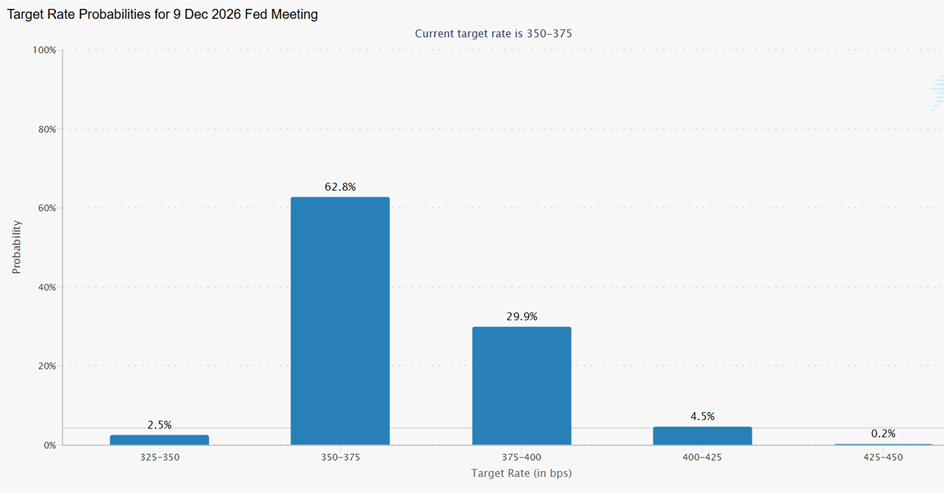

Odds of Rate Cuts This Year Under 3% After April CPI Source: CME Group

Source: CME Group

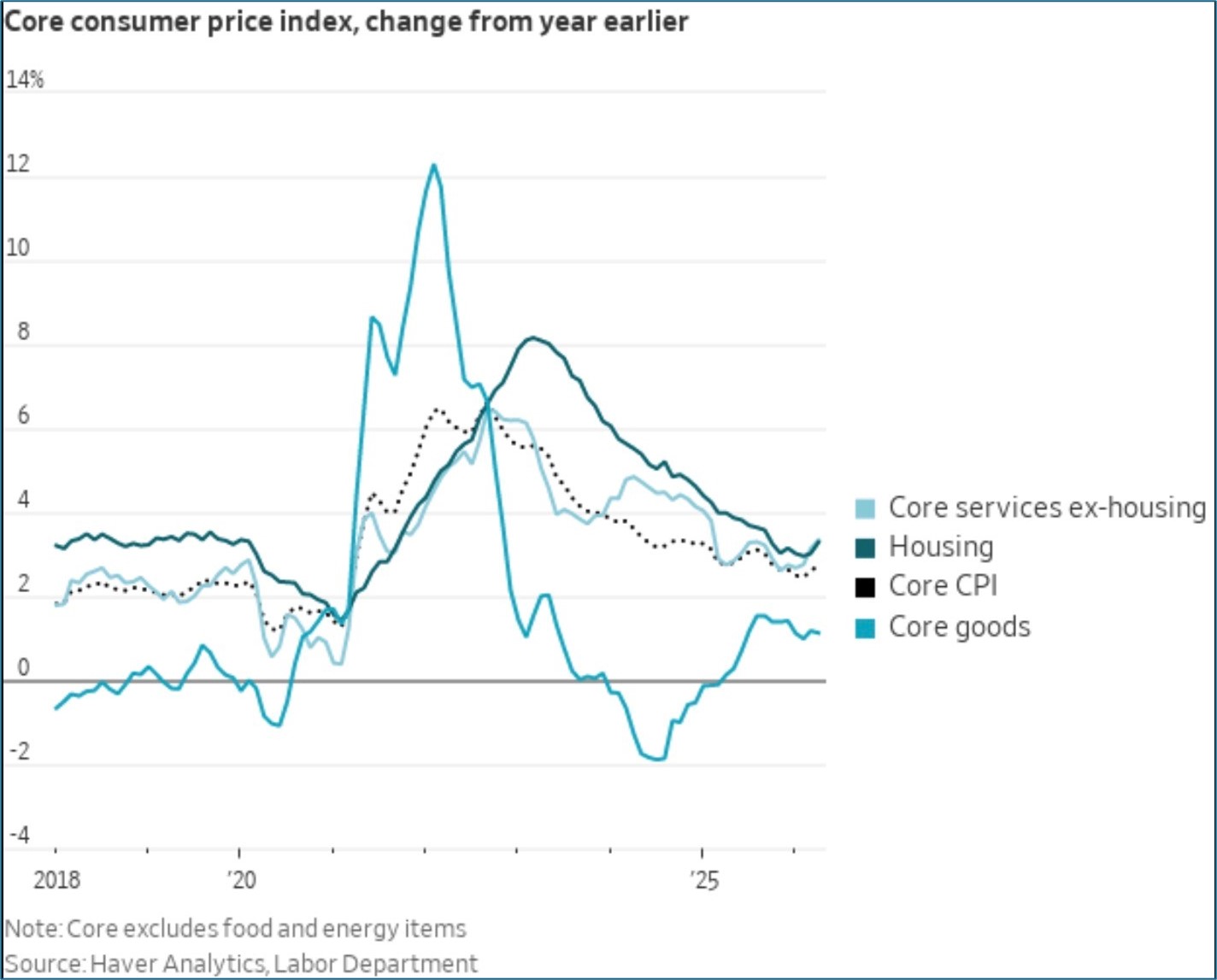

All Headed Higher Except Core Goods

Services Ex-Housing Up 0.38% MoM and 3.4% YoY – Higher Energy Costs Apparently Leaking into Other Areas

Source: BLS

Food at Home Up 0.68% MoM in April – Groceries Quick to Reprice Higher

Source: BLS

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.