April Jobs Report Beats Expectations, Unemployment Rate Unchanged

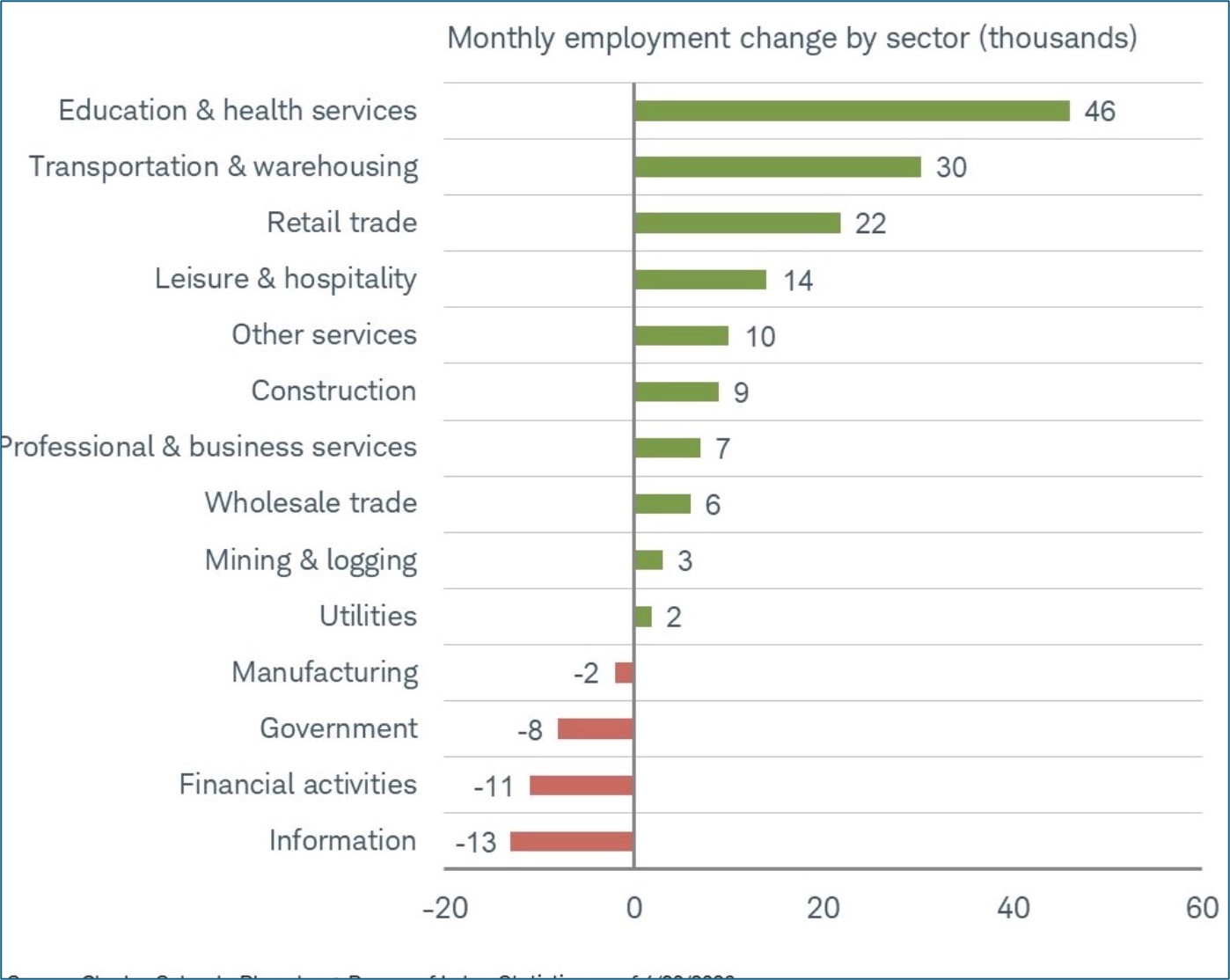

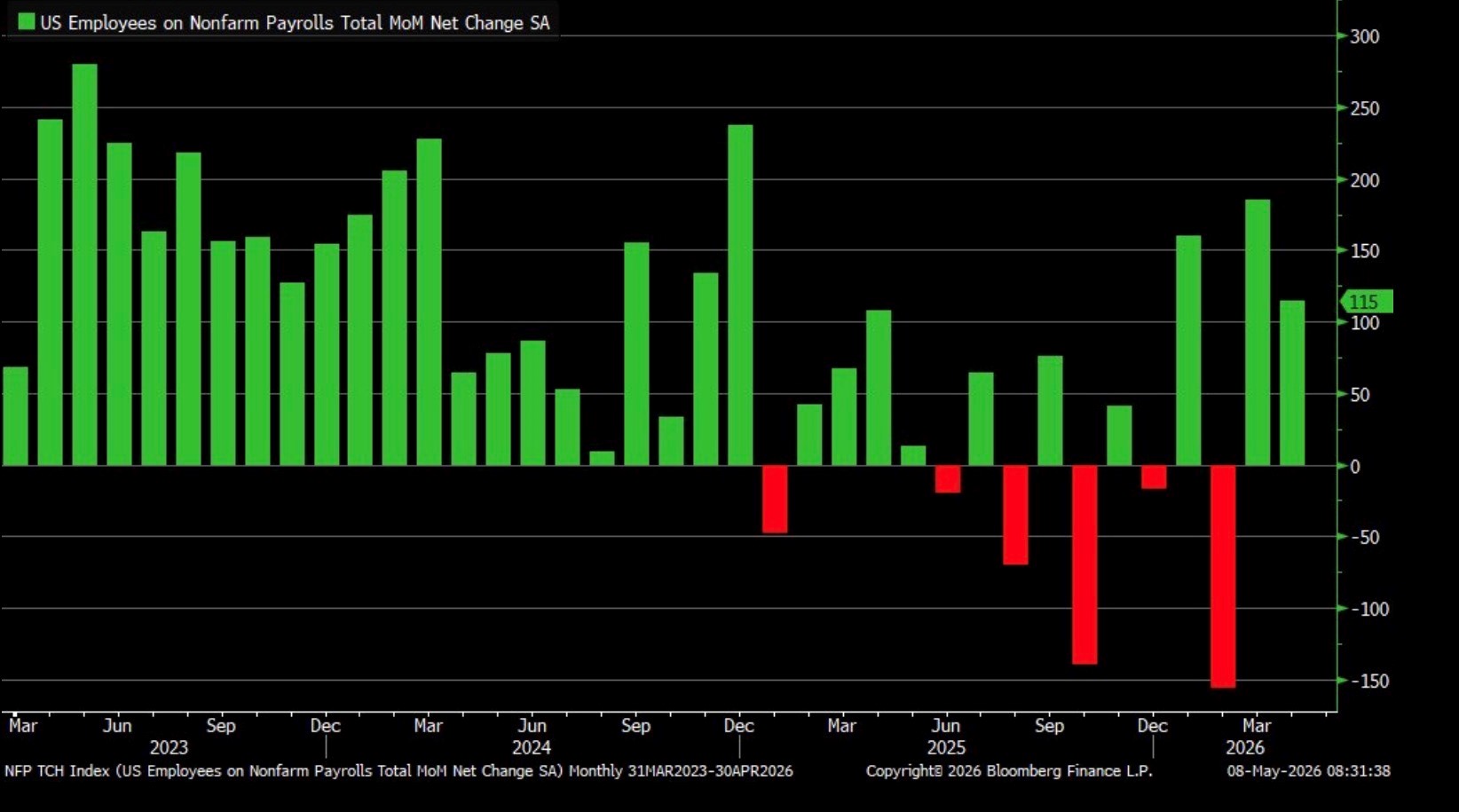

- April nonfarm payrolls rose 115 thousand, easily beating the 65 thousand expected but less than the 185 thousand gained in March (revised higher from an initial 178 thousand). Two-month revisions cut 16 thousand jobs from previous estimates. The March bounce wasn’t entirely surprising given February weather issues along with a healthcare worker strike, so for April, a return to job gains in the 100 thousand range seems to be the current run rate for the economy. Job gains remained strong in areas that we’ve come to expect, namely healthcare (+46k), and transportation/warehousing (+30k). On the other hand, the federal government continued to shed jobs with 9k lost during the month.

- The Household Survey is smaller than the Establishment Survey and subject to more volatility, but it generates the important unemployment rate, labor force participation rate, etc.. The survey reported a decrease of 92 thousand people in the labor force (those employed and those not working but actively looking for employment) and a 134 thousand increase in unemployed persons. You can read that as nearly 100 thousand people left the workforce, and now not counted, yet, the number of unemployed increased. The unemployment rate remained at 4.3% (4.34% unrounded vs. 4.26% in March), for a second straight month, but the granular details point to a slight weakening vs. March. The small drop in the labor force follows a slightly larger decline in March, which if it continues will become a concern. The labor force decrease led to a downtick in the Labor Force Participation Rate from 61.9% to 61.8%.

- Many Fed officials have referenced the stability in the unemployment rate as evidence of overall labor market stability, so an unchanged rate, on the surface, conforms with that stability picture. That said, a shrinking labor force and increase in the number of unemployed, albeit slight, is not the type of stability I think the Fed is looking for, and that’s one takeaway from today’s report.

- Meanwhile, Average Hourly Earnings rose 0.2% MoM, missing the 0.3% expectation but matching the March gain. The year-over-year pace increased one-tenth to 3.6%, but that missed the 3.8% expectation. Average weekly hours increased a tenth in April to 34.3 hours reversing the drop in March. Bottom line, with YoY wage gains stabilizing, and hours worked slightly increasing, the consumer continues to have spending power to drive the economy into the summer travel season. How they handle those elevated gas prices may be another matter!

- In summary, today’s release confirms other recent employment-focused reports received this week (ADP, JOLTS, ISM, Jobless Claims) that painted a picture of employment momentum holding steady, and importantly not indicating a new leg lower. The healthcare sector remains the leading job gainer while government jobs continue to contract.

- Bottom line: with solid job growth, a stable unemployment rate, and stable wage gains, the Fed can remain patient and wait for the inflation picture to improve. While one can pick at the slight increase in unemployed and slight decrease in the labor force, the overall picture of stability remained, at least for April. The energy price spike will start to spread into other sectors in upcoming inflation reports and that will create a challenge for the Fed as they wait on supply constraints through the Strait of Hormuz to ease, and even when that happens it will take months to return to pre-war conditions. Thus, the inflation/growth question will continue dominating trading into the summer with the market expecting a Fed on hold into 2027, and that expectation will not be altered by today’s jobs report.

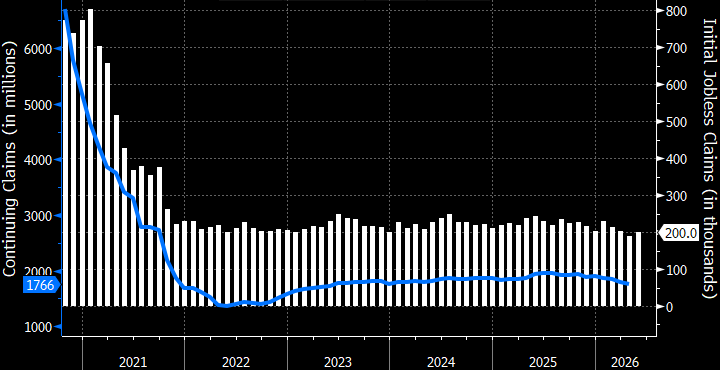

- Finally, initial jobless claims and continuing claims continue with the low-fire theme even as hiring appears to be stable. Initial claims for the week ending May 2 rose from 190 thousand to 200 thousand. The 4-week average ticked lower from 207.75 thousand to 203.25 thousand. Continuing claims for the week ending April 25 fell 10k from 1.776 million to 1.766 million. As the graph below shows, however, little has changed between the two measures for months now as companies have slowed hiring but they remain content to hang onto employees through the current war-induced uncertainty.

Healthcare Continues to Dominate New Hires Source: BLS

Source: BLS

Monthly Change in Nonfarm Payrolls – Over 100K for Second Straight Month

Source: BLS

Initial and Continuing Jobless Claims – Continue to Reflect the Low-Fire Environment

Source: Dept. of Labor

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.