Back to Focusing on the Middle East

- The China Summit is over and with little in the way of substantive wins, the focus this week returns to the Middle East situation. The data calendar obliges by being rather dull, so the market will take direction from the strength or weakness in Treasuries and any new Middle East developments. The highlights for the limited calendar include the FOMC minutes on Wednesday and a preliminary look at May PMIs on Thursday. Meanwhile, yields are at or flirting with yearly highs as oil prices move up yet again. Currently, the 10yr is yielding 4.59%, and were up to 4.63% in earlier trading, while the 2yr is yielding 4.07%, the highest in a year.

- After last week’s onslaught of hot inflation reports, and a retail sales report that while not hot was warm to the touch, this week the pace slows considerably and will be dominated more by how the market trades and a return to Middle East headlines. The President’s trip to China didn’t result in any groundbreaking news other than some pre-organized deals for Boeings, beef, and beans but the amounts are modest for two global powers.

- One report this week that may get some attention will be Thursday’s S&P Global Preliminary PMIs for May. Last month, the Manufacturing PMI printed at 54.5, the Services PMI at 51.0, and the Composite at 51.7. Those levels will be compared to the latest findings in addition to the level of prices paid, employment and new orders in each category. Continued price pressure and any indication of weakening orders and/or employment will be early yellow if not red flags.

- Another report that will get market attention will be the FOMC Minutes from the April 29th However, with the inflation news from last week, any discussion of possible rate cuts will be put aside, and instead, the minutes will be scoured for hints of any serious thought as to rate hikes. With new Fed Chair Kevin Warsh set to preside over the June meeting, his rate-cutting mandate is on life support and he’s probably smart enough to not push that out of the box. Look for his initial push to be in a messaging shift (perhaps a reduction in forward guidance, including the elimination of the controversial Dot Plots.

- He may also focus on his other major point of contention with the Powell-led Fed and that is shrinking the Fed’s balance sheet. He has made that a key point of the Warsh Agenda but even there he may face pushback. Fed Governor Michael Barr spoke last Thursday in New York and had this to say about possible balance sheet reduction: “I think shrinking the balance sheet is the wrong objective, and many of the proposals to meet this objective would undermine bank resilience, impede money market functioning, and, ultimately, threaten financial stability. Some would actually increase the Fed’s footprint in financial markets.” His concluding comment was this, “In any consideration of a change in the Federal Reserve’s approach to managing its balance sheet, we ought to go back to basics and ask what problem we are trying to solve. In sum, shrinking the Fed’s balance sheet is the wrong goal, and reducing the resilience of the banking system is the wrong means.”

- Looks like the new Fed Chair is going to have some work to do to bring the committee around to his key priorities: rate cuts and balance sheet reduction. It could be a rough start for him, fortunately, monetary policy seems fixed in place for now, which allows Warsh time to work the room for future agreements.

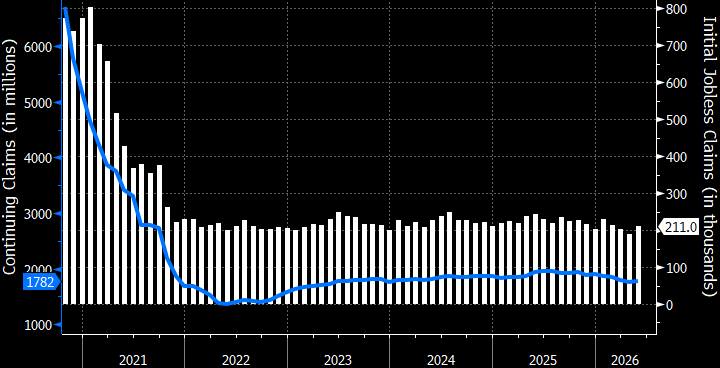

- Away from possible Fed drama, the weekly jobless claims report is another one that will garner attention as the Fed looks to the labor market for continued stability that will give them time to see improvement on inflation. Last week’s initial claims increased 12 thousand but that still leaves it historically low and it has been remarkably stable in the low 200 thousand level for months. The Fed will be hoping that continues while time and higher market rates begin to deflate the recently expanding inflation balloon.

- Finally, last week we made a couple presentations with an updated economic outlook for the balance of this year and into early 2027. Spoiler alert, we see GDP growth slowing this year (1.5% to 2.0%) but avoiding a recession (although those risks are rising). Inflation will trend higher but remain below levels requiring rate hikes. Healthcare job growth and data center buildout will keep the economy limping along enough to prevent the Fed from cutting rates this year. The major caveat there is that we avoid a major equity market correction that dents the wealth effect and slows the middle-to-upper income consumer. Then, all bets are off. You can access the slide deck here.

Initial and Continuing Claims Have Been Remarkably Stable for Months – the Fed Hopes this Continues Source: Dept. of Labor

Source: Dept. of Labor

30Yr Treasury Bond Yield Hit 20yr High – Does the run to Higher Yields Continue This Week? Source: CNBC

Source: CNBC

Fed Funds Futures for December are all About Rate Hikes Now Source: CME Group

Source: CME Group

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.