Consumers Say Jobs Increasingly Harder to Find

- President Trump’s first State of the Union Address in his second term was a longwinded affair, longest ever actually, but it didn’t break new ground and didn’t relent from tariffs being a centerpiece of trade policy, despite last week’s Supreme Court ruling. Of the 1 hour 45-minute speech, 8.5% was spent on national security, 6.6% on crime, 5.8% immigration, 4.8% Venezuela and 4.2% the economy. Given that ranking, it’s perhaps not surprising that markets this morning are mostly where we left them yesterday. Currently, the 10yr is yielding 4.06%, up 2bps, while the 2yr is yielding 3.48%, also up 2bps on the day.

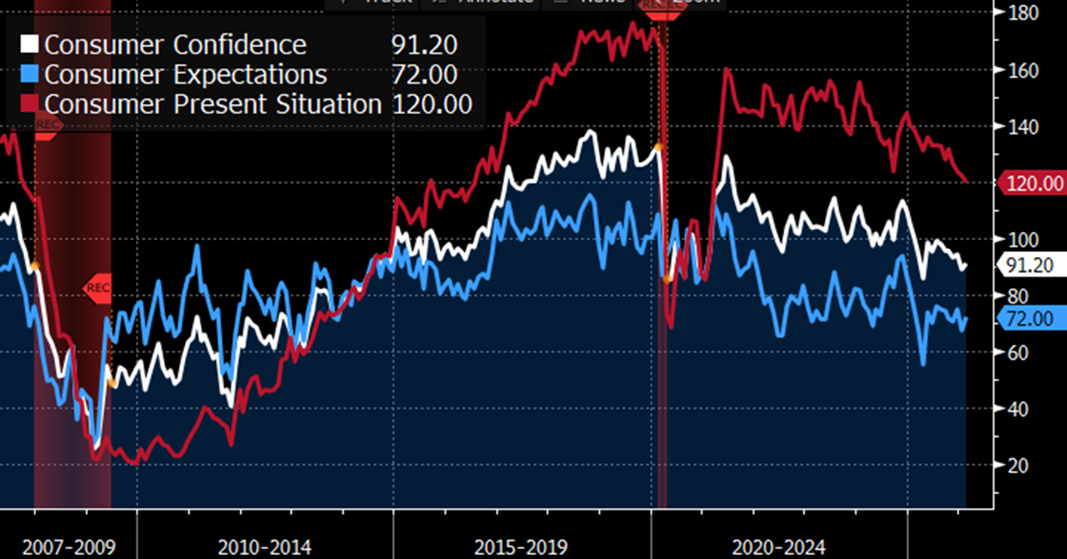

- Turning to other news, while it’s admittedly a slow week for economic releases, the highlight was probably yesterday’s Conference Board Consumer Confidence Survey for February. Overall confidence increased from 89.0 to 91.2 but the Present Situation metric ticked lower from 121.8 to 120.0 while Expectations improved slightly from 67.2 to 68.6. Despite the modest improvement, consumer outlooks remain below year ago levels (see graph below).

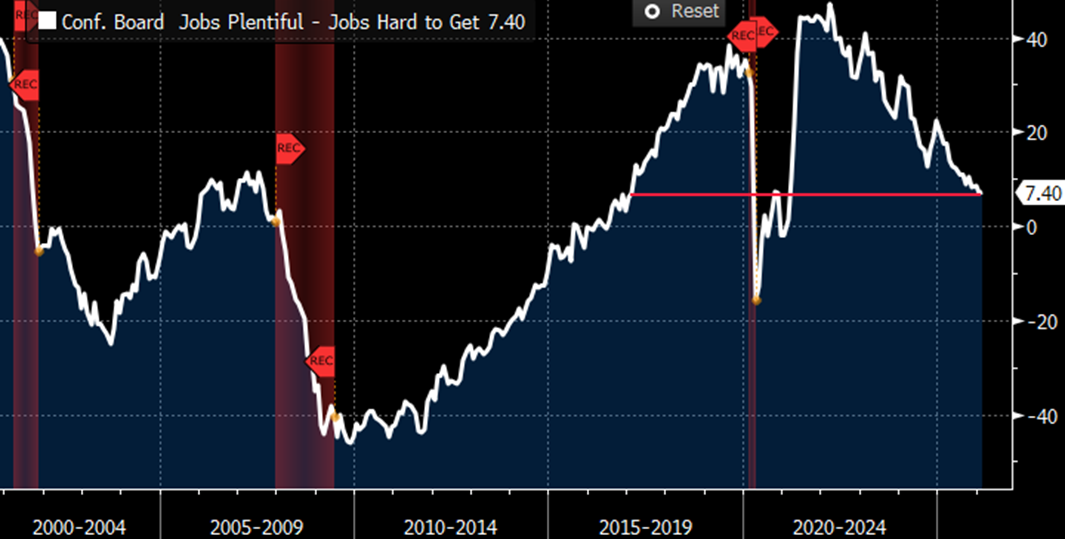

- The key metric we’re interested in is the so-called Labor Differential, which is the difference between respondents finding jobs plentiful minus those saying jobs are hard to get. While that differential improved slightly it remains in a multiyear downtrend and except for the pandemic/shutdown period is at the lowest reading since 2017. In fact, the Jobs Hard to Get metric hit a post-pandemic high this month (see graph below). The difficulty in finding a job may be increasing but until the unemployment rate starts to move higher this reading alone won’t be enough to move the Fed into cutting rates sooner rather than later.

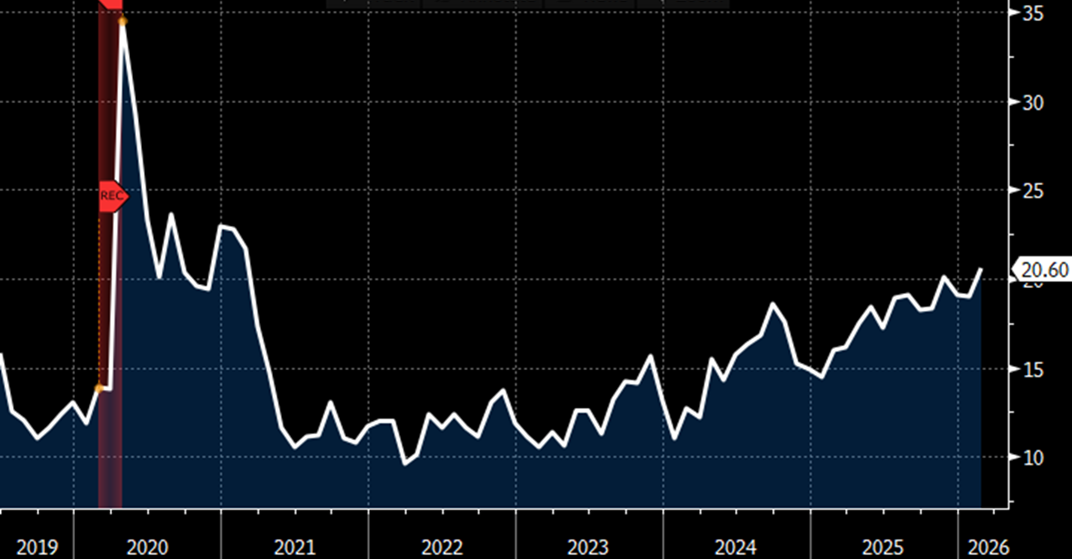

- Another report from yesterday, however, painted a slightly more optimistic picture of the labor market according to the weekly National Employment Pulse Report from ADP. For the four weeks ending February 7, private employers added an average of 12,750 jobs per week. It was the fourth straight week of strengthening job gains (see graph below).

- While these numbers are preliminary and could change as new data is added it speaks to a labor market generating jobs in the 50 thousand per month range. Assuming little change in government jobs, that would be enough to keep the unemployment rate steady as the new level of labor market equilibrium is estimated in the 40 to 60 thousand range, given the slowing in population growth. So, while labor market momentum has undoubtedly slowed from earlier years, the Fed has identified the unemployment rate as a key metric in measuring labor market stability. That is, if the unemployment rate is steady, despite a slowdown in job creation, the Fed is inclined to wait for inflation to move lower before resuming rate cuts.

- Meanwhile, the residential housing market continues to plod along with little improvement. The S&P Cotality Case-Shiller U.S. National Home Price Index posted a meager 1.3% annual gain for December 2025, down from 1.4% in the previous month. Interestingly, geographic divergence widened with Chicago and New York leading all markets with gains above 5%, while Tampa, Phoenix, Dallas, and Miami posted the steepest declines among markets that finished the year in negative territory. Former leaders in price appreciation are now trailing while former laggards are now on top.

- For the year, national home prices grew by just 1.3%, the weakest full-year gain since 2011, when prices fell 3.9%, and 5.3 percentage points below the 6.6% 10-year annual average. Even excluding 2021’s near-20% Covid-era surge, the 10-year average annual gain stands at 5.2%, still 3.9 percentage points ahead of this year’s result. With mortgage rates moving closer to 5-handle range the bottom may hopefully be near (see graph below).

- Fed speak was heavy yesterday. First, Boston Fed President Susan Collins (non-voter), said that the Fed is ‘quite likely’ to hold rates steady for some time. Second, Fed Governor Lisa Cook (voter) said, “If AI continues to raise productivity, economic growth could remain strong, even as churn in the labor market leads to an increase in unemployment. In a productivity boom such as this, a rise in unemployment may not indicate increased slack.” Third, Chicago Fed President Austan Goolsbee (non-voter) said, “The dynamic of low hiring, low firing — which I believe came from business uncertainty — is made even more solidified by adding more uncertainty. That said, it could bring relief to the inflation side.” That’s a reference to tariffs perhaps receding in importance following the Supreme Court ruling.

Consumer Confidence Improves Slightly in February but still Tracking Low

Source: Conference Board

Labor Differential (Jobs Plentiful – Jobs Hard to Get) Still Points to a Rough Market for Job Seekers

Source: Conference Board

Jobs Hard to Get – Hits a Post-Pandemic High, Frustrating Job Seekers

Source: Conference Board

ADP’s Weekly Report of New Private Sector Jobs Improved for 4th Straight Week

Source: ADP

Bankrate National Average for 30Yr Mortgage – Nearing 6.00% Source: BankRate

Source: BankRate

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.