Early Tremors in Equity Land?

- Some selling in the high flyers of the equity world benefited Treasuries as a flight to safety trade was evident yesterday. The equity selling started in Asia, with the Korean Index down a solid 10%. While selling followed around the globe, it didn’t match the Asian intensity. For now, thoughts that a severe market correction may finally slow consumption will have to wait for another day, but just like in geologic-terms, initial tremors are usually followed by more. Today doesn’t offer much in the way of new data, so it may be again the case of following clues in the equity markets, oil prices, and geo-political news. Tomorrow brings May PCE numbers which will re-focus fixed income investors on matters closer to home. Currently, the 10yr is yielding 4.45%, down 5bps, while the 2yr is yielding 4.17%, down 3bps on the day.

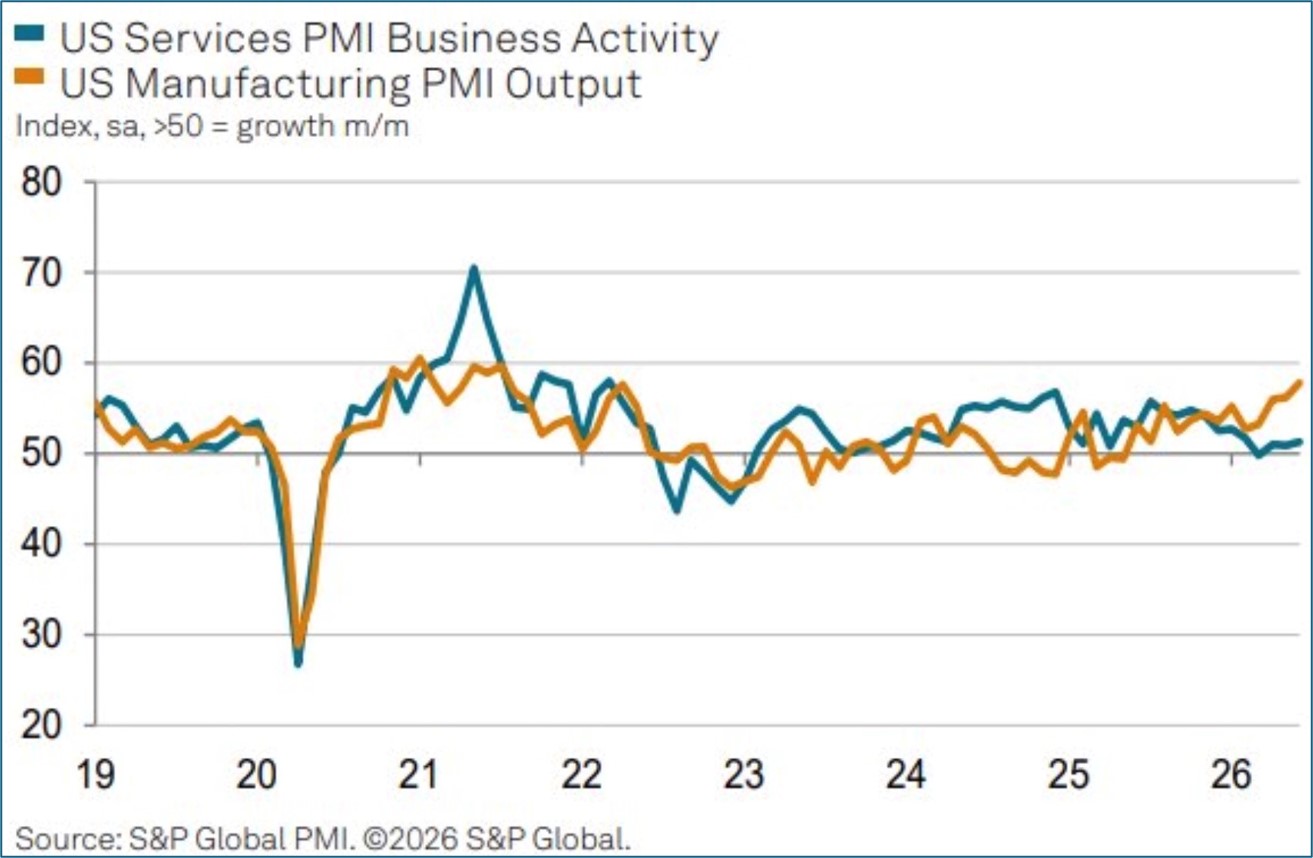

- Yesterday, brought us the first look at June activity with the S&P Global Preliminary PMI readings. While it’s not as famous as the ISM series it is a quality report that warrants attention before next week’s ISMs. US business activity growth improved for a third successive month in June; however, the rate of growth remained weaker than at the start of the year. Companies also cut back on their staffing levels amid concerns over the outlook and in response to rising costs, notably in raw materials. Input price inflation cooled a bit but remained historically high, leading to an unchanged elevated rate of selling price inflation. The survey also showed an unbalanced economy, as sluggish demand for services contrasted with historically strong growth in demand for manufacturing goods, although the latter was again supported by precautionary stock building amid increasingly widespread supply issues.

- The Manufacturing PMI rose from 55.1 to 55.7 in June, the highest since May 2022. Growth accelerated as new orders showed the largest rise since April 2022. Input inventories posted the largest rise since May 2025, and the second steepest in survey history. The greatest lengthening of supplier delivery times since August 2022 also contributed positively to the PMI. However, weighing on the PMI was the sharpest fall in employment since May 2020.

- Although notching its largest increase in business activity since February, buoyed in some cases by the soccer World Cup, the service sector again reported only a modest increase in both output and new orders. The headline reading increased from 50.7 to 51.3. Service providers cited elevated prices, higher interest rates, and low confidence among both business and consumer customers as limiting factors in activity.

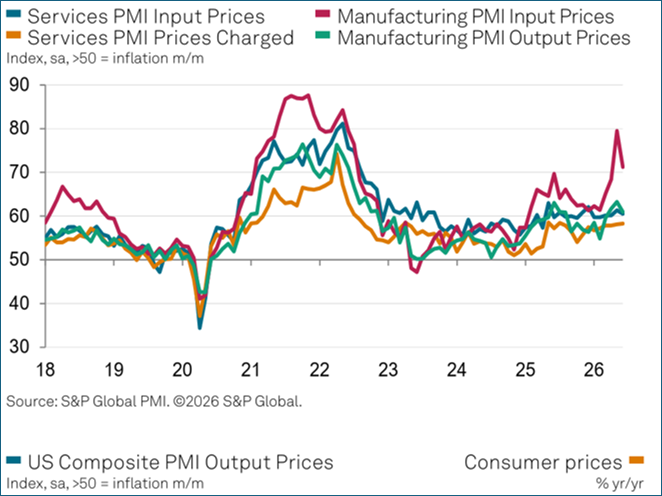

- Average input prices meanwhile rose to the third-highest recorded since the start of 2023. Although manufacturing input cost inflation moderated from May’s recent peak, it was the second highest in nearly four years. Services input cost inflation meanwhile edged up to a six-month high. Meanwhile, employment fell for a second month in a row, and for the third time in the past four months, as companies continued to focus on cost reduction amid high input prices and concerns over the outlook. While only a modest drop in services jobs was reported, manufacturing headcounts were cut at the fastest rate since the COVID-19 lockdowns of early 2020.

- Expectations in both the manufacturing and services sectors improved to the brightest since February, with the improved outlook partly linked to hopes of an easing of war-related disruptions and price pressures. However, sentiment nonetheless remained well below long-run averages which points to subdued overall business confidence, with blame often placed on the economic uncertainty relating to the ongoing impact of the Iran war and policies such as tariffs.

- Also released yesterday, ADP reported that for the four weeks ending June 6, 2026, U.S. private employers added an average of 30,750 jobs per week. It was the first hiring pickup since May 2. This early read on June employment indicates ADP should report next week’s monthly private sector job growth to be in the neighborhood of May’s 122 thousand. That report will be released on Wednesday, July 1, with the BLS Nonfarm Payrolls Report the following day. That report is expected to find 110 thousand new overall and private sector jobs in June. That would be a slightly slower pace of job growth than the past few months, but it should be enough to keep the unemployment rate unchanged at 4.3% and allow the Fed to remain firmly focused on its price stability/inflation mandate.

Manufacturing Sector Strength Continued in June While Services Activity Held Just Above 50 Source: S&P Global

Source: S&P Global

S&P Global Preliminary June PMIs – Input vs. Output Prices: Suppliers Eating Some Costs for Now Source: S&P Global

Source: S&P Global

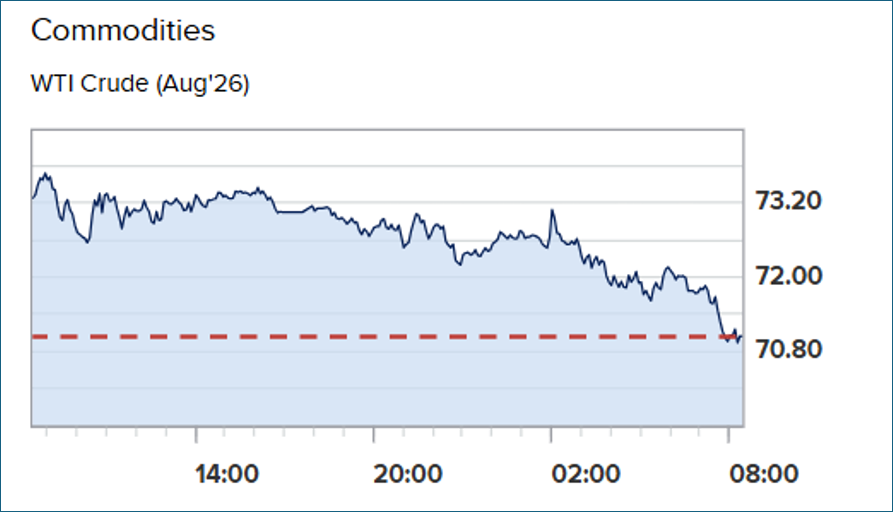

Oil Prices Continue to Move Lower (Nearing $70/bb) – The Consumer May Soon See More Relief at the Pump Source: CNBC

Source: CNBC

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.