Eyes on CPI and Persian Gulf this Week

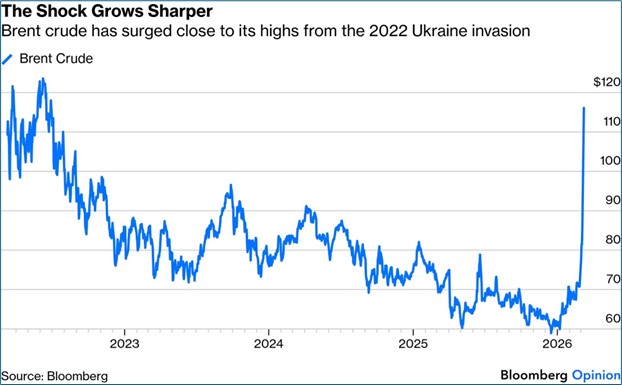

- Friday’s big miss on jobs and lackluster January retail sales didn’t provide the spark for a Treasury rally as investors took the confusing jobs report and decided to worry more about inflation risk from the Iran war that weekend events showed is not going away anytime soon. Oil surging 70% in one week will do that and the longer it sticks, the more a temporary price impact will be revised into a more permanent higher cost structure that will impact the Fed’s monetary policy decisions. So, despite a CPI and PCE inflation update this week, the story may be more about what will the inflation picture look like in a few months, not so much today. Currently, the 10yr is yielding 4.17%, up 4bps, while the 2yr is yielding 3.60%, also up 4bps on the day.

- Iran has chosen a new leader, and it’s Mojtaba Khamenei, son of the slain former supreme leader. Meet the new boss, same as the old boss. This isn’t actually regime change, nor is it the choice of a country looking to appease its enemy and seek an off-ramp. That contributed to a sharply lower trade in Asia. Brent crude rose as high as $118 in overnight trading and is currently in the $104 range, up 35% for the week and a 4-year high. In Japan, the Nikkei 225 was down 5% and the Korean Kospi down 6%.

- The initial kneejerk fear in markets has been the inflationary impact of higher oil prices, but those higher prices also act as a dampener on demand the longer they stay at elevated levels. For now, the market isn’t focused on that but given the last two so-so retail sales reports, it could soon be part of the calculus. For now, however, markets are pricing in the prospect of higher inflation, as a result, some risk-off trading is taking place in equities (Dow futures indicated 470 points lower) and longer-term debt in the form of higher yields. The next step may be a repricing lower of consumer consumption expectations and then we’ll get into the recession vs. stagflation scenarios.

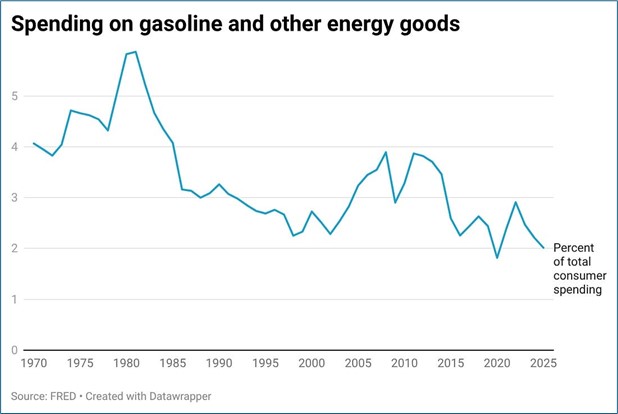

- The good news is we spend much less per capita today on gas (see graph below), and inflation expectations are better anchored today vs. prior oil shocks, so that may factor into the recession vs. stagflation set-up. Nevertheless, the latest developments have the next rate cut being pushed into the September FOMC meeting.

- After last week’s data deluge in the midst of the geo-political machinations, there’s no rest for the weary with February CPI set for this Wednesday. Expectations are for both headline inflation and core (ex-food and energy) to increase 0.2% MoM with the YoY headline rate unchanged at 2.4%, and core from 2.5% to 2.4% as more benign 0.2% MoM February 2025 prints roll out of the calculations (as opposed to 0.5% and 0.4% Jan. 2025 numbers last month). And that’s the bad news in that subsequent months will see a string of 0.1% and 0.2% monthly prints roll off. Thus, further YoY gains will be hard to come by and that’s before we consider the add-on impact of higher oil and commodity prices coming from the Iran war. Thus, just maintaining mid-2% YoY inflation numbers will be a challenge in the coming months.

- The inflation fun doesn’t stop there as we’ll get the January Personal Income and Spending Report on Friday. Recall, the BEA has been trying to catch-up from the government shutdown in October and this January print is part of that story, Stale though it may be, it is the Fed’s preferred inflation measure and expectations are for overall PCE to increase 0.3% with the YoY pace unchanged at 2.9%. Core PCE is expected to post a solid 0.4% MoM increase with the YoY rate unchanged at 3.0%. Just like the CPI series, January, and February 2025 monthly prints of 0.31% and 0.45% will shift to a string of 0.2% prints so any improvement in the YoY pace will likely only happen by the end of this quarter . After that the comparisons get tougher, and the higher costs from the Iran war will be expected to appear in the results.

- Given the back-to-back underwhelming results from the Retail Sales Report (Dec. and Jan.), the personal spending numbers from the PCE report will be important as well. It’s a broader and inflation-adjusted look at spending with nominal expected to increase 0.3% meaning real spending is likely to come in flat, or unchanged. Similar to the Retail Sales series and not a good look at the opening month of the year for the consumer.

- Also on Friday will be the University of Michigan’s preliminary Sentiment reading for March. Expectations are for a slight improvement from 56.6 to 57.0. The report will also provide a view on Current Conditions and Expectations (both 56.6 in Feb.). Perhaps more importantly, year-ahead inflation expectations are expected to be unchanged at 3.4%, tied for the lowest reading since January 2025. The expected reading still exceeds those seen in 2024 and remains well above the 2.3-3.0% range seen in the two years pre-pandemic. Long-run inflation expectations are also expected to be unchanged at 3.3%. These surveys occurred before the latest news on oil, so the results could be tossed as stale, at this point. Long-run inflation expectations that begin to move higher will be a major concern for inflation hawks at the Fed. The un-anchoring of inflation expectations during the ‘70’s oil shock did much to feed the inflation spiral then and the Fed does not want a repeat of that.

Tankers Anchored on Both Sides of the Hormuz Straits – A Lot of Watching and Waiting and not much Sailing

Source: MarineTraffic

Per-Capita Spending on Gas Much Less than Prior Oil Spikes

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.