February CPI – As Expected

- Treasuries have been taking their lead from oil markets this week and yesterday that led to a dizzying roundtrip between losses and gains as news of a US warship successfully escorting a tanker through the Straits of Hormuz brought a relief rally and drop in oil prices. Then that news was taken down and replaced with reports Iran was beginning to mine the Straits. Talk about the fog of war. While war headlines will continue to dominate trading, we do have February CPI today to distract from Middle East news. We detail the latest inflation news below. Currently, the 10yr is yielding 4.19%, up 5bps, while the 2yr is yielding 3.62%, also up 5bps on the day.

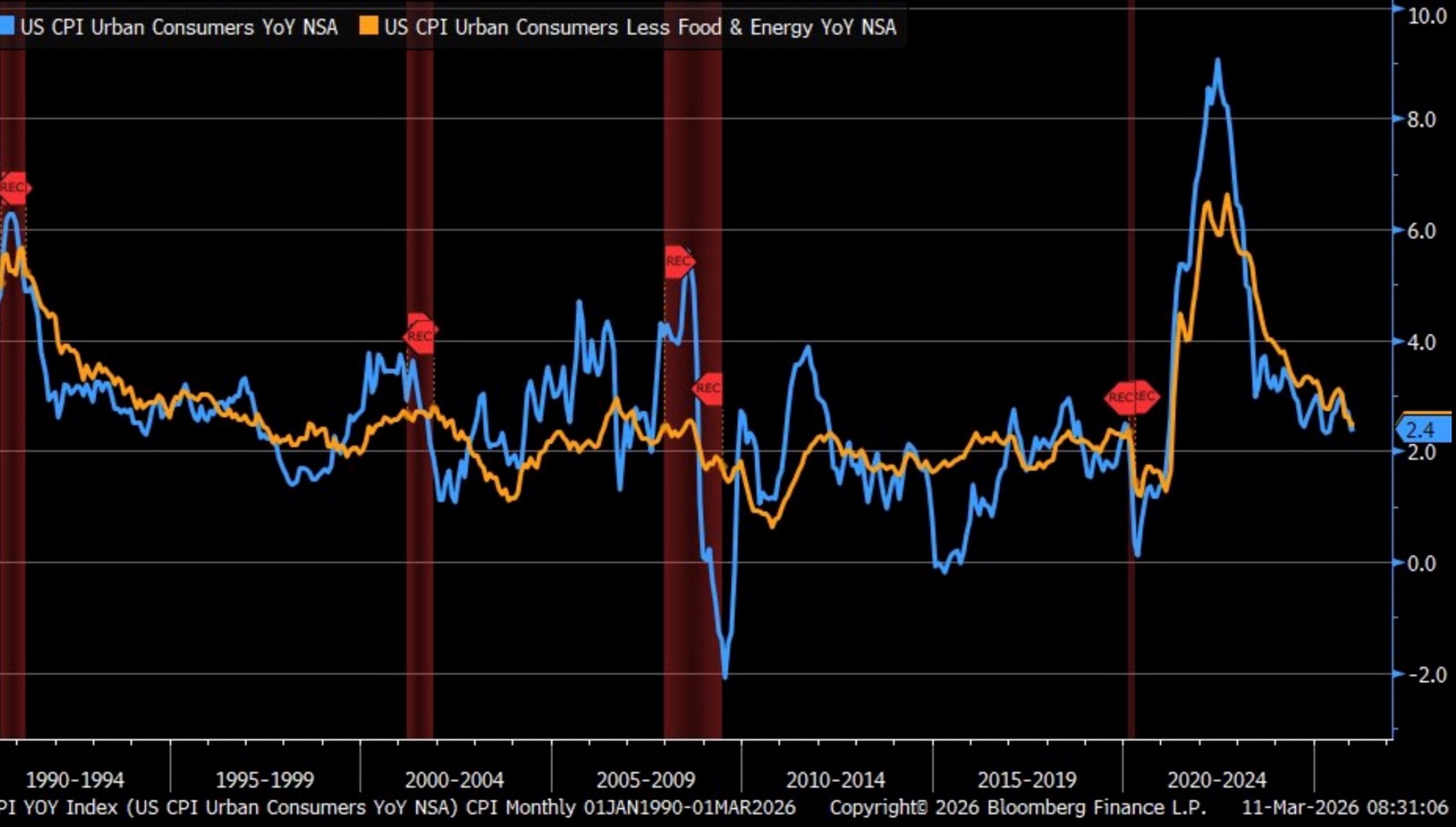

- Today’s February CPI was close to expectations, but this is all before the surge in oil prices that followed the opening salvo in the Iran war. So, exactly how much will be paid to this report? We suspect it will get its fair share of attention, especially the core number, but the bias will be that succeeding months will show signs of higher oil and supply line constraints. As for February, overall inflation increased 0.3% for the month, matching expectations with the YoY rate unchanged at 2.4%.

- Meanwhile, core CPI came in at 0.2% (0.216% unrounded) MoM, matching expectations with the YoY rate unchanged at 2.5% (2.46% unrounded), also matching expectations. The issue from here is that the next several months see a string of 0.1% and 0.2%MoM prints from last year rolling off, making it difficult for YoY rates to improve unless the new prints come in lower and that will be a challenge, especially with the surge in energy prices and the expected flow through to other items.

- Shelter costs rose 0.2%, matching the increase in January and 3.0% YoY. Meanwhile, the heavily weighted (27% of CPI) Owners’ Equivalent Rent (OER) rose 0.2%, matching the prior month. That puts it squarely in the 2.5% annual range, which is back to pre-pandemic levels. Some further improvement here is possible, but it will probably be grudging at best. One issue is the BLS decision coming out of the shutdown to roll forward pricing for 2 of the 6 geographic regions that didn’t get refreshed valuations in October and November. Thus, while the notoriously lagging OER is squarely in a downward trajectory, reflecting softer rental prices from the past two years, the process was slowed due to the lack of data collection/refresh during the shutdown. The regions that weren’t updated last fall will be adjusted in April and May, so another downtick may be possible when those updates take place.

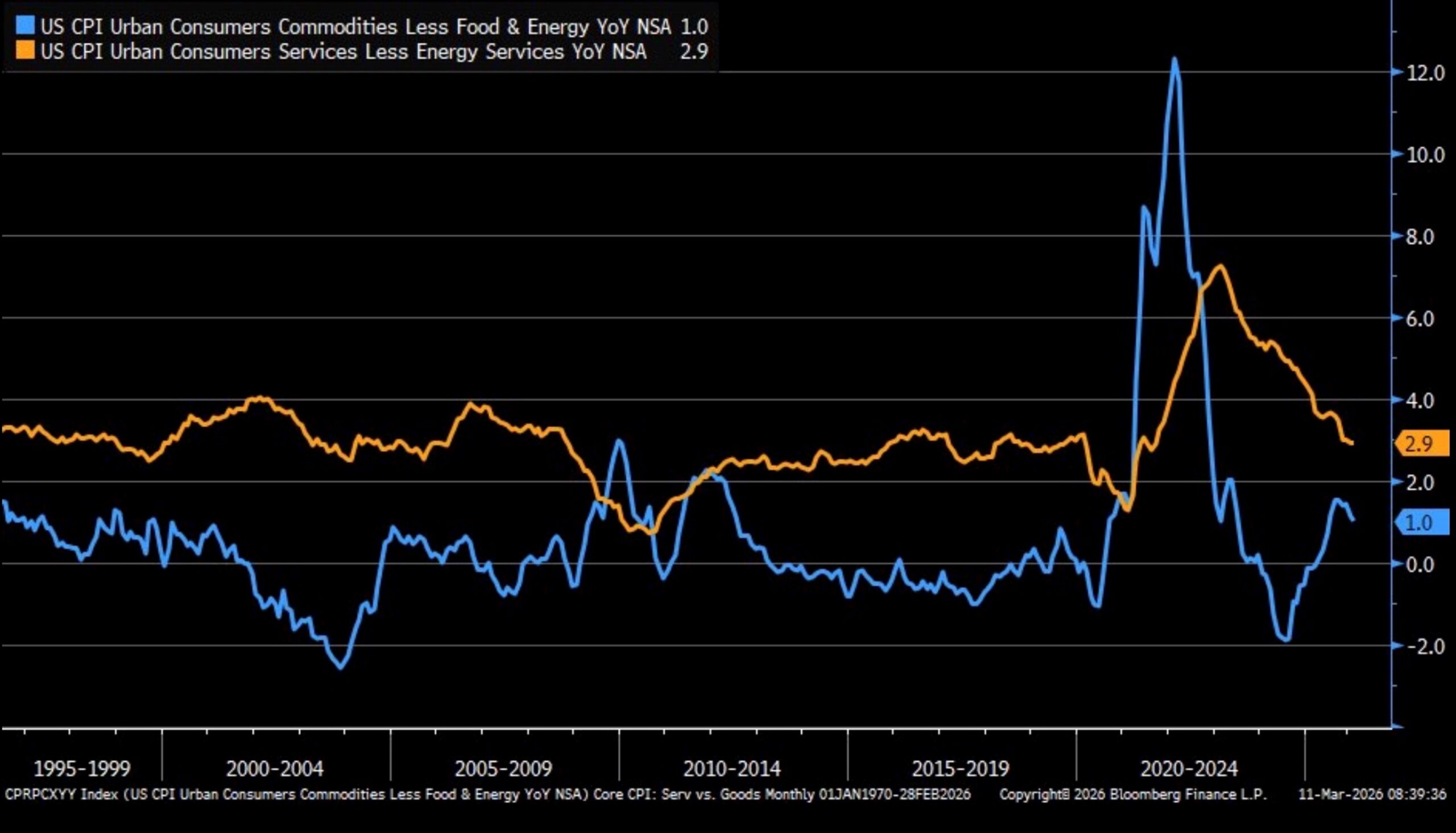

- Another lingering concern, prior to the oil price concern, is core services have been sticky high of late. For February, core services rose 0.3% vs. 0.4% in January. YoY the level is 2.9%.With a combined weighting of 61% in CPI, it needs to fall to the 0.2% monthly range for headline inflation to continue trending towards 2.0%. Core goods were eased slightly to 1% YoY indicating pass through of tariff costs remains modest at best. Bottom line, we think the Fed refrains from cutting rates again until core services move into a steady 0.2% MoM print, or less. Given the expected uptick in energy and related costs, those sectors that were sore spots away from the energy complex will have to settle down to encourage the FOMC inflation hawks to consider rate cuts.

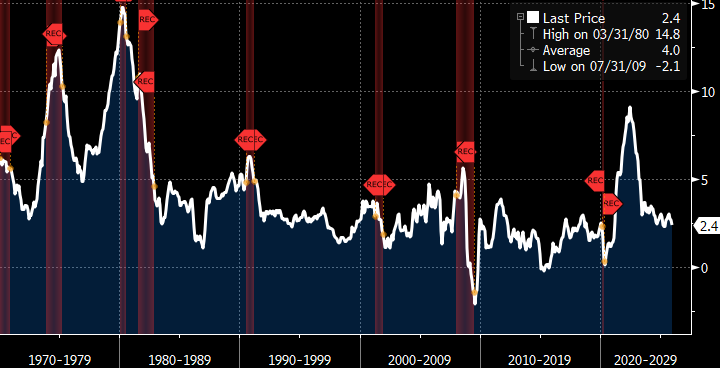

- From an inflation perspective, one of the battles the Fed doesn’t have to fight this time versus the 70’s-era oil shock is the wage-price spiral that was a big contributor to the inexorable inflation increases from that ‘70’s episode. Back then, CPI rose from a low of 5% to nearly 15% between 1976 and 1980 (see graph below). A couple things contributed to that 10% increase in inflation: (1) the US was still very dependent on imported oil, so oil-rich regimes were quick to exploit that situation with further supply constraints; (2) unions had much bigger influence than with most having cost of living adjustments (COLA) built into contracts. Thus, higher inflation begat higher wage adjustments with expectations that the cycle would persist. That was the period of “unanchored” inflation expectations, something that then Fed Chair Paul Volcker slayed with double-digit fed funds rates. That’s why we often hear from Fed officials of the necessity for policy to keep inflation expectations anchored in order to avoid a repeat of the 1970’s experience.

- Today, the US can internally supply itself with oil; thus, shortages won’t be a thing in this episode. While prices may increase given the global trading of the commodity, those are likely to be short-lived when global output returns to prior levels. There is little incentive for major producers to restrict supplies further where lower output, despite higher prices, leads to less revenue. Also, unions hold far less sway over US workers today such that the wage-price spiral of yore will not be much of a factor, if at all, in this episode. Those two changes fundamentally limit possible price increases.

- It’s still possible this episode slows the timing of rate cuts that may have been expected prior to the beginning of hostilities. The inflation hawks will want to see proof that any pass-through into core prices is limited at best. Thus, when a June rate cut was above 50% odds on Feb. 28, it sits at 38% today.

CPI and Core CPI (YoY) – Move into the mid 2% Range

Core Services Flattens in February (YoY), While Core Goods Edges Lower (YoY)

Inflation Shock from 1970’s Not Likely to be Repeated Source: BLS

Source: BLS

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.