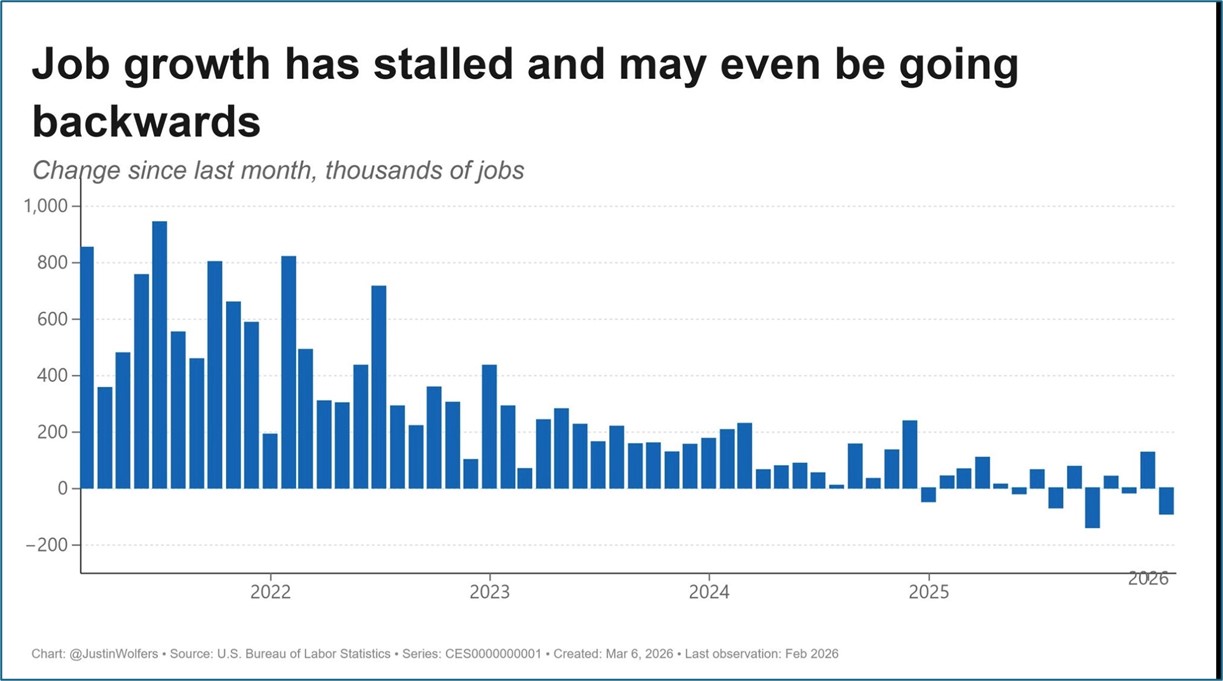

February Jobs Report Disappoints and Retail Sales Just So-So

- February nonfarm payrolls fell 92 thousand, missing by a wide margin the 55 thousand expected and 126 thousand gained in January (revised lower from an initial 130 thousand). Two-month revisions cut 69 thousand jobs from previous estimates with December revised 65 thousand lower and January 4 thousand lower. Given the level of disparity between the two months (and some population adjustments in the Household Survey impacting those numbers) our recommendation is to average the two months, and you arrive at something close to static job growth to start the year.

- The Household Survey, which is smaller than the Establishment Survey and thus subject to more volatility, generates the unemployment rate, labor force participation rate, etc.. In addition, today’s report carries the annual population benchmarking that reduced population levels and thus reduced the survey’s population and labor force numbers, unemployed, and employed. The trouble is the annual changes are lumped into December which makes a raw comparison between December and subsequent months problematic. Luckily, the BLS provides a table to show the post-population adjustments January and February and those monthly post-adjustment changes seem reasonable, but the numbers look odd compared to pre-adjusted totals. Confused? You should be and that’s why the market is mostly ignoring this report and trading the war news instead.

- The survey reported an increase of 18 thousand people in the labor force (those employed and those not working but actively looking for employment) and a 203 thousand increase in unemployed persons. Thus, the unemployment rate ticked a tenth higher to 4.4% (4.444% unrounded vs. 4.283% in January). Several Fed officials have pointed to the stability in this rate as evidence of labor market stability so an increase will light a little concern in the pause mode group, and that’s probably the key takeaway from today’s report.

- Average Hourly Earnings rose 0.4% MoM, beating the 0.3% expectation and equal to January gain. With the hourly beat, the year-over-year pace ticked a tenth higher to 3.8%. Average weekly hours held at 34.3 hours after increasing a tenth in January. Bottom line, with YoY wage gains continue to live in the mid-3% to 4% range, wage-price inflation won’t be a Fed worry as long as that YoY rate doesn’t start to edge into 4-handle territory.

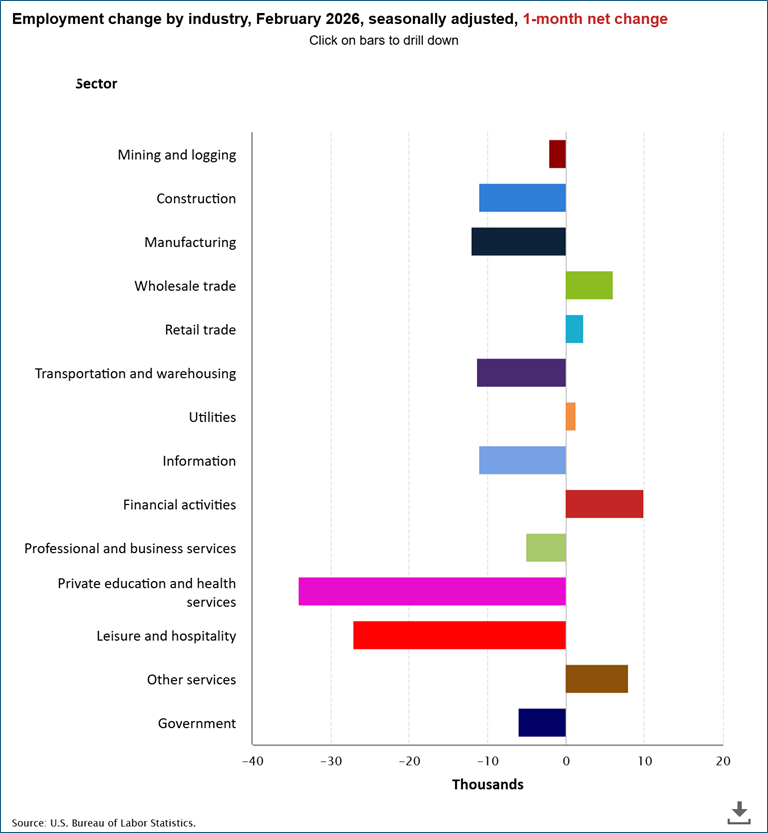

- In summary, today’s release missed expectations, which is at odds with the other employment-focused reports received this week, and the January report. The service sector finally showed some weakness losing 61K service jobs, with healthcare down 28K and doctors losing 37k, that seems truly odd). Even buildout of AI data centers seemingly slowed as construction jobs saw an 11k decrease, but weather is being blamed here.

- Bottom line: even with all the moving parts and some strange results, we can say the hiring machine that looked to have rebounded in January reversed in February, so we recommend averaging the two months together to get a pretty flat start to the labor market. The market has pretty much shrugged off this report for two reasons : (1) the adjustments in the Household Survey follow benchmarking adjustments to the Establishment Survey in January which makes the volatility between the two months even more challenging; (2) The focus is more clearly on the oil price spike and the ongoing cost/inflation concerns with the Iran war. So, with the market doing some of the Fed’s work in gently higher rates in the face of increasing inflation risk, the Fed will sit, somewhat concerned over the increased unemployment rate, but remain firmly in pause mode for now.

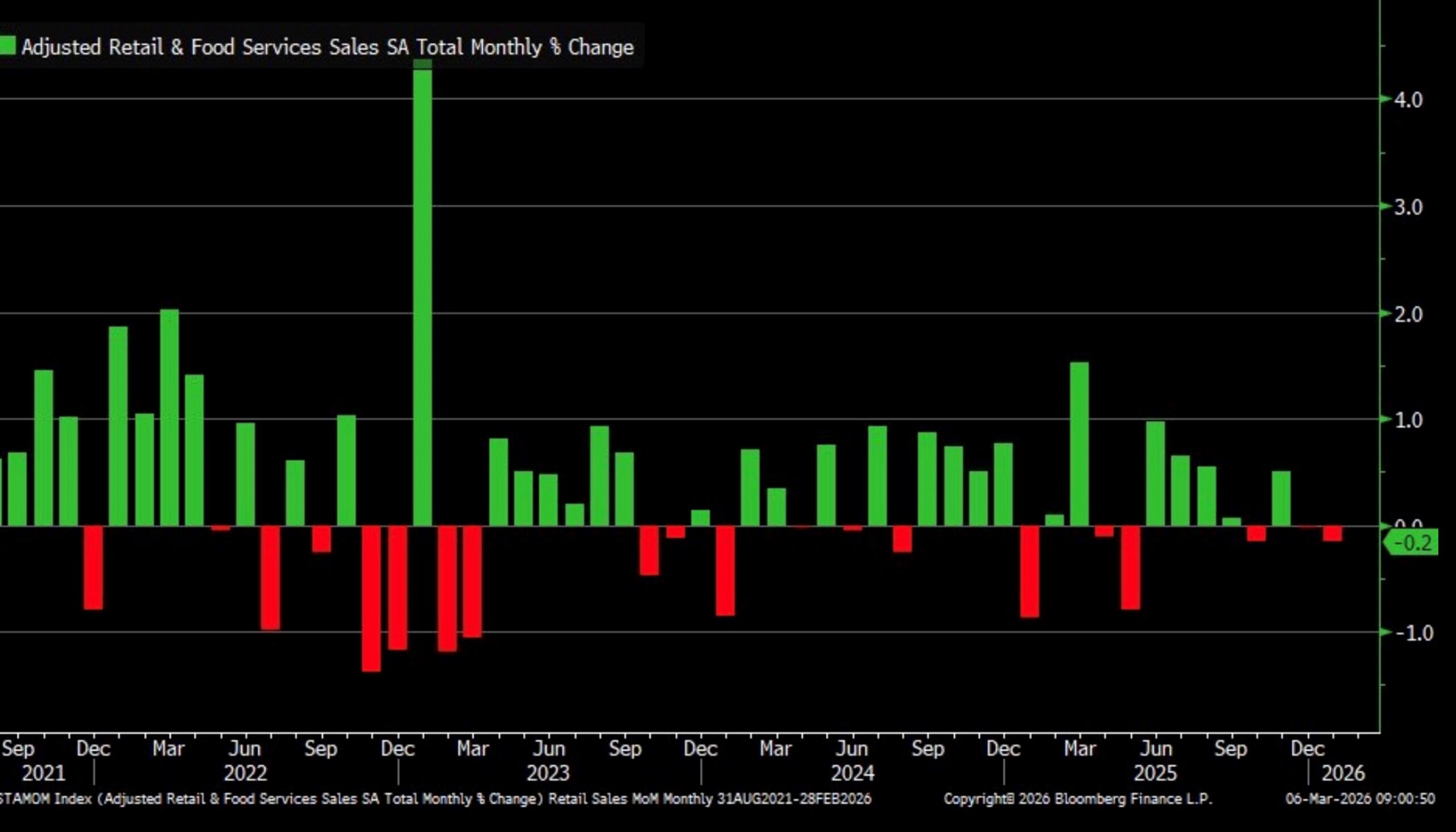

- Finally, the January Retail Sales Report was also released this morning as the government shutdown-induced backlog of reports continues to be worked down. Recall that December sales were soft so there was keen interest in assessing whether that was a single-month hiccup or something longer-lasting. Well, January retail sales painted a similar picture to December’s soft results. Advance retail sales were down -0.2% for the month vs. -0.3% expected and flat sales growth in December. Sales less autos and gas were up 0.3% vs. unchanged in December. The Control Group, a direct GDP feed, rose a decent 0.3%, matching expectations but better than the -0.1% in December. Keep in mind, this report is not inflation adjusted so an expected 0.3% increase in monthly prices effectively flattens the Control Group’s nominally impressive 0.3% gain.

- Thus, a somewhat shaky performance by the consumer to start 2026, albeit a bit better than December. The more comprehensive, and inflation adjusted, Personal Income and Spending Report for January will be released March 13, so look for this more complete read on the consumer. The December report confirmed the retail sales weakness so we’ll see if that was the case in February too.

Previous Big Job Gainers Lost in February – Seems Curious

Advance Retail Sales – Soft off Weak Auto Sales

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.