Fed Day

- The first FOMC meeting of 2026 concludes today with a rate decision at 2pm ET. Alas, the suspense on this one is nearly nonexistent. The Fed is widely expected to pause rate cuts for the first time since July, with the post-meeting Powell presser the highlight. Questions about his successor and/or the subpoena matter are likely swatted away, save for a reminder to watch his video reply. As for monetary policy, expect Powell to refer to March as a “live” meeting (data dependent, etc.), but with rate-cutting odds less than 15% it will take a dramatic downward move in either the labor market or inflation between now and March, and that’s not expected. So, while Powell may refer to the March meeting as “live”, as far as rate-cutting prospects go the meeting is on life support. Better rate-cutting odds are for June, so we’ll see how any of that shifts later today. Currently, the 10yr is yielding 4.24%, up 2bps, while the 2yr is yielding 3.57%, unchanged on the day.

- While all Fed meetings have importance, some are more important than others, unfortunately, this is not one of those meetings. With no updated dot plot, nor refreshed economic forecast, the only bit of intrigue will be the post-meeting press conference. With Chair Powell having recently prepared a video response to the subpoena affair he is not likely to re-hash those comments. Instead, we’re likely to get more of the usual Jay Powell: a steady, measured performance in which he’ll say every future meeting is “live” regarding rate-cutting potential. What the market will be after is any lean from Powell on how much weakness in the labor market is acceptable if inflation remains above 2%, which it’s likely to do for much of this year. You can expect Stephen Miran to dissent with his usual 50bps rate cut request. The question is will others join in dissent? Waller and Bowman are obvious possibilities as they’ve been making the case for months for more easing.

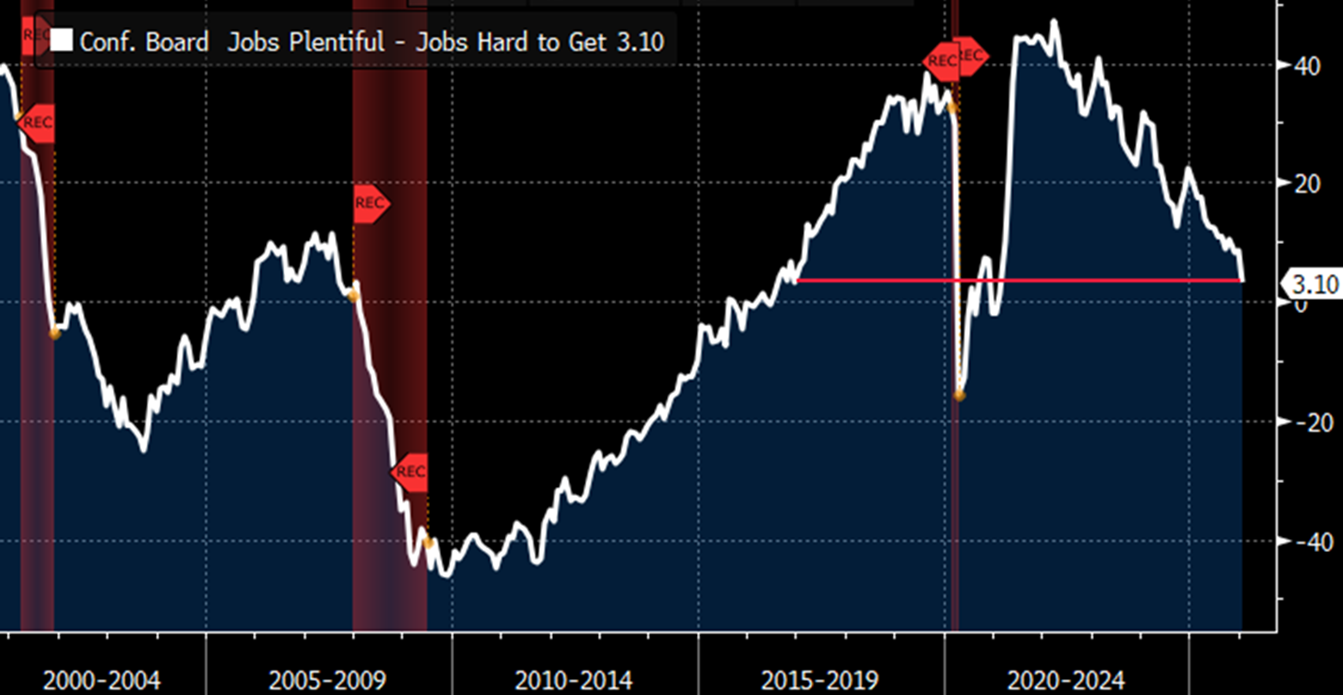

- Last Friday’s University of Michigan Sentiment Survey presented a consumer who was feeling a little better about things this month versus December. Yesterday, the Conference Board presented its January Consumer Confidence Survey and the respondents were much more pessimistic. The headline confidence reading dropped to 84.5 in January vs. 94.2 in December and 91.0 expected. That’s the lowest in nearly twelve years (May 2014). The minor measures weren’t any better. Present Situation dropped to 113.7 vs. 123.6 prior, lowest since February 2021. Expectations fell to 65.1 vs. 74.6 prior, the lowest since April 2025. Perhaps most importantly, the Labor Differential (Jobs Plentiful minus Jobs Hard to Get) fell to 3.1 from an upwardly revised 8.4 in December, that’s the lowest since February 2021, and beyond that covid-inspired weakness it’s the lowest since 2017. Overall, it was a disappointing read across the board, but dour consumer sentiment is not a new feature of this economy. The continued weakening, however, in the Labor Differential will certainly get the non-inflation hawks on the FOMC squirming some (see graph below).

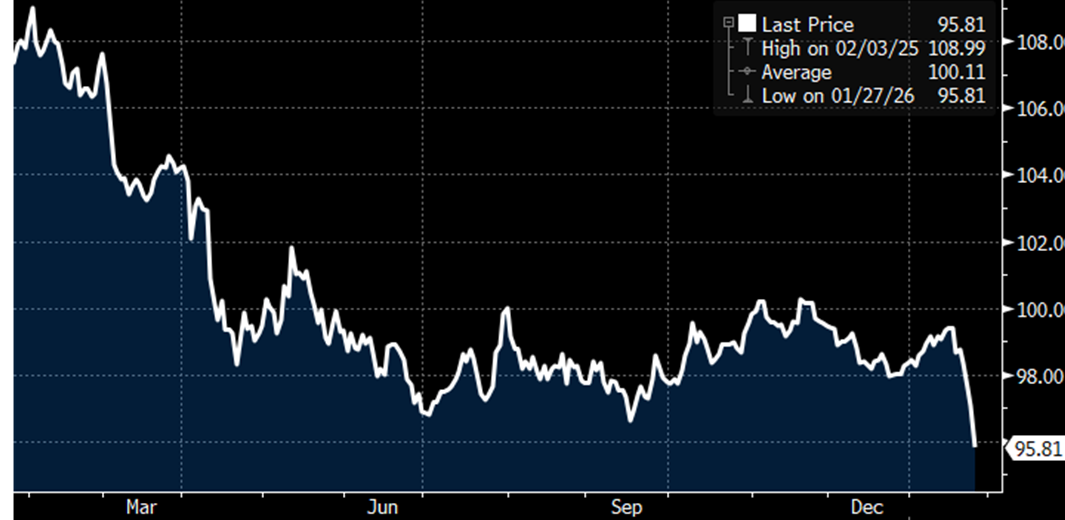

- Meanwhile, the US dollar is going through some things. It’s off more than 12% since its 2025 peak on February 3rd and in the early days of 2026 it’s down 2.2%. Part of the blame for the 2025 weakness was the ever-changing tariff and trade policies. A new wrinkle this year is the claim that the US may be aiding Japan in supporting its currency (selling dollars, buying yen) in a bid to keep Japanese bond yields from climbing further and limiting the potential for lower US yields. In any event, dollar depreciation makes imports more expensive which may play to the Trump administration’s overriding desire to reduce the trade deficit, but more immediately it may create an uptick in inflation until imported goods flow start to slow. It’s one of the things to put on the radar as we move through the year (see graphs below).

- The last of the meaningful releases this week will be Friday’s December PPI. While December CPI was released two weeks ago PPI carries importance as some of the metrics for the Fed’s preferred inflation measure, PCE, are pulled from this report. Expectations are for monthly increases in the 0.2% – 0.3% range with YoY figures dipping from 3.0% to 2.8% – 2.9%. Specifics like health insurance and airfares are two of the more notable items that flow into PCE.

- As shown below, the so-called super core measure (Core services ex-housing) of PCE has recently trended higher than CPI with much of that difference coming from PPI additions that measure some items as changes in margin which involves price paid as well as price asked. So, just because a margin may increase, it doesn’t necessarily mean a higher asking price, it could, instead, mean a lower price paid. In any event, for those hoping/expecting a March rate cut, you’ll want to see a softish PPI print that will eventually lead to a softer PCE print (see graph below).

January Conference Board Labor Differential (Jobs Plentiful – Jobs Hard to Get) Hits Five-Year Low Source: Conf. Board

Source: Conf. Board

US Dollar Continues to Weaken. The Latest Move May be in Defense of the Japanese Yen Source: Bloomberg

Source: Bloomberg

Sudden Rebound in Japanese Yen May Signal Currency Intervention Source: Bloomberg

Source: Bloomberg

Super Core PCE Has Recently Resisted Moving Lower Unlike Super Core CPI Source: Bloomberg

Source: Bloomberg

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.