Fed Expected to Pause at Wednesday’s Meeting

- This week will be dominated by the first FOMC meeting of 2026 with a rate decision on Wednesday afternoon (2pm ET). While a rate cutting pause is widely expected, Powell’s post-meeting press conference will certainly get attention and no doubt questions around his successor, and his unusually direct video response to the subpoena matter. We expect, however, Powell will revert to his usual stoic demeaner on Wednesday. The week also offers a smattering of interesting releases, namely January Consumer Confidence (Tues.) and December PPI (Fri.) to fill in time around the FOMC discussions. Currently, the 10yr is yielding 4.21%, down 3bps, while the 2yr is yielding 3.59%, down 1bp on the day.

- The other big event this week is a possible naming of Powell’s successor. The current Polymarket favorites are Kevin Warsh and Rick Reider. Both are considered independent enough to not endanger the Fed’s appearance of independence and thus viewed as capable of forging committee consensus where a Trump loyalist pick may encounter more pushback and possible dysfunction. Reider has been vocal about lowering longer term rates as a means to improve the housing market and his nomination would probably boost prices on longer duration debt.

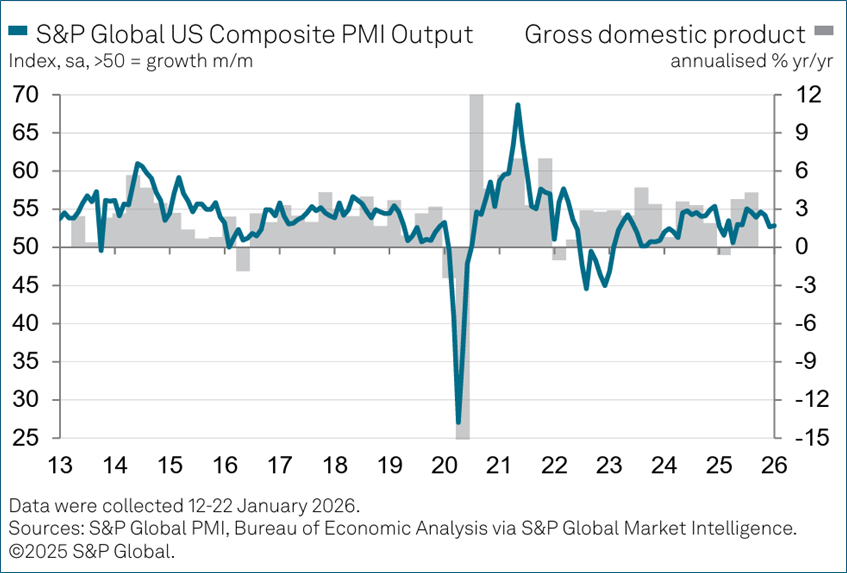

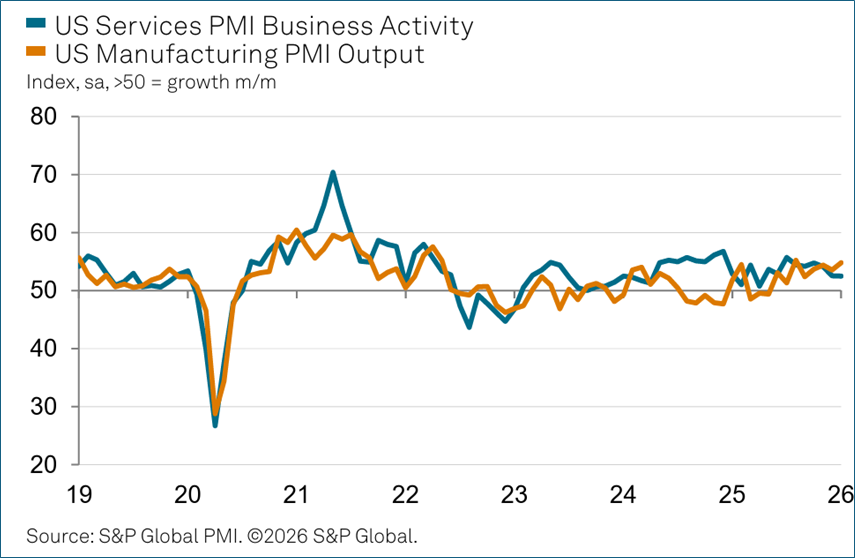

- Last Friday, S&P Global and its “flash” preliminary January PMI numbers reported business growth ticked higher but remained subdued compared to the typical rate of expansion seen in the second half of 2025. Manufacturing growth accelerated to outpace that of services, but the January survey brought further signs that underlying order growth has softened in both sectors recently, led by falling exports. Job numbers consequently remained little changed in January.

- Chris Williamson, Chief Business Economist at S&P Global Market Intelligence commented that “Confidence in the year ahead outlook remained positive but dipped slightly lower, as hopes for sustained economic growth and favorable demand conditions were somewhat offset by ongoing worries over the political environment and higher prices. Elevated rates of input cost and selling price inflation were again commonly attributed to tariffs, especially in the manufacturing sector, where price pressures intensified in January. However, service sector inflation moderated, linked in part to intensifying competition.”

- Williamson continued, “The survey is signaling annualized GDP growth of 1.5% for both December and January, and a worryingly subdued rate of new business growth across both manufacturing and services adds further to signs that first quarter growth could disappoint. Jobs growth is meanwhile already disappointing, with near stagnant payroll numbers reported again in January, as businesses worry about taking on more staff in an environment of uncertainty, weak demand, and high costs. Increased costs, widely blamed on tariffs, are again cited as a key driver of higher prices for both goods and services in January, meaning inflation and affordability remains a widespread concern among businesses.”

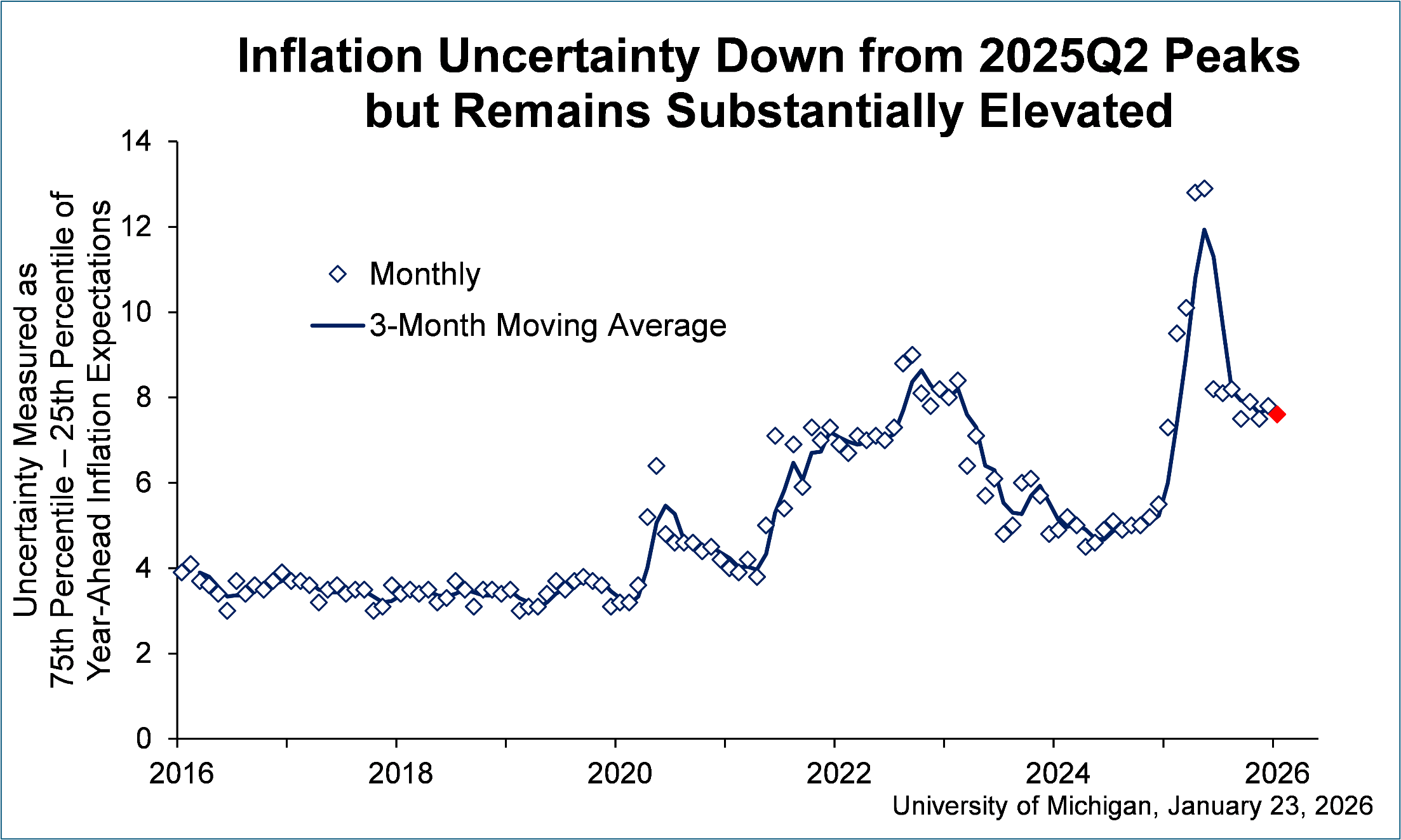

- Also released on Friday, the final look at January consumer sentiment via the University of Michigan Sentiment Survey. Consumer sentiment lifted this month to 56.4 vs. 54.0, with minor gains seen across all index components. While the overall improvement was small, it was broad based across income distribution, educational attainment, older and younger consumers, and Republicans and Democrats alike. However, national sentiment remains more than 20% below a year ago, as consumers continue to report pressures on their purchasing power stemming from high prices and the prospect of weakening labor markets.

- Year-ahead inflation expectations fell back to 4.0% this month from 4.2% in December. This is the lowest reading since January 2025 but remains well above that month’s 3.3%. Long-run inflation expectations inched up from 3.2% last month to 3.3% this month. In comparison, readings ranged between 2.8% and 3.2% in 2024 and were below 2.8% throughout 2019 and 2020.

S&P Global January “Flash” PMIs Soften Slightly

S&P Global Flash Manufacturing Output PMI Edges Higher While Services Unchanged

University of Michigan January Sentiment Survey – Year Ahead Inflation Uncertainty Elevated

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.