Fed Speakers Building Case for Shift from Easing to Neutral Bias

- Oil and commodity prices fell yesterday, while yields fell also, but little new was learned in the Middle East peace/ceasefire process. Such is life in the financial markets in 2026. The Conference Board’s survey of consumer sentiment yesterday wasn’t good, but it wasn’t as lousy as the University of Michigan numbers so there is that. Also, plenty of Fed speak will greet investors today and tomorrow which will help inform markets, as well as new Fed Chair Warsh. So far, the speakers have almost uniformly been on the hawkish side, so if Warsh is looking to begin setting the table for rate cuts, he’ll have plenty of setting to do. Currently, the 10yr is yielding 4.48%, down 1bp, while the 2yr is yielding 4.05%, also down 1bp on the day.

- With new Fed Chair Kevin Warsh now in place, the Fed speak will be interesting from this point forward as other FOMC members start to make their thoughts known before the June FOMC meeting. Fed Governor Chris Waller wasted no time speaking last Friday in Frankfurt, Germany noting he supports the idea of eliminating the easing bias saying the Fed should hold rates steady until elevated energy prices begin to fall, and that the Fed should stand ready to raise rates as much as it is to lower them. He said, “you just can’t look at this data and say, ‘Oh, yeah, we could cut rates here by September’ or something. You can’t be serious as a central banker and talk about that.”

- Waller wasn’t one of three who dissented at the last meeting. They were Logan, Hammack, and Kashkari, and they dissented because they wanted the easing bias shifted to neutral. The minutes, however, said “many” members wanted the change, which in Fed parlance implies 8-9; thus, several more than the three who formally dissented. Today, Fed speakers include Dallas Fed President Lorie Logan, Governors Jefferson and Cook and Chicago Fed President Austin Goolsbee. We’ll have three more speakers tomorrow and six on Friday. So, Warsh will have a pretty good idea where the committee stands when he gavels in the June FOMC meeting.

- The weekly ADP Pulse Report noted that 35,750 new private sector jobs were created during the week ending May 9th. The figure is a four-week average, so it covers the last two weeks of April plus the first half of May. The previous week’s average of 42,750 was the highest in the brief history of the report which started July 25, 2025 (see graph below). While the correlation between ADP and the BLS Nonfarm Payrolls Report has been tenuous at times, the ADP private sector strength implies the BLS Report due on June 5th will be decent to solid giving the Fed time to wait on better inflation numbers.

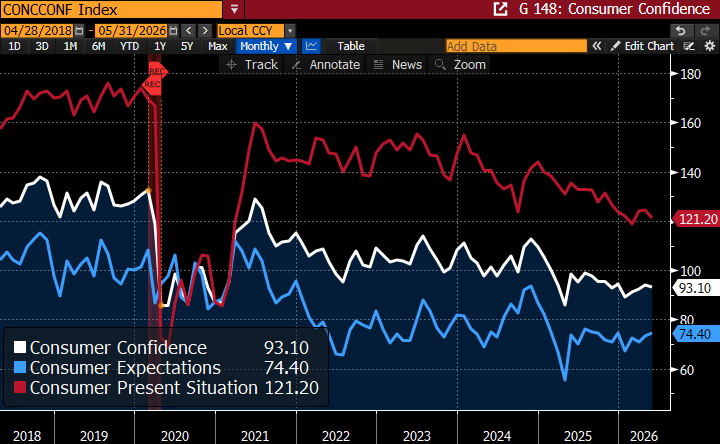

- Last Friday’s University of Michigan Final Sentiment Survey for May surprised to the downside with a new all-time low in sentiment with upside surprises to both the 1yr and 5-10yr inflation expectations. Yesterday’s Conference Board Consumer Confidence was lower as well but not to the degree found in the Michigan survey.

- The Conference Board’s confidence gauge decreased from 93.8 to 93.1, but that beat the 92.0 expectation. The Present Conditions index fell 3.2 points to a three-month low of 121.2 vs. 123.0 expected, while the Expectations measure rose from 72.2 to 74.4 and beating the 71.9 forecast. The report adds to evidence of growing anxiety among American consumers about the high cost of living. Two-thirds of consumers reported cutting back on spending due to rising prices. When asked how their spending habits had changed, many respondents reported buying fewer items, delaying expensive purchases, and buying cheaper versions of the same item.

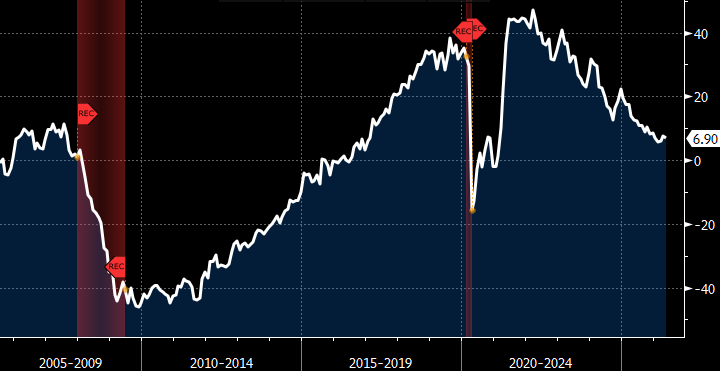

- Dana Peterson, chief economist at the Conference Board noted that, “consumer confidence edged downward in May as the inflationary impacts of the war in the Middle East intensified.” At the same time, despite the declining sentiment readings, consumer spending has been solid, partly aided by tax refunds, which should be playing itself out in the next month or two. The survey showed consumers expect more jobs to be available in the next six months with expectations gauge rising to the highest level this year. The share of consumers who said jobs were plentiful decreased to the lowest since 2021, but the share saying jobs were hard to get also moved lower. The difference between these two — the so-called Labor Differential — edged down from 7.50 to 6.90 but that remains above the recent low of 5.70 in February (see graph below).

ADP Weekly Pulse Report – Today’s Update was 35,750 for the Week Ending May 9th Source: ADP

Source: ADP

Conference Board – Consumer Confidence Dips but Expectations Improve

Conference Board – Labor Differential (Jobs Plentiful Minus Jobs Hard to Get) Dips in May but Above Feb. Low Source: Conf. Board

Source: Conf. Board

Conference Board – Jobs Plentiful Drops to Five-Year Low Source: Conf. Board

Source: Conf. Board

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.