Fed Still Sees One Cut in 2026

Meeting Highlights

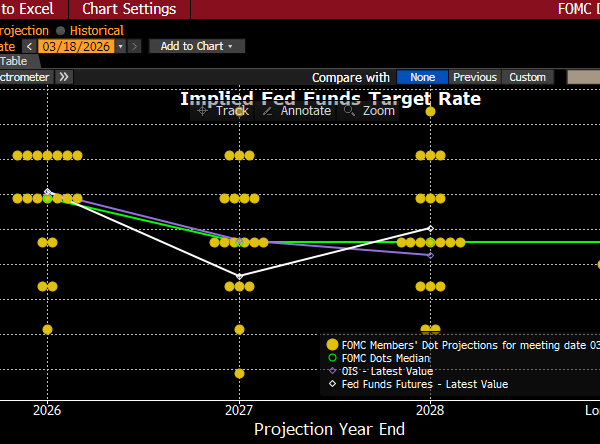

- As widely anticipated, the Fed left the funds rate unchanged at its target rate range of 3.50% – 3.75%. The biggest uncertainty heading into the meeting was the updated rate forecast, or dot plot, along with changes to the Summary of Economic Projections (SEP). In December, they had the funds rate dropping to 3.25% – 3.50% at year-end 2026, that implied a single 25bps cut in 2026. The median rate in today’s dot plot also expects a single 25bps rate cut in 2026 to finish the year at 3.25% – 3.50%. That would put the rate just above the so-called neutral rate, or the rate that is neither restrictive nor accommodative. That rate was bumped up from the December dot plot to 3.125% from 3.00%.

- The notable change to the statement regards the war developments. In the January statement the Committee was, “attentive to the risks to both sides of its dual mandate.” In today’s statement that take remained in place with the caveat preceding it that “The implications of developments in the Middle East for the U.S. economy are uncertain.”

- The FOMC will have a new Fed Chair in May, with Kevin Warsh the President’s nominee and the expectation is that he’ll be more inclined for rate cuts than Powell, but he’s just one of twelve voters; thus, the futures market continues to see, at best, one 25bps cut this year. As for today’s meeting there was just one dissent, Fed Governor Stephen Miran, who kept his streak alive dissenting at every meeting he has attended. However, the updated dot plot continues a trend of dispersion among participants, with 7 participants expecting no rate change this year, but x participants expecting a single rate cut this year and 5 participants comprising the dovish contingent that see two (2 participants), three (2), or four (1) cuts by year-end. That dispersion continues into subsequent years with the neutral, or Longer Term, rate median lifted from 3.00% to 3.125%. The dispersion of the neutral rate runs from 2.60% to 3.90%. Thus, there is a wide range of views on the Committee so good luck to future chair Warsh in herding those cats towards a rate cut in future meetings.

- Fed Funds futures pricing prior to the announcement had one cut priced in for 2026, but it wasn’t a firmly held outlook. After the updated dot plot projections, the futures market increased the odds modestly for a single rate cut for this year (41%), with 19% odds now for a second cut. Thus, the futures market expects the Fed to cut this year, but the betting remains more with a single cut rather than two or more.

- Given this is a quarter-end meeting, the FOMC updated its economic forecast with a fresh Summary of Economic Projections (SEP). We should caution, however, that with the effects of the Iran war still very uncertain this update should be viewed with a wide error band. That said, the Fed now sees 2026 GDP growth at 2.4% versus 2.3% in the December forecast. Growth is expected to slow to 2.3% in 2027 and 2.1% in 2028, both a tenth above the December forecast.

- On inflation, the Fed increased the expected median core PCE for year-end 2026 to 2.7% vs. 2.5% in the December forecast. We are currently at 3.1% as of January. The 2027 forecast was bumped a tenth higher at 2.2% then 2.0% in 2028, same as the December forecast.

- As for the labor market, the forecast is for the unemployment rate to remain at 4.4%, same as the December forecast and matching the current rate. For 2027, the rate is expected to be 4.3% then 4.2% in 2028, again matching the December forecast.

- Today’s SEP update seems rather optimistic that the impact of the Iran war will be limited with little change in economic measures from the December forecast. That will obviously be tested in the coming weeks and perhaps months. A period of “watchful waiting” seems to be the prudent course for now. We certainly don’t envy chair nominee Warsh as he attempts to convince Committee voters to look through the potential war impact and sign on for rate cuts if the hostilities are ongoing. After the supply shock following the pandemic reopening, and the spike in inflation that followed, an energy-induced supply shock that still has an indefinite duration will light the inflation warning light with many on the FOMC. That is, they will be very reluctant to cut until most of the uncertainty around the depth and length of the latest supply shock is removed.

Dot Plot from March FOMC Meeting

Source: FOMC

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.