FOMC Day – We Expect a Hawkish Message Today

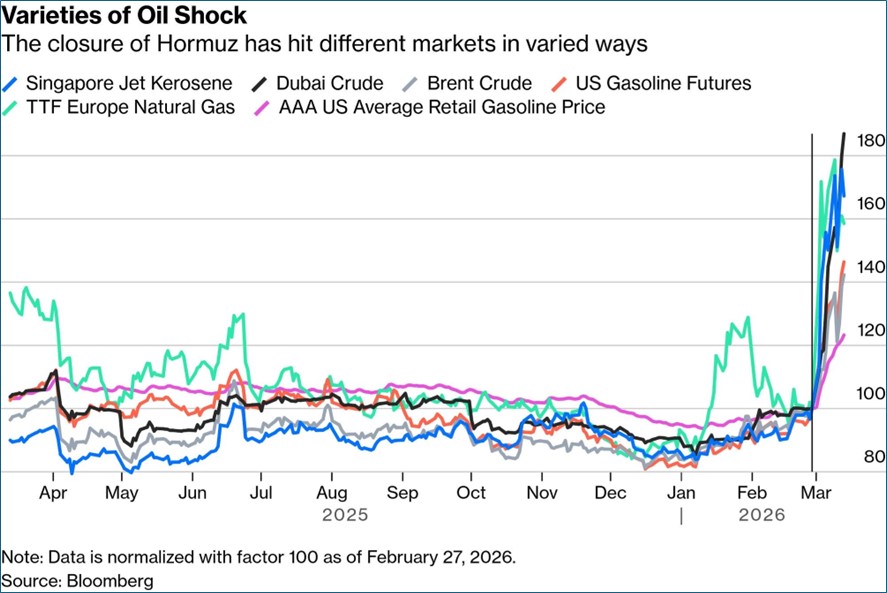

- It’s Wednesday, so that means FOMC Decision Day. While everyone, including us, expect the Fed to pause there’s still plenty to learn from today’s meeting that we delve into below. Also, another piece of the inflation puzzle was revealed today as the February PPI report was released and that means more pieces to fit into the PCE inflation puzzle. Meanwhile, the topic looming above all others, the Iran war, remains in play with little movement still around the Strait of Hormuz, except apparently, ships that are getting the OK from Iran to transit the Strait. These few vessels appear to be India and/or China bound with Iranian oil. Currently, the 10yr is yielding 4.21%, up 1bp on the day, while the 2yr is yielding 3.71%up 4bps on the day.

- The FOMC will render its rate decision this afternoon at 2pm ET. While no rate cut is the widely held expectation, one key unknown is whether the updated Dot Plot will continue to see a single rate cut this year, same as the December forecast. If the expected hawkish tone is the theme, we see the single cut expectation from December rescinded with a view towards no rate cuts in 2026.

- The Fed will also update its economic forecast, or what it calls the Summary of Economic Projections (SEP). In that regard, we expect 2026 year-end core PCE inflation (2.5% in Dec. forecast) and the unemployment rate (4.4% in Dec.) to be revised higher, with GDP (2.3% in Dec.) to be revised lower. How close we come to a stagflation-type forecast is another question investors will be looking to have answered, not that the market is enthralled with the Fed’s forecasting abilities, rather, it may provide a clue into the Fed’s current reaction function. That is, do they accept higher inflation in order to keep employment and growth up, which implies a bias to cut, or do they see inflation moderating but at the expense of growth and jobs, implying a stable rates policy.

- Powell will also provide a post-meeting press conference and is sure to be asked about the Fed’s thinking on the potential impact of the Iran war. In true Powellian fashion, we expect the Chair to defer an unequivocal answer until more is known, primarily the timeframe of the conflict, and particularly the status of the shipping choke point that is the Strait of Hormuz. Much like the pandemic, the war is creating supply shortages, this time oil and a myriad of other second-order petro-derived products. The longer this effective shipping embargo lasts, the greater the spread of the supply shock. Thus, Powell recalls the inflation surge from the pandemic supply shock and will probably signal an alertness for any repeat of that scenario. Thus, we anticipate, on whole, a rather hawkish meeting and commentary today.

- While we’ll get messaging dominated by Powell today, we’re also mindful that his time as Chair is ending soon. There is another meeting in April and then his final meeting as Chair in May. Then, it becomes in all likelihood Kevin Warsh’s FOMC, and we know where he probably sides in that inflation/demand debate. The retort to that is he is but one vote in twelve, so good luck bringing over enough inflation hawks to the rate-cutting caucus to reach the seven rate-cutting votes. We’ll be back this afternoon with a recap of the meeting and what we did or didn’t learn.

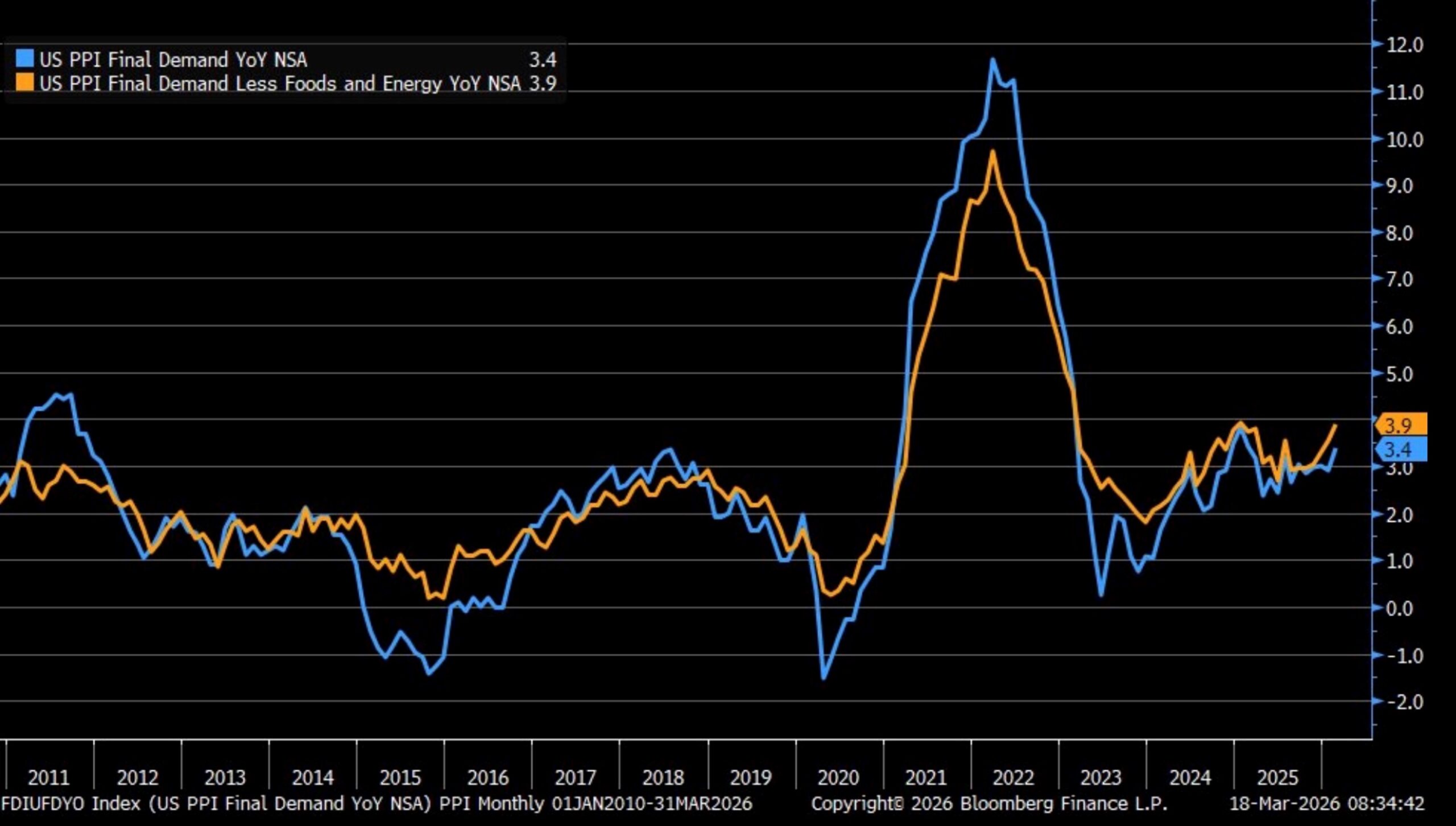

- Speaking of inflation, we received a hot February PPI Report this morning with the overall reading up 0.7% vs. 0.3% expected and 0.5% in January. PPI ex-food, energy, and trade was up 0.5% vs. 0.3% expected and 0.8% the prior month. Overall PPI is now up 3.4% YoY vs. 2.9% in January. PPI ex-food, energy, and trade was up 3.5% vs. 3.4% the prior month. The monthly PPI report has become more than just a read on wholesale pricing movements and more a tell on upcoming PCE inflation numbers as a handful of increasingly sensitive pieces within PPI are also used in the PCE series. With the widening gap between CPI and PCE inflation, any sign that the PCE-related pieces come in hot implies more heat when the PCE series is released later this month.

- In that regard, foreign airline fares rose 0.9%, investment management fees rose 1.0%, and healthcare was up 0.6%. Given that with February CPI already published analysts were leaning towards a hottish 0.4% MoM print for PCE, so these additional pieces may add to that temperature even more. And keep in mind, this all comes before the increasing energy costs and secondary effects from the Iran war. It would seem a potent arsenal for the inflation hawks on the FOMC to argue for a lengthy pause in policy.

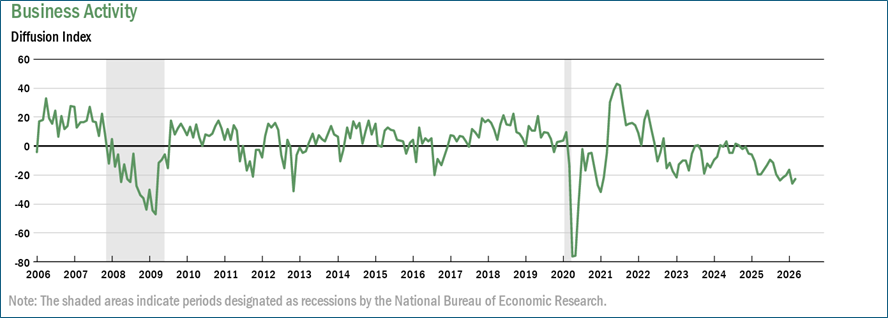

- We mentioned on Monday that the March preliminary University of Michigan Sentiment Survey covered both the week before and the week the Iran war began. The difference in responses from one week to the next was noticeable. Well, we have another survey where the survey period is from early March, so coming fully after the war began and the sentiments are even more downbeat. We speak of the New York Fed’s Business Leaders Survey. The latest survey found business activity continued to decline significantly in the region’s service sector. The survey’s headline business activity index was little changed at -22.6. 19% of respondents reported that conditions improved over the month while 42% said that conditions worsened. The business climate index fell five points to -46.2, with 56% of respondents reporting an unfavorable business climate, suggesting the business climate remained much worse than normal. Employment fell for a seventh consecutive month. Supply availability worsened. The pace of both input price increases and selling price increases was little changed but remained elevated. Looking ahead, firms were less optimistic about the outlook.

February PPI – Hotter Than Expected and Before War Effects

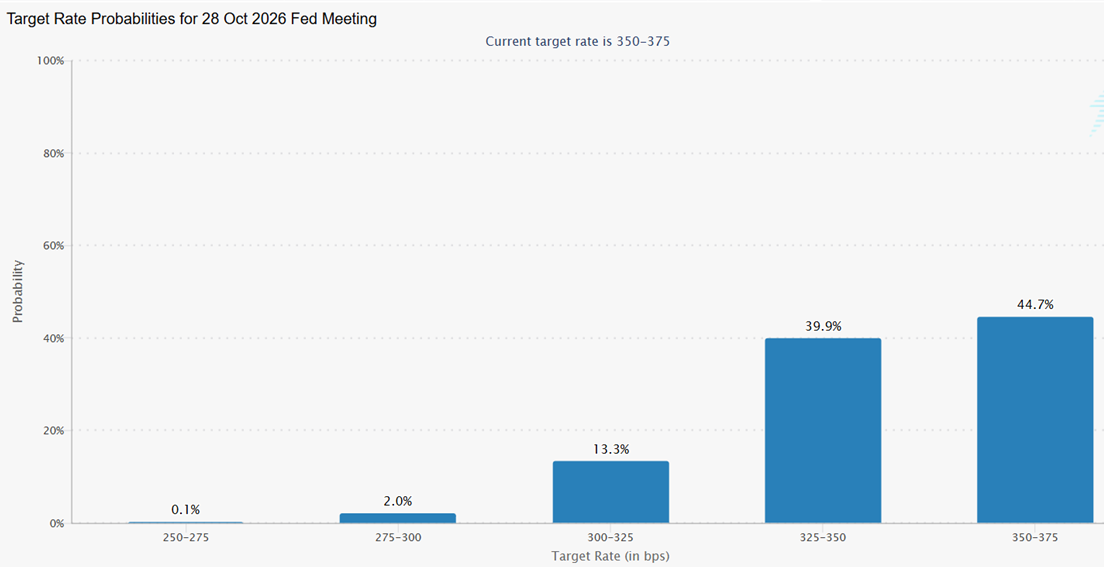

Futures Getting the Hawkish Message – Odds Now See October Meeting as Next Possible Rate Cut Source: CME Group

Source: CME Group

NY Fed Business Sentiment – Not Great as War Concerns Increase Source: NY Fed

Source: NY Fed

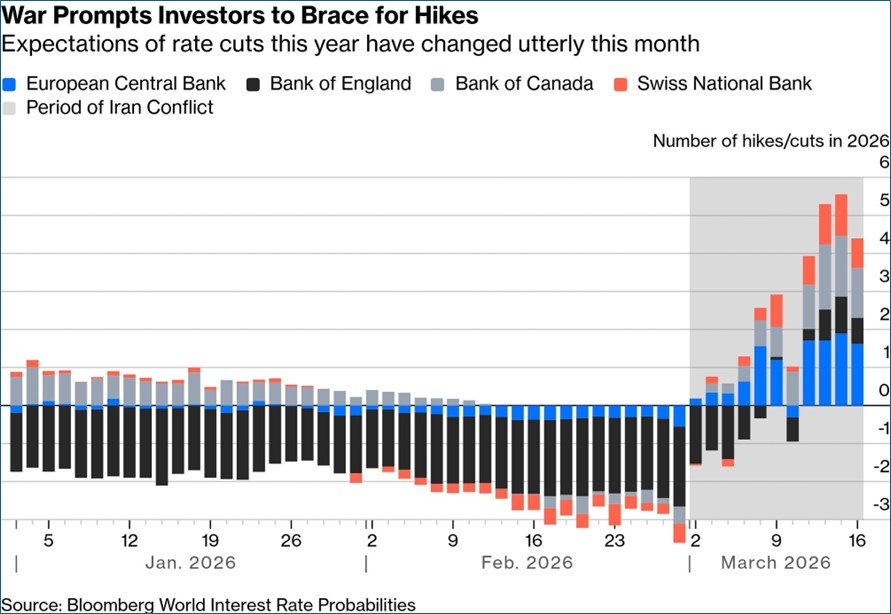

Other Central Banks May Shift to Hikes to Offset Increasing Inflation Risk

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.