FOMC Meeting and Powell’s Future

- This week will be highlighted by the FOMC rate decision on Wednesday, despite the almost universal expectation that they will hold rates steady. The other big event should be the advancement of Kevin Warsh’s nomination as Fed Chair now that the DOJ has dropped litigation regarding the Fed’s construction project, and Senator Thom Tillis (R-NC) has agreed to let the vote proceed. Whether that leads to current Fed Chair Powell stepping down in May, only he can answer that which he will no doubt be asked at the FOMC press conference. Add in a dose of inflation news with the March PCE numbers on Thursday and the ever-present Iran war uncertainty and it looks to be a week sprinkled with moments of routine and possible drama. Currently, the 10yr is yielding 4.31% unchanged on the day, while the 2yr is yielding 3.79% up 2bps on the day.

- While the FOMC is expected to hold rates steady on Wednesday, the DOJ’s decision last Friday to drop litigation on the Fed’s construction project will certainly prompt questions regarding Chair Powell’s future. Assuming Kevin Warsh is confirmed by the Senate as the new Fed Chair, will Powell elect to stay on as a governor until that term expires in 2028, or will he elect to depart as has been the customary move?

- Powell will no doubt be asked the question on his future but whether he delivers a definitive answer is still up for debate. Just because the DOJ has announced it is dropping the litigation, there is nothing to say the DOJ can’t resurrect the litigation, and that may keep Powell hesitant to depart. Not to mention, if he does leave it gives President Trump another spot to fill with what will undoubtedly be another cut-minded candidate. Fed intrigue seems destined to increase in the weeks and months ahead.

- Away from the Fed news, the major economic release will be Thursday’s March Personal Income and Spending Report. The PCE inflation component will be the most watched from the report but the personal spending numbers, especially the inflation-adjusted numbers, will be plenty of attention too.

- Personal income is expected to increase 0.4% vs. a disappointing -0.1% in February. Personal spending is expected to increase a robust 0.8% vs. 0.5% the prior month with real personal spending (net of inflation) expected to increase 0.1% vs. 0.1% in February. The solid Retail Sales Report last week is providing belief that the more comprehensive and services-heavy personal spending numbers will be at least as solid as the retail sales number, if not more, as consumers appear to have continued spending on travel and entertainment during spring break month.

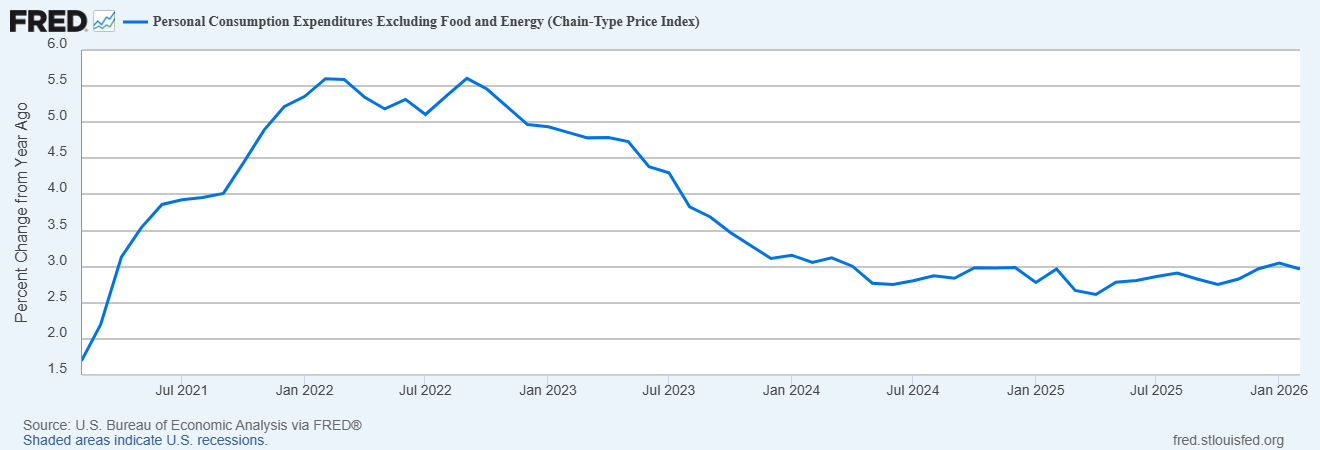

- The PCE inflation series is expected to post a large increase, spiked by higher energy costs, with headline PCE expected to increase 0.7% vs. 0.4% in February with the YoY rate climbing from 2.8% to 3.5%. Ex-food and energy, core PCE is expected to increase a more moderate 0.3% vs. 0.4% in February with the YoY rate ticking up from 3.0% to 3.2%. These numbers will obviously keep the inflation hawks on the Fed firmly in pause mode, and the realization that higher energy costs and supply shortages will likely spread into more of the core areas in subsequent months is a big reason that futures markets see little chance of a rate cut before year-end. Adding to the inflation challenge, for the next couple quarters the monthly numbers dropping from last year will be in the 0.1% – 0.2% range, so expect no improvement in the YoY rates for quite some time.

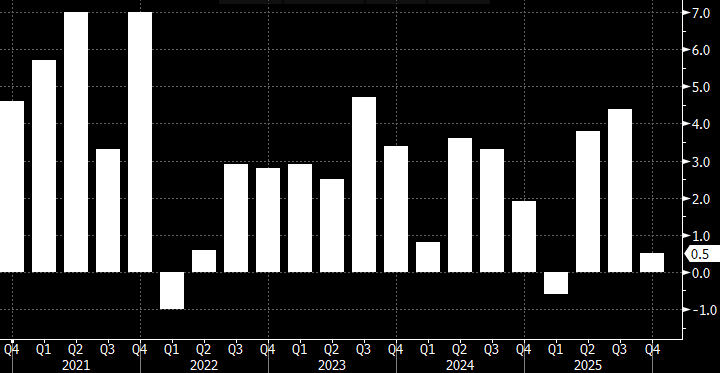

- Also on Thursday, we’ll get the first estimate of 1st quarter GDP with expectations at 1.6% annualized vs. 0.5% in the 4th Personal consumption is expected to be similar to the 1.9% pace set in the 4th quarter. The price indices will get less attention just because the spike in March will be softened some by the inclusion of more benign January and February numbers and the belief that higher energy costs from March will spread into other areas in April. That’s a long-winded way of saying don’t spend too much time combing over the GDP inflation numbers as they’ll be considered somewhat stale.

- Finally, the April ISM Manufacturing Index will be released on Friday with expectations that it held steady at 52.7. Last week’s better-than-expected S&P Global PMI numbers were talked down some as it was surmised that much of the increased activity was simply preemptive in nature; that is, restocking ahead of expected price increases and/or shortages due to the shipping blockade out of the Strait of Hormuz. We’ll see if ISM comes to the same conclusion.

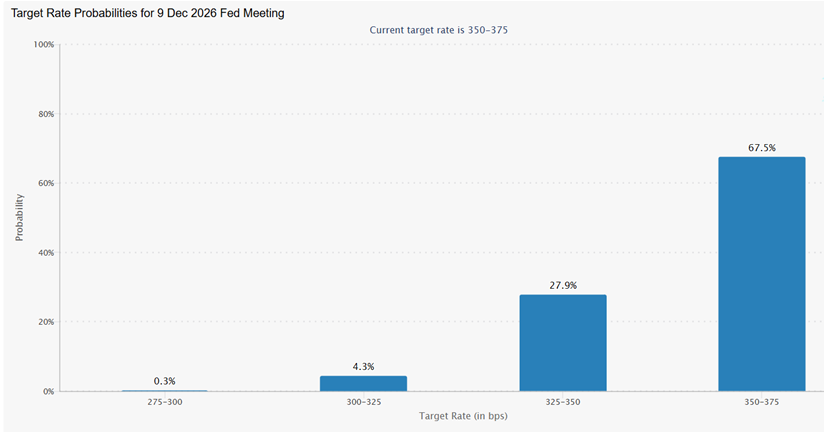

Futures See 68% Odds of No Rate Change This Year

Source: CME Group

First Quarter GDP (Annualized) Expected at 1.6% vs. 0.5% 4Q25  Source: US BEA

Source: US BEA

March Core PCE Inflation (YoY) – Expected to Increase from 3.0% to 3.2%

Source: Dept. of Labor

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.