FOMC Rate Decision Today and Powell Presser

- This afternoon the FOMC will render an unchanged rate decision, surprising no one, but the real drama will be the post-meeting press conference. With the way now clear for Kevin Warsh’s nomination to succeed him as Fed Chair will Powell declare his time at the Fed done, or will he stay on through the end of his governor’s term, which extends through January 2028? We’re not likely to get that much clarity today but expect the question to be asked. In addition to the Fed’s rate decision today, several other central banks meet this week which will add to the policy drama. Add in a sprinkling of first-tier economic reports and the menu is a solid one for market watchers.

- While the FOMC is expected to hold rates steady, with Kevin Warsh now expected to clear his nomination vote this week, will Chair Powell discuss his future in today’s press conference? While Powell’s term as chairman ends on May 15, his term as governor extends into 2028. While it’s been customary for a Fed chair to leave the FOMC when their chairmanship ends, it’s not unprecedented for one to stay on, and with no love loss between Trump and Powell, not to mention the risk that the litigation can be restarted, Powell may decide to hang around as a governor until that term expires in 2028.

- What we learn later today about Powell’s future will be the primary drama coming from today’s meeting. I suspect he feels hesitant to leave the scene when the risk of litigation remains front and center. It could be a case of better to control what you can from inside rather than looking in from the outside. I don’t expect we’ll get that kind of clarity today, but I also don’t expect a retirement announcement either.

- It’s not all about the Fed this week. The ECB, Bank of England, Bank of Canada, and Bank of Japan also hold, or have held, central bank meetings this week with all expected to keep their respective policy rates unchanged. The bigger question is how much will the risk of higher inflation stemming from the Middle East situation play into future policy moves, and how much will the commentary represent a sort of preparing investors for coming rate hikes? We suspect there will be just that prep work in this week’s meetings as the other central banks have a single inflation mandate unlike the Fed’s dual mandate. We should add the Bank of Japan has already had its meeting and it was defined as a “hawkish hold.” Rates were left unchanged, but the commentary was definitely leaning towards a hike in the near future. That may well be the message we hear from the others as well.

- In non-central bank news, yesterday the Conference Board released its latest reading on consumer confidence for April. Overall confidence edged up from 92.2 to 92.8 vs. 89.0 expected. The Present Situation Index fell from 124.1 in March to 123.8, while the Expectations Index increased from 71.0 the prior month to 72.2 in April. Consumers were also less negative about the labor market in April. 16.1% of consumers expected more jobs to be available, up from 15.4% in March, while 26.9% anticipated fewer jobs, down from 27.8%. So, a slightly better view of job prospects and in sentiment, generally speaking, although the gains were marginal at best.

- March Trade Balance numbers are due this morning along with preliminary Durable Goods Orders. The trade balance deficit is expected to widen from -$83.5 billion to -$87.9 billion as exports are expected to slow more than imports as international shipments face pricing and transportation snags from the Iran war. It’s expected to also be a mixed picture on durable goods with orders up 0.5% vs. -1.3% the prior month but ex-transportation it’s a bit less robust with a 0.4% increase expected vs. 0.9% in February.

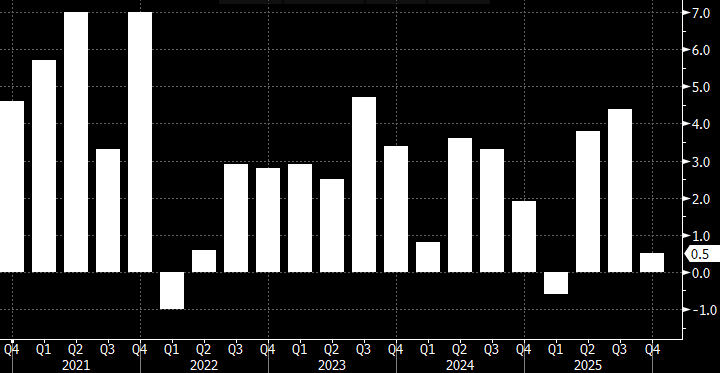

- Tomorrow brings the first estimate of 1st quarter GDP with expectations at 1.6% annualized vs. 0.5% in the 4th Personal consumption is expected to be similar to the 1.9% pace set in the 4th quarter. The March Personal Income and Spending Report will also be a key piece of information and while the numbers are part of the 1st quarter GDP report, the Fed’s preferred inflation series (PCE) is expected to reflect the beginnings of price pressure from the blocked and or slowed oil and cargo shipments in and around the Strait of Hormuz.

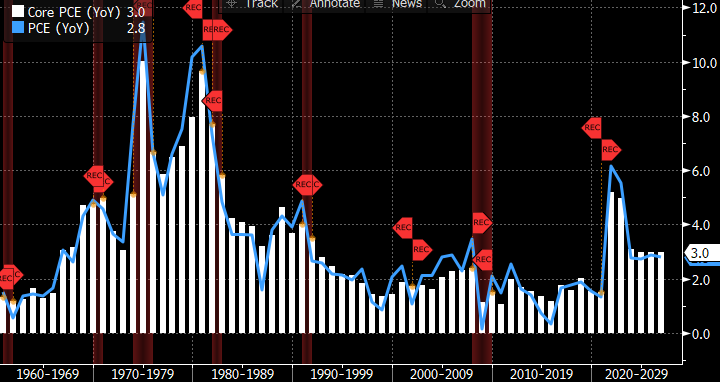

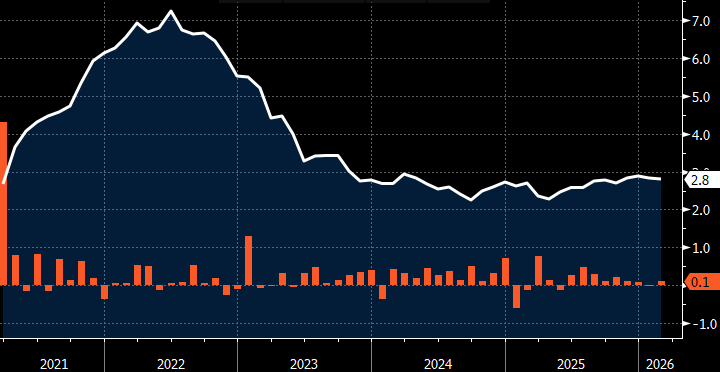

- It’s expected that inflation gains a robust 0.7% during March with the YoY rate rising from 2.8% to 3.5%. The core rate (ex-food and energy) is expected up a more manageable 0.3% vs. 0.4% in February with the YoY rate increasing from 3.0% to 3.2%. With low 0.1% and 0.2% monthly prints from last year rolling off the calculation over the next several months expect those YoY rates to continue inching higher into the summer. That will keep the Fed firmly in pause mode as long as the labor market isn’t falling apart.

PCE Inflation Expected to Move Higher in March Source: US BEA

Source: US BEA

Real Personal Spending Has Held Up to this Point – Will it Continue in March? Source: US BEA

Source: US BEA

First Quarter GDP (Annualized) Expected at 1.6% vs. 0.5% 4Q25 Source: US BEA

Source: US BEA

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.