Fourth Quarter GDP Misses While Inflation Stays Sticky

- With geo-political issues swirling we end the holiday-shortened week with a pair of headline grabbing reports: Fourth Quarter GDP and Personal Income and Spending. We discuss the results of both of those reports below and look ahead to next week where the Conference Board’s February look at consumer confidence headlines a second-tier list of releases. Currently, the 10yr is yielding 4.08%, unchanged on the day, while the 2yr is yielding 3.47% also unchanged on the day.

- This morning, we received the first estimate of fourth quarter GDP and it disappointed at 1.4% vs 2.8% expected and 4.4% in the third quarter. The Atlanta Fed’s GDPNow forecast had its final estimate at 3.0% (2.99%, unrounded). Personal consumption increased 2.4% matching expectations but off the 3.5% in the prior quarter. On the inflation front, overall PCE increased 3.0% vs. 2.8% expected and 3.8% the prior quarter. Core PCE prices rose 2.7% vs. 2.6% expected and 2.9% in the third quarter. Real Final Sales to Domestic Purchasers (consumer spending and business fixed investment) was 2.4% vs. 2.9% in the 3rd quarter (see graph below).

- Thus, GDP cooled quite a bit from the third quarter with the government shutdown and slower exports contributing to that miss but consumer spending, at 2.4%, was still solid and that is reflected in the Real Final Sales to Private Domestic Purchasers (see graph below). The hotter inflation read could be problematic but some easier YoY comparisons await in January and February, so some first quarter improvement is likely. One question is whether consumer spending continued slowing into the new year, and more specifically how did spending hold up in December? The answer to that question, and the inflation trend, are answered in the other report received today, Personal Income and Spending for December.

- While the Personal Income and Spending data for December are a part of today’s GDP release, it does give us a better sense of momentum heading into 2026. Personal income increased 0.3% as expected and 0.4% in November. Personal spending increased 0.4% vs. 0.3% expected and 0.4% the prior month. Real spending – adjusted for inflation – increased 0.1% as expected and 0.3% in November.

- On the inflation front, overall PCE increased 0.4% vs. 0.3% expected and 0.2% the prior month. Core PCE (ex-food and energy) rose 0.4% (0.36% unrounded) vs. 0.3% expected and 0.2%. On a YoY basis, overall PCE advanced 2.9% vs. 2.8% expected and matching the November print. Core PCE YoY was 3.0% vs. 2.9% expected and 2.8% the prior month. It’s the highest YoY pace since Feb. 2025. Thus, inflation continued to be sticky as 2025 ended. The good news with the PCE series is that January and February 2025 at 0.31% and 0.45%, respectively, provides a possible roll down in the YoY rate during the first quarter of 2026 if the monthly updates print in the 0.2% area or less, we obviously missed that in December. Thus, a rate cut in the June time frame remains possible if early year inflation behaves.

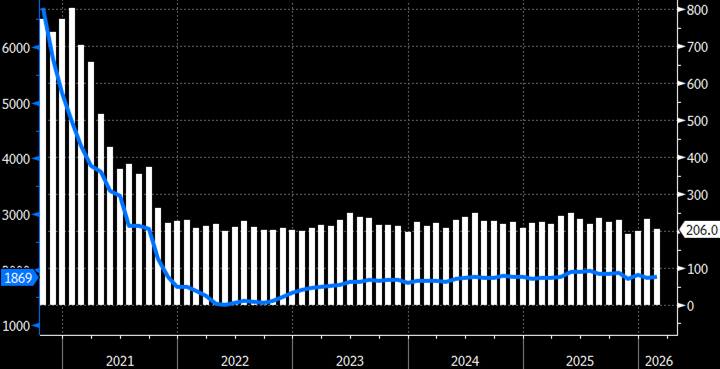

- Yesterday, we received the latest read on initial jobless claims, and this one carries a little more weight as it coincides with survey week for February Nonfarm payrolls. For the week ending February 14, initial jobless claims totaled 206,000 a decrease of 23,0000 from the previous week’s revised 229,000 (up from 227,000 originally reported). The 4-week moving average was 219,000, a decrease of 1,000 from the previous week’s revised average. That represents the sixth month out of the last seven where jobless claims during survey week surprised to the downside. That bodes well for another decent/solid jobs report for February. The release of that report is scheduled for March 6.

- Continuing claims for the week ending February 7 was 1,869,000, an increase of 17,000 from the previous week’s revised level. The previous week’s level was revised down by 10,000 to 1,852,000. The 4-week moving average was 1,845,250, an increase of 1,000 from the previous week. Thus, once again the low-hire, low-fire environment that we’ve been in for a year appears to be continuing.

- December’s Trade Deficit widened to -$70.3 billion vs. -$55.5 billion expected and -$53.0 billion prior. Imports improved +3.6% MoM vs. 0.1% expected and +4.2% in November. Exports fell at -1.7% MoM vs. +0.1% expected and -3.4% the prior month. The goods trade deficit widened to -$98.5 billion vs. -$86.0 billion expected and -$82.8 billion prior. For 2025, the deficit was $901.5 billion, down $2.1 billion vs. 2024. Exports were $3,432.3 billion, up $199.8 billion from 2024. Imports were $4,333.8 billion, up $197.8 billion from 2024. Thus, despite all the volatility over trade policies during the year and the application of tariffs on nearly all trading partners there was almost no change in the deficit position in 2025 vs. 2024.

Government Shutdown Contributed to 4th Quarter GDP Miss

Source: BEA

Final Sales to Private Domestic Purchasers (Consumer Spending and Private Fixed Investment) – Down from 2.9% in the 3rd Quarter but Still Solid Result

Source: BEA

Initial Jobless Claims and Continuing Claims – Signal Low-Hire, Low-Fire Continues

Source: Dept. of Labor

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.