Heavy Data Week Spars with War News

- We enter what is typically the busiest week of any month as far as first-tier economic data is concerned, headlined by the jobs report on Friday, but this week the economic data will spar with geo-political developments for investor attention. The weekend war news creates additional issues and uncertainties that the market must react to while assessing the latest readout on the economy and the labor market. The early action is fairly predictable with oil and gold prices up while equities are pointed lower and yields backing up a bit from the weekend price action. Currently, the 10yr is yielding 4.00%, up 4bps, while the 2yr is yielding 3.45%, up 7bps on the day.

- Markets are acting predictably in the face of the weekend events with oil prices up and equity futures lower in a classic risk-off move. Oil is currently trading around $72.80 per barrel, up nearly $6 while shipments through the Straits of Hormuz remain severely constricted. Most of Iran’s oil heads east towards India, China, and other Asian markets so the supply impact to the West and to the US is much less intense, although as a global commodity you see the price reaction, (See graph below). The Houthi’s have said they will start striking vessels again in the Red Sea near the Bab-al Mandeb Strait. That will force ships to avoid the Suez Canal and route cargo the long way around Africa. Thus, the early developments are higher oil prices and longer, slower delivery times.

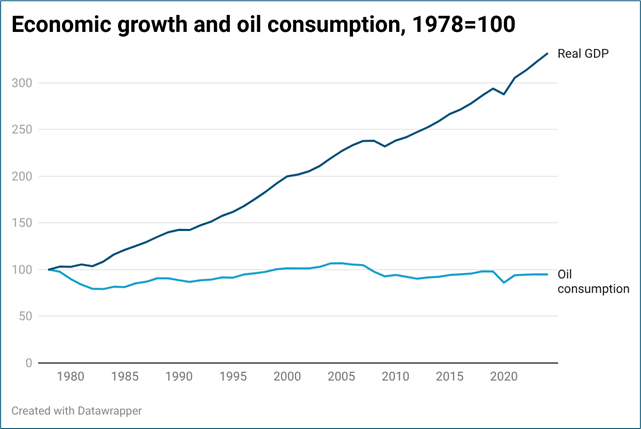

- Those that are old enough to recall the 1970’s oil lines probably are having some unpleasant flashbacks. The good news is that that is not likely to happen again. First, the US is mostly energy independent thanks to the shale revolution, so even with slowing global shipping of crude we should have plenty of supply. Also, while some price spikes are inevitable, our economy uses oil/energy much more efficiently than in the ‘70’s. Our GDP is 4X as large as in 1980, but we consume a similar amount of oil (see graph below). Also, in the 70’s core inflation was near 7%, so the price jump made a bad inflation situation intolerable. While we might see a bump in overall inflation, it’s likely to be less intense and coming from a much lower base level. That’s not to say we sail through this with little disruption but comparisons to a 70’s-like scenario are probably not accurate.

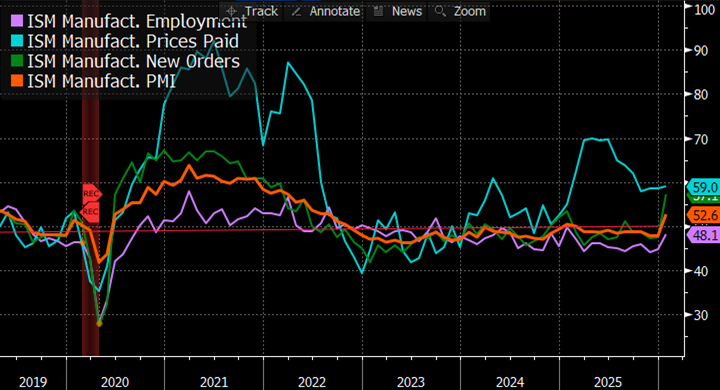

- Turning to the mundane matters of economics, as we mentioned above, the first week of the month provides a deluge of reporting on the prior month’s activity, and despite the outbreak of hostilities in the Middle East this week is no different. First on the list is the ISM Manufacturing Survey at 10am ET with the headline reading expected to tick slightly lower from 52.6 to 51.8. The 52.6 from January was a surprising beat and well clear of the 50 dividing line between an expanding versus contracting sector. It was the first time above the 50-level since a one-month pop in January last year. Can it maintain a plus 50 reading this year unlike in 2025? The other readings within the report, Prices Paid, New Orders, and Employment all moved higher in January and will get plenty of scrutiny along with the headline reading as well.

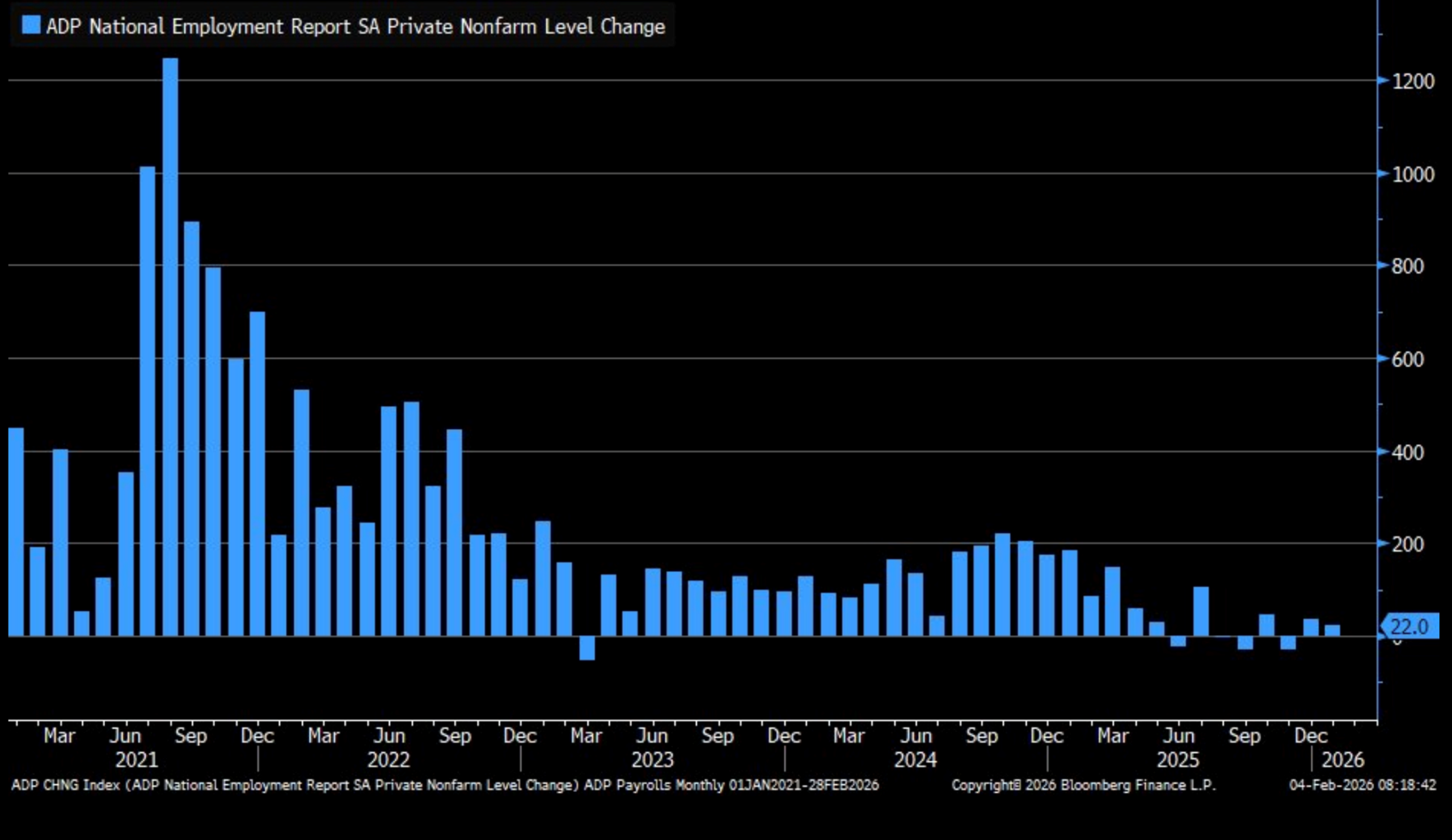

- Wednesday brings a pair of interesting labor market reads. First, ADP will publish its February Employment Change report with 43 thousand private sector jobs expected vs. 22 thousand in January. Later that morning, the ISM Services Index will be released with a slight uptick expected from 53.8 to 53.9. That would keep it solidly in expansion territory but with little change from January. Just as in the ISM Manufacturing Survey the other measures like Prices Paid, New Orders and Employment will get attention, but expectations are that both the manufacturing and services sides of the economy posted solid performance in February and that bodes well for economic performance.

- The February employment report will be released on Friday with expectations for payrolls to increase by 60 thousand vs. 130 thousand in January. Private payrolls are expected to increase 75 thousand vs 172 thousand in January. The surprising upside beat in January was somewhat discounted by the market as the initial beat is expected to be downwardly revised which has been a feature of this report in the post-pandemic environment, so revisions will get almost as much attention as the February print. The unemployment rate is expected to return to 4.4%, after the surprising January strength sent it a tenth lower to 4.3%. Given the latest Fed speak, a stable unemployment rate represents a stable labor market despite the slowdown in new jobs, so we’ll see where that stands on Friday.

- A bonus this week will be the release of January Retail Sales, also on Friday, as the backlog from the government shutdown continues to be worked off. This will be a key report too as the surprising weakness in December sales put investors on the alert that the vaunted resilience of the US consumer may be taking a breather. The Personal Income and Spending Report from December also identified some softening in consumer spending in December so any further evidence of softness in January will be cause for some concern.

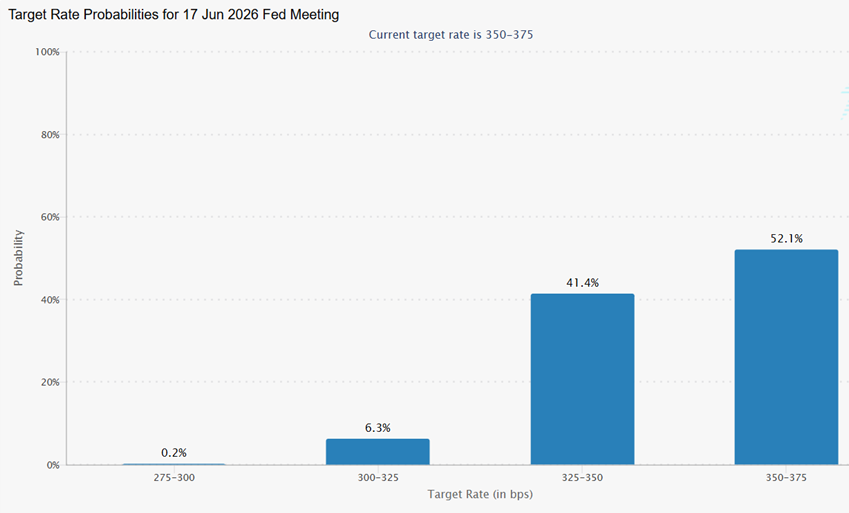

Odds of June Rate Cut Still Less Than 50% After Weekend Events Source: CME Group

Source: CME Group

US Consumes the Same Amount of Oil as in 1980 Yet GDP Nearly 4X – “Oil Intensity” is Lower

ISM Manufacturing Survey – Will it Maintain its Surprising Jump from January?

Source: ISM

ADP Employment Change for February Expected Similar to Improve from December

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.