Heavy Data Week Spars with War News

- We enter what is typically the busiest week of any month as far as first-tier economic data is concerned, but this week the economic data will spar with geo-political developments for investor attention. The Wall Street Journal is reporting plans to put US boots on the ground to extract enriched uranium stockpiles which would point to escalation. Meanwhile, President Trump said Iran agreed to let more oil tankers leave the Strait of Hormuz. So, those competing narratives open the week. The early price action is risk-on but also lower yields. There is some thought that with the latest troop movements this will not be the hoped for short affair. Instead, markets are beginning to consider a longer operation which will add to demand destruction along with widening the initial inflation concerns. Look for that issue to develop more fully this week. Currently, the 10yr is yielding 4.37%, down 7bps, while the 2yr is yielding 3.86%, down 6bps on the day.

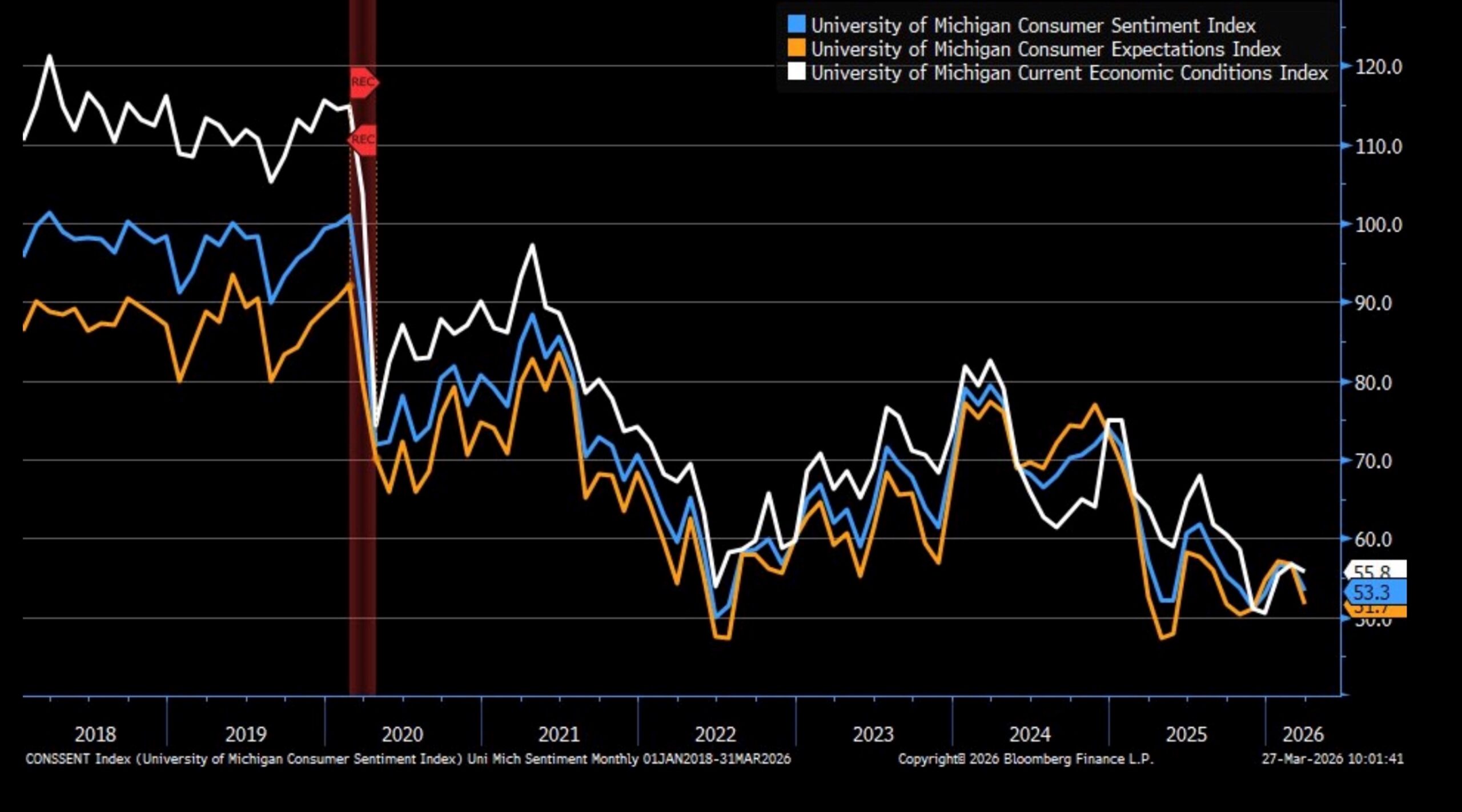

- Before we dig into some of the economic data on offer this week, let’s look back at the University of Michigan Sentiment Survey from late Friday morning. This was the final report of the week, and it revealed a clear downturn in sentiment as war developments, and the cost impact, weighed on consumers.

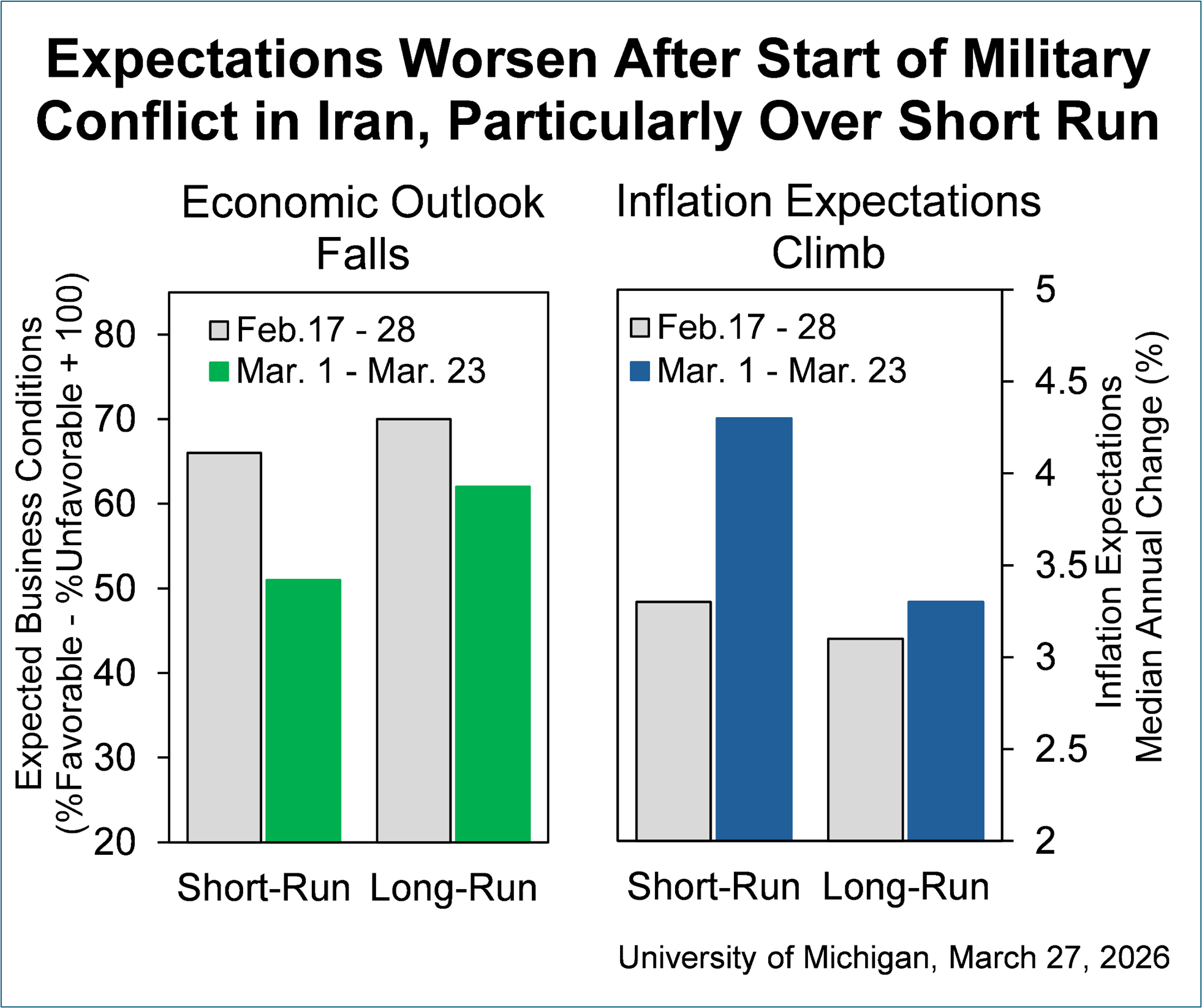

- The final University of Michigan Index of Consumer Sentiment came in at 53.3, significantly below the preliminary 55.5 and February’s 56.6. It also missed the 54.0 expectation. That’s a 6% monthly decline and the lowest reading since December 2025. Interviews for this survey were collected between February 17 and March 23, with about two-thirds completed after the start of the Iran war. Middle to higher income consumers with stock wealth were particularly affected as escalating gas prices and volatile financial markets led to a large drop in sentiment. Overall, the short-run economic outlook plunged 14%, and year-ahead expected personal finances sank 10%. Longer-run expectations declined too but the drop was more subdued. These patterns suggest that, currently, consumers do not expect recent negative developments to persist far into the future. If the Iran conflict becomes protracted, or if higher energy prices pass through to overall inflation, then those longer-term sentiments will likely deteriorate.

- Year-ahead inflation expectations climbed from 3.4% in February to 3.8% this month, the largest one-month increase since April 2025. The current reading exceeds those seen in 2024 and remains well above the 2.3-3.0% range seen in the two years pre-pandemic. Long-run inflation expectations inched down to 3.2%. In 2024, values ranged between 2.8% and 3.2%, while in 2019 and 2020, they were consistently below 2.8%. It should be noted that for both time horizons, interviews completed after February 28th exhibited higher inflation expectations than those completed before that date (see graphs below).

- Turning to matters economic, the first of the first-tier March reports will be the ISM Manufacturing Survey on Wednesday with the headline reading expected to tick slightly lower from 52.4 to 52.1. After spending all but January 2025 below the 50 dividing level, it bounced to 52.6 in January and continues to remain above the dividing line between an expanding and contracting sector, but it’s been unable to move above the January bump. The other readings within the report, Prices Paid, New Orders, and Employment will get plenty of scrutiny along with the headline reading as well.

- Before that March data, we’ll get a pair of important February reports. Tomorrow, brings the latest JOLTS (Job Openings and Labor Turnover Survey) and Wednesday brings the latest Retail Sales Report. First, JOLTS is expected to see the headline job openings level dip slightly from January’s 6.946 million to 6.800 million. That level is well off the post-pandemic high of 12 million but has resisted moving substantially lower from recent prints as it hovers near the total unemployed level. The Quits Rate (voluntary separation to total employed) has been stable at 2.0%, like pre-pandemic rates, signaling that worker confidence in finding other employment remains decent.

- A bonus this week will be the release of February Retail Sales, also on Wednesday, as the backlog from the government shutdown continues to be worked off. This report is always important but doubly so recently as the softness in December and January sales put investors on alert that the vaunted resilience of the US consumer may be taking a hit. Recall, January sales were down -0.2% as auto sales weakened but the direct GDP feed Control Group posted a solid 0.3% gain. We’ll see where those figures come for February, before the Iran hostilities began, which is a big caveat to this and other February reports.

- The March BLS Nonfarm Payrolls Report will be released on Good Friday with expectations for payrolls to increase by 51 thousand vs. a loss of 92 thousand jobs in February. Recall, the disappointing February print followed a surprising upside 126 thousand beat in January, so averaging the two together represents a monthly average of 17 thousand new jobs which may be closer to what the economy is currently generating. The unemployment rate is expected to return to remain at 4.4% for a second straight month after the surprising January strength sent it a tenth lower to 4.3%. Given the latest Fed commentary, a stable unemployment rate represents a stable labor market despite the slowdown in new jobs, so we’ll see where that stands on Friday.

- Finally, I sat down to chat with Billy Fielding, head of our Asset Liability Service, last week and discussed what he sees in the latest reports and what he’s hearing from examiners in the field when they review AL results and procedures. It was an interesting discussion so give it a listen here.

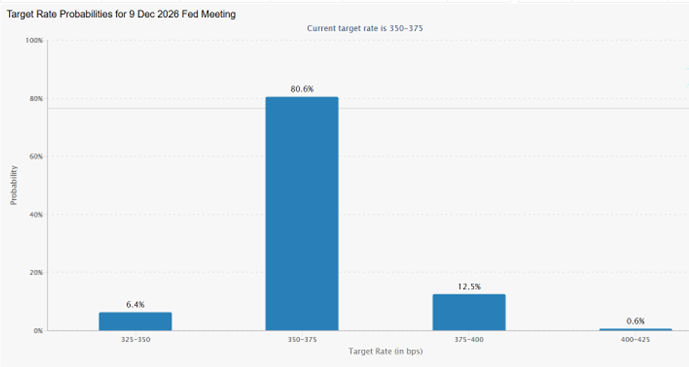

81% Odds of No Rate Cuts this Year, 12.5% Odds of a Rate Hike  Source: CME Group

Source: CME Group

Univ. of Michigan – March Sentiment Reading Due Later This Morning

Source: Univ. of Michigan

Source: Univ. of Michigan

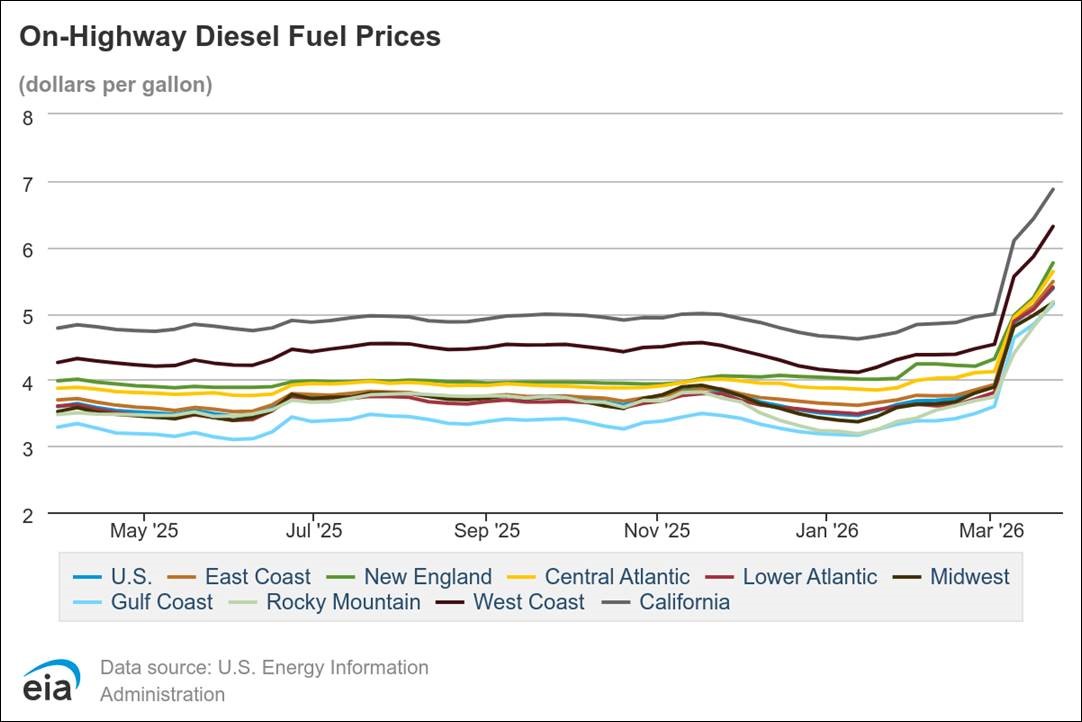

Forget Gas, Diesel Prices Already Well Above $5/gallon – That Will Impact Shipping Costs Soon

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.