Inflation Angst is Not Going Away

- Investors continue to focus on the inflation aspect of the war and that contributed to a poor 2yr Treasury auction yesterday, despite a nearly 50bps increase in yields this month. At some point, inflation angst will compete with demand destruction from higher costs which should limit the upward bias of yields, but for now that battle hasn’t been engaged. Below, we discuss March PMI data that speaks to increasing price pressures, and also signs that demand is faltering some, at least on the services side of the economy. At some point that flagging demand will garner more attention from investors, but that day wasn’t yesterday. Also discussed below, February import prices were released this morning and will provide a baseline from which subsequent war-related costs will be added in future reports. Meanwhile, the Treasury will be selling $70 billion in 5yr notes today at the highest yields since last June. That fresh supply, and investor reluctance, points to more yield concessions on the horizon. Currently, the 10yr is yielding 4.33%, down 6bps, while the 2yr is yielding 3.88%, also down 6bps on the day.

- Despite yields increasing nearly 50bps in March, yesterday’s 2yr Treasury auction was weak, indicating continued hesitancy on the part of investors. Yesterday’s sale came 2.0 bps above the market yield, while non-dealer bidding (an indicator of investor interest) was also weak at 75.9% vs. an 89.3% average. The bid-to-cover ratio at 2.44 was the weakest in nearly two years, also indicating hesitant demand. A 4-handle yield looms just overhead and that psychologically strong level may prove too much to resist before more bullish trading conditions emerge, or the war and its cost pressures start to recede.

- The preliminary S&P Global PMIs for March saw business activity slow as surveys reported a slightly weaker upturn in new orders and spike in prices following the outbreak of hostilities with Iran. Between the service sector and manufacturing the service sector was harder hit as manufacturers reported an upturn in output and new order book growth. The manufacturing PMI rose from 51.6 to 52.4. Meanwhile, the services sector PMI dipped from 51.7 to 51.1. The composite index, driven by the weakness in services, fell from 51.9 to 51.4, an 11-month low. Although the latest reading is above the 50-equilibrium point, the March decrease pointed to a slowing growth rate for a second straight month and completes the weakest quarter in more than two years.

- Expectations displayed a similar divergence with a weaker outlook among service providers contrasting with a more upbeat perspective among manufacturers. The latter were boosted by fewer tariff related worries, but overall private sector confidence declined and contributed to the first fall in employment in over a year. In a sign of further inflation worries, average input costs rose by the largest monthly increase in ten months which led to the largest average selling price increase since August 2022. A combination of war-related energy cost increases and tightening supply conditions led to the upward pricing pressure.

- Chris Williamson, Chief Business Economist at S&P Global Market Intelligence summarized the report, “The flash PMI survey data for March signal an unwelcome combination of slower growth and rising inflation following the outbreak of war in the Middle East. Companies are reporting a hit to demand from the additional uncertainty and cost of living impact generated by the conflict. Travel, transport and tourism related issues are compounded by financial market jitters and affordability constraints, notably including concern over the impact of higher interest rates, surging energy prices, and supply chain delays. The PMI data are indicative of GDP rising at an annualized rate of just 1.0%, with a modest 1.3% expansion signaled for the first quarter.” The Atlanta Fed’s latest GDPNow has first quarter GDP at 2.0%, but the estimates have been coming down as hard data replaces more optimistic estimates. It should be noted that S&P also noted declines in preliminary PMI readings across Europe as the continent grapples with similar war-related cost issues.

- Speaking of rising costs, the final piece of February inflation data arrived this morning with the Import/Export Price Index and it’s not a pretty picture. Import prices rose 1.3% vs 0.6% expected and 0.6% in January (revised up from 0.2%). It’s the largest monthly increase since March 2022. Imports less petroleum rose 1.1% vs. 0.4% expected and 0.4% the prior month. The YoY rate increased to 1.3% vs. 0.4% expected and -0.1% the prior month. That’s the largest annual increase in a year. The February cost bump comes before the beginning of hostilities with Iran with that starting on Feb. 28. It will provide a baseline from which to assess war-related cost increases when we see the March and following months. Meanwhile, export prices increased 1.5% vs. 0.5% expected and 0.6% in January. On a YoY basis, export prices increased 23.5% vs. 2.6% in January. While these inputs into the PCE inflation series are relatively small, they will bump it higher, nonetheless. Core PCE for February is already estimated at 0.4% and today’s numbers will only add to that.

- Finally, the high frequency weekly ADP Pulse Employment Report continued to point to a modest level of job growth in March with 10 thousand new private sector jobs for the week ending March This compares to 9 thousand the prior week and continues a trend in the 8 to 12 thousand range per week. That implies a monthly rate near 40 to 50 thousand, like the March Nonfarm Payrolls expectation due on April 3.

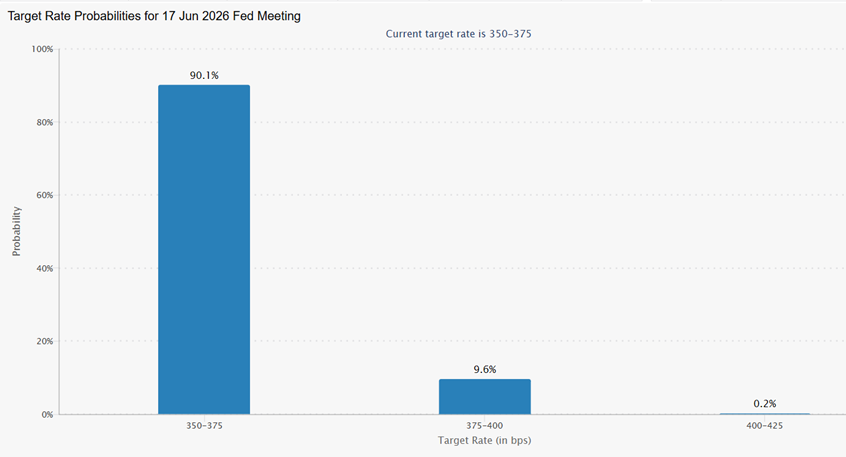

Rate Hiking Odds for June FOMC Meeting – Down Slightly from Monday Source: CME Group

Source: CME Group

2Yr Treasury Yield – Up Nearly 50bps in March Source: Bloomberg

Source: Bloomberg

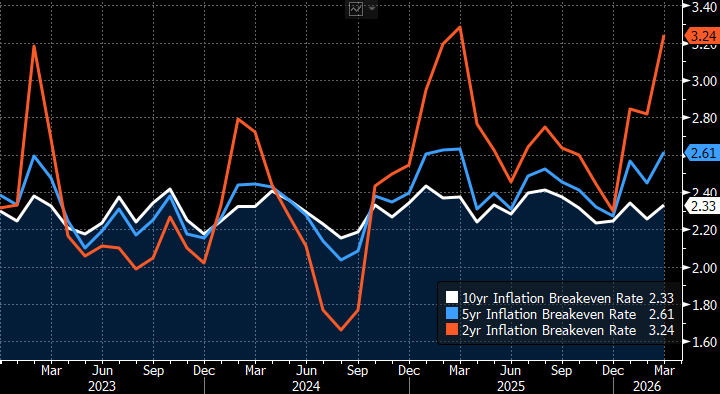

TIPS Inflation Breakeven Rates – Shorter Term Yields Jump Higher Reflecting Heightened Inflation Fears

Source: Bloomberg

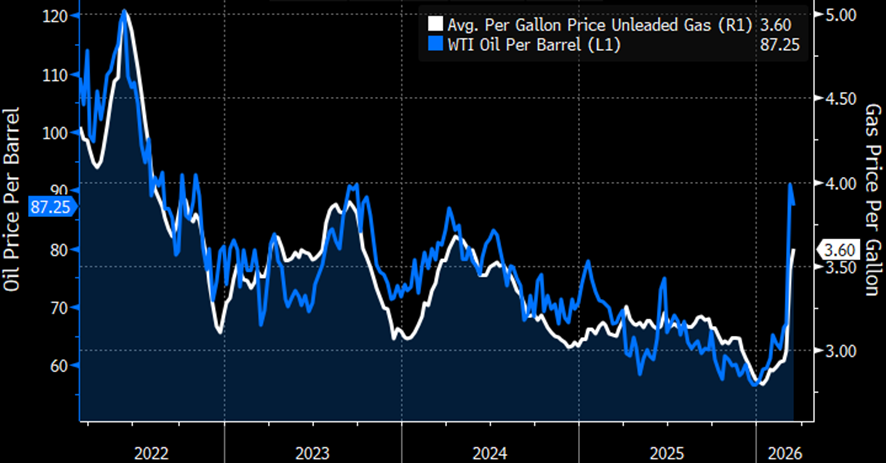

WTI Oil Leads Gas Prices Higher Source: Bloomberg

Source: Bloomberg

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.