Inflation Week Arrives

- The absence of a peace deal over the weekend has Treasuries on the back foot and equity futures waffling around unchanged levels as the week opens. Friday’s decent jobs report didn’t provide the spark for a Treasury selloff as investors took the headline beat but dug a little deeper to see a slight uptick in the unrounded unemployment rate, along with another decline in the labor force, and decided it wasn’t a slam dunk beat that the Fed’s inflation hawks were looking for. Anyway, speaking of inflation hawks, attention quickly turns this week to the April CPI report tomorrow, PPI on Wednesday, then Retail Sales on Thursday. So, plenty of data to digest in the coming week. Currently, the 10yr is yielding 4.39% up 3bps, while the 2yr is yielding 3.92%, also up 3bps on the day.

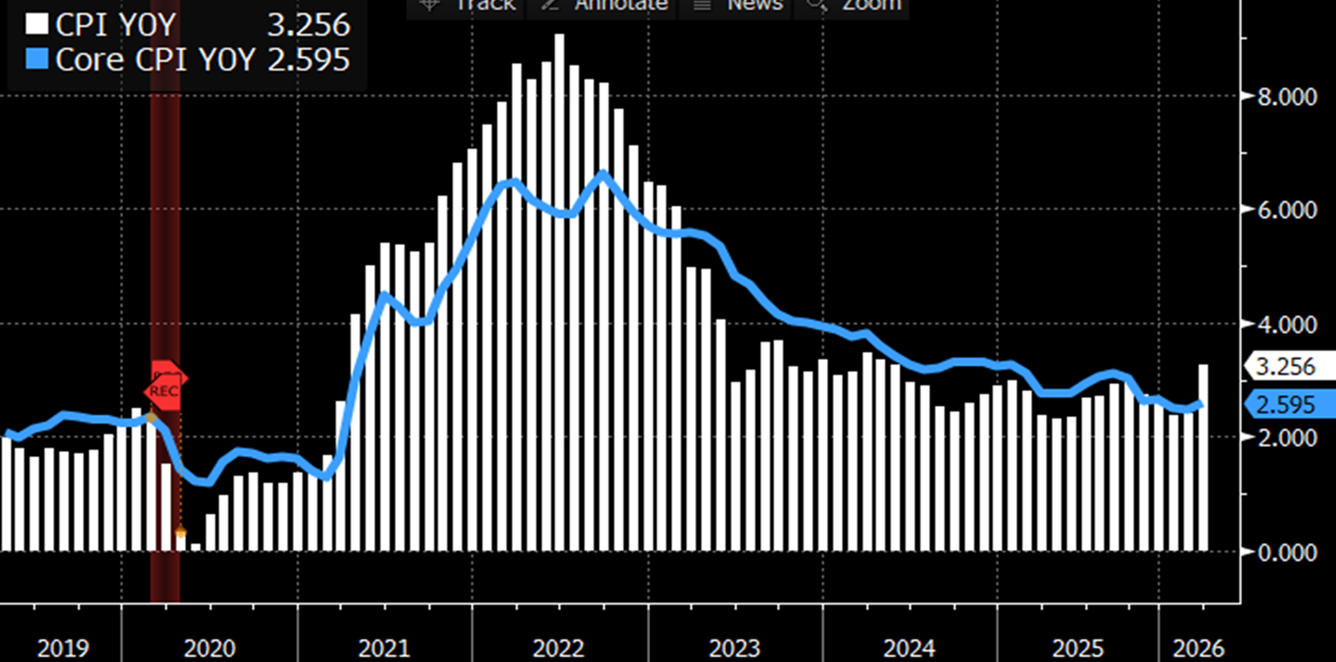

- After last week’s data deluge of labor market data, there’s no rest for the weary with April CPI set for tomorrow. Expectations are for headline inflation to increase 0.7% MoM with the YoY headline rate moving up from 3.3% to 3.8%, the highest since May 2023. Core CPI (ex-food and energy) is expected to increase 0.3% with the core YoY rate increasing a tenth from 2.6% to 2.7%. The bad news is that subsequent months will see a string of 0.1% and 0.2% monthly prints roll off. Thus, YoY rates are not likely to improve anytime soon. Thus, keeping core inflation under 3% YoY will be a challenge in the coming months.

- The inflation fun doesn’t stop there as we’ll get the April PPI Report on Wednesday. Expectations are that overall wholesale inflation is expected to increase 0.5%, same as March with the ex-food and energy rate increasing 0.3% vs. 0.1% in March. PPI ex-food, energy, and trade is expected to increase 0.2%, same as March. The overall YoY pace is expected to increase from 4.0% in March to 4.2%. Thus, wholesale price pressures look poised to continue pushing on retail prices in the coming months. Once we have CPI and PPI this week, analysts will start calculating estimates for PCE which will be released at month-end but expect more increases there as well.

- April Retail Sales on Thursday completes the major reports for the week with overall sales expected to increase 0.4% vs. 1.7% in March, driven by the gas surge. Ex autos and gas monthly sales are expected to increase 0.3% vs. 0.6% the prior month. The Control Group – a direct feed into GDP and considered a better core look at spending is expected to increase 0.3% vs. a robust 0.7% in March. The caveat we always offer for this report is that it’s not inflation adjusted so be careful with reading nominal increases especially in this period of heightened price pressure. In any event, with that warning, and pricing out gas purchases, sales are expected to be decent but not up to the solid March results.

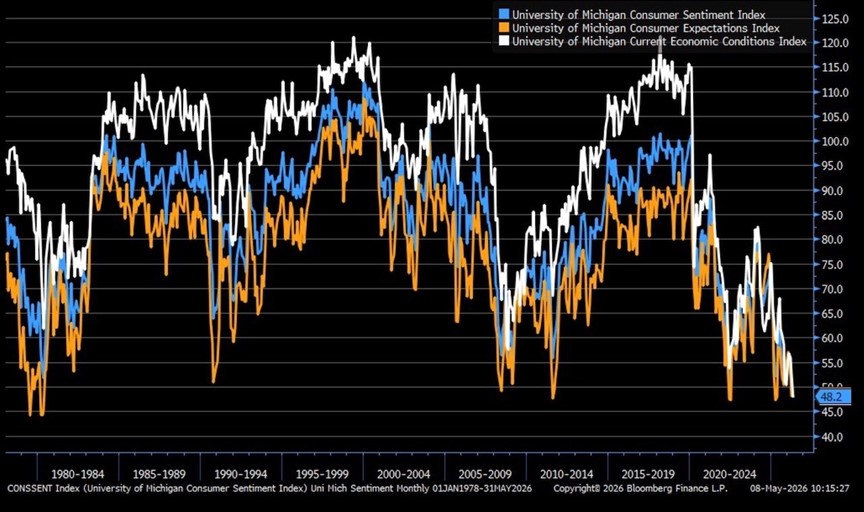

- Last Friday, we received the University of Michigan’s preliminary Sentiment reading for May. Overall sentiment dipped from 49.8 to 48.2. Expectations were for a nearly unchanged reading at 49.5. Current Conditions decreased from 52.5 to 47.8, widely missing the 52.0 expectation. However, consumer expectations rose from 48.1 to 48.5, beating the 48.2 expectation.

- The report noted that current conditions fell back due to a surge in concerns about high prices both for personal finances as well as buying conditions for major purchases. Real income expectations continued a decline that began in March. About one-third of consumers spontaneously mentioned gasoline prices and about 30% mentioned tariffs. Taken together, consumers continue to feel battered by cost pressures, led by soaring gas prices. The report concluded that ”Middle East developments are unlikely to meaningfully boost sentiment until supply disruptions have been fully resolved and energy prices fall.” That seems like a months away vs. weeks away development.

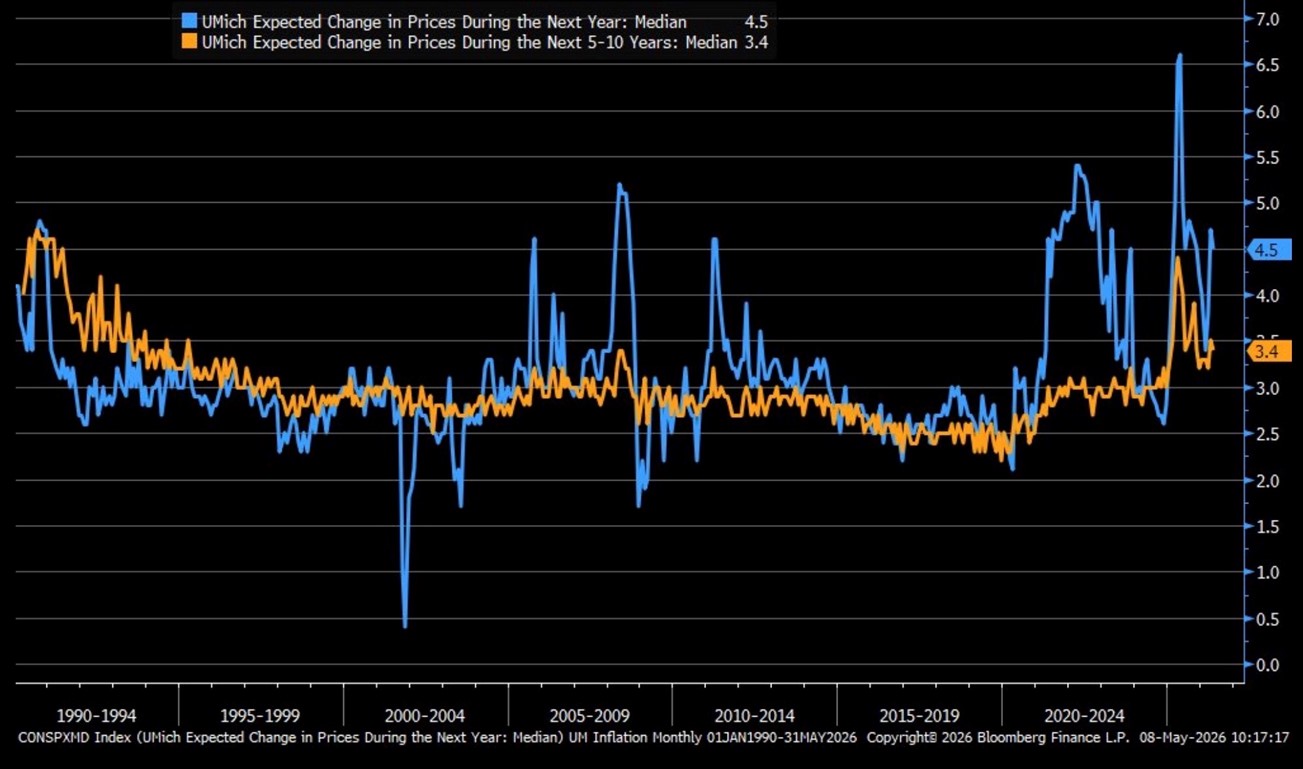

- Despite the increasingly dour sentiment outlook, year-ahead inflation expectations softened a touch from 4.7% to 4.5%. The current reading still substantially exceeds the 3.4% reading seen in February prior to the start of the Iran war, along with all 2025 readings and the 2.3-3.0% range seen in the two years pre-pandemic. Long-run inflation expectations inched down from 3.5% in April to 3.4% in May. In 2024, values ranged between 2.8% and 3.2%, while in 2019-2020, they were consistently below 2.8%. So, while inflation expectations edged down a bit from April, they remain well above pre-war levels and pre-pandemic expectations. That will be noted by the Fed inflation hawks.

April CPI Due Tomorrow – Expectations are for Overall at 3.8% and Core at 2.7% YoY

Source: BLS

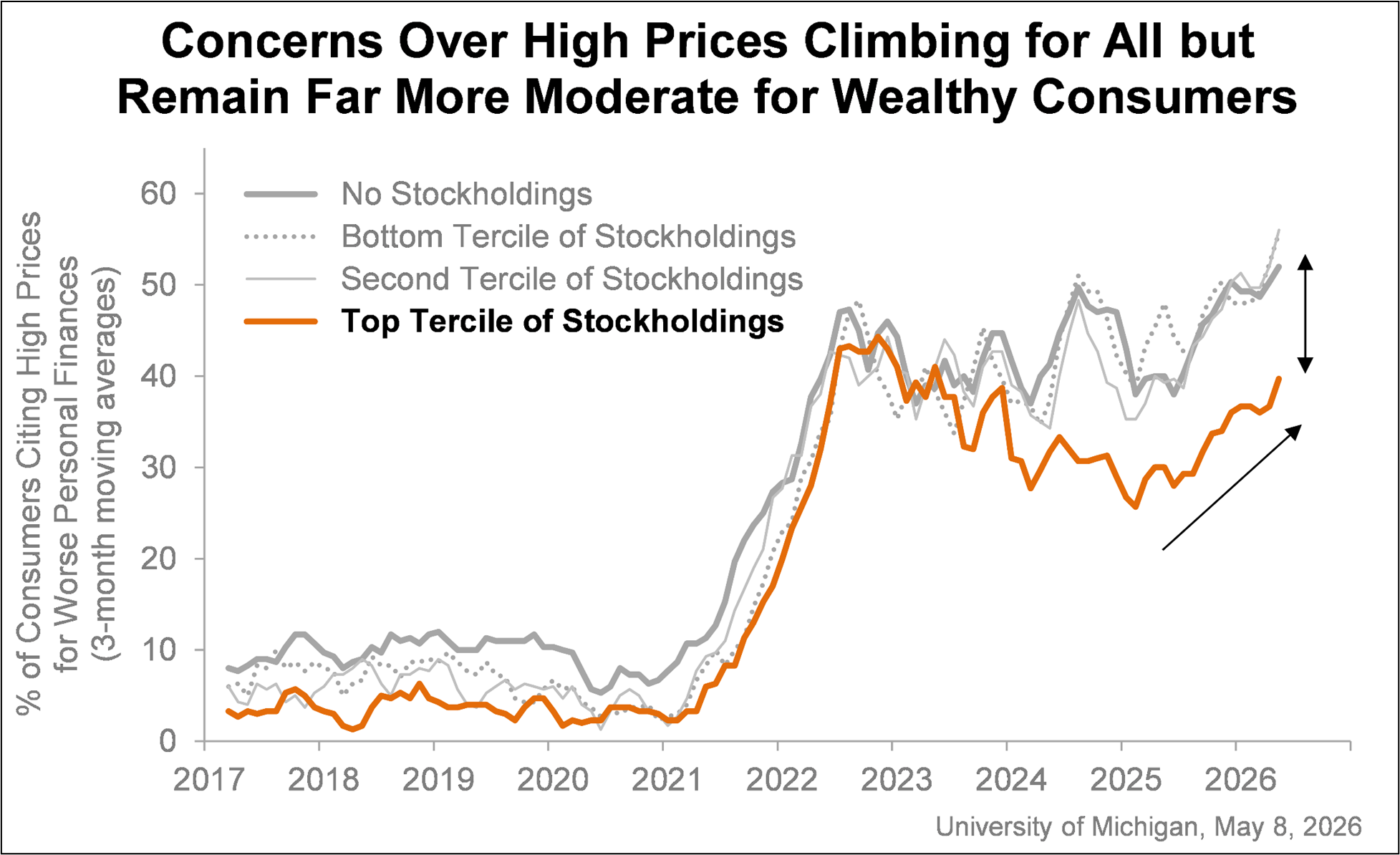

If You Own Equities, You’re Handling the Higher Prices a little Better

Source: Univ. of Michigan

Univ. of Michigan May Consumer Sentiment – Current Conditions Index Falls to Record Low Source: Univ. of Michigan

Source: Univ. of Michigan

Univ. of Michigan May Consumer Inflation Expectations – Edge Lower but Still Historically High

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.