Inflation Week Delivered

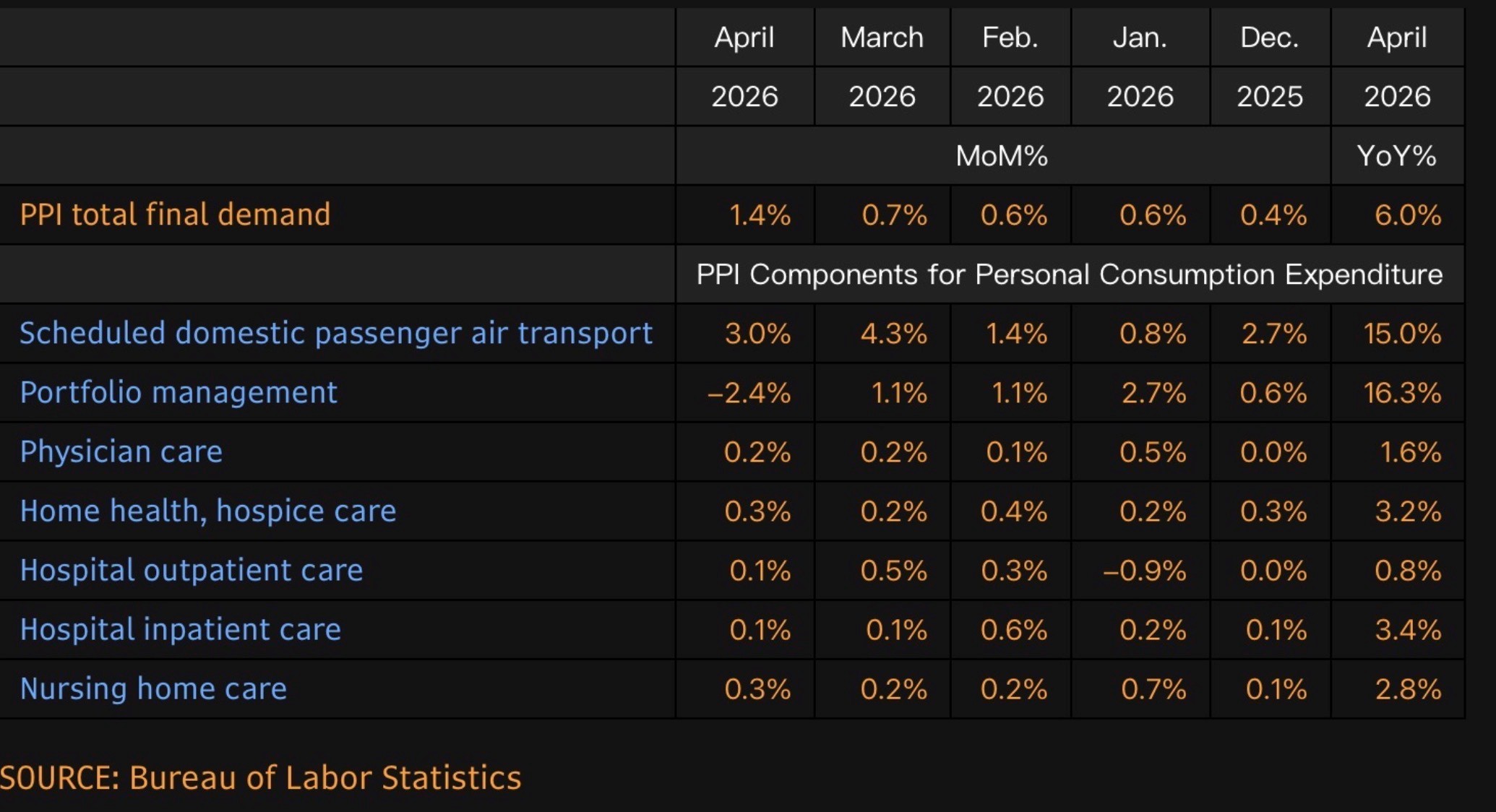

- Inflation week certainly lived up to its name and delivered some sobering news on prices. First, it was CPI, followed by PPI, and yesterday’s Import/Export Prices followed suit with steamy prices that extend beyond energy and energy adjacent goods and services. The Fed’s preferred inflation measure, PCE, is not due until May 28 and if there was any good news in the inflation numbers it was that the pieces that feed into PCE were not particularly hot, so the expectation of a 0.2% to 0.3% core PCE gain for April remains intact (see table below). What was perhaps the most telling bit of information during the week was the increase in goods and services prices that are not energy related. Thus, the passthrough of higher energy prices into other products/services is occurring faster than some expectations, and will no doubt continue in the months ahead. That, unfortunately, has yields moving higher with the 30yr bond yield reaching a 20yr high this morning (see graph below). Currently, the 10yr is yielding 4.54%, up 8bps, while the 2yr is yielding 4.05%, up 5bps on the day.

- Yesterday brought a trio of reports that touch on all the key areas right now. You want some more inflation numbers? We have the Import Price Report for April. You want the latest on the consumer? We have that with April Retail Sales. You want an update on the labor market? The weekly Initial Claims Report fits that description. And the report’s results continue to be a theme in all three areas: inflation is heading higher, the consumer continues to consume, and the labor market continues to signal stability.

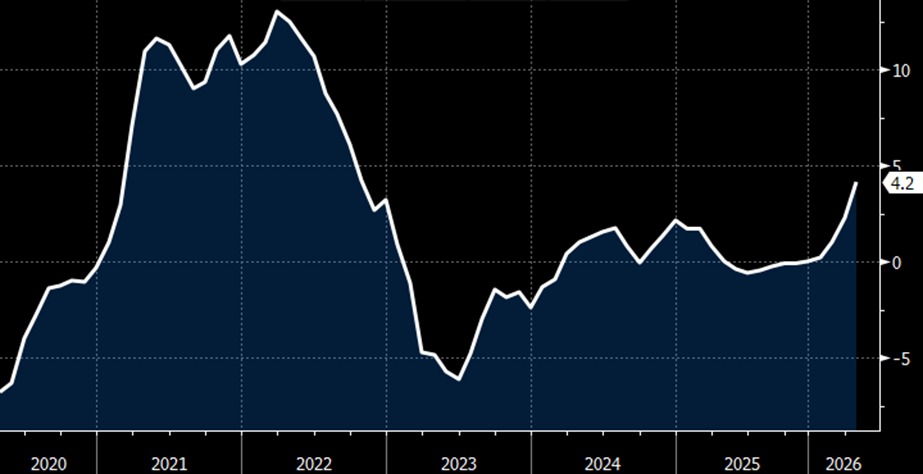

- First, the Import Price Index rose 1.9%, exceeding the 1.0% expectation and 0.9% March result. Even ex-petroleum the gains were strong at 0.7% vs. 0.5% expected and unchanged in the prior month. YoY gains increased from 2.3% to 4.2%, easily above the 3.2% expectation. It’s the highest annual gain since September 2022. If there’s any good news in the report it may be that foreign airfares were down 2.7% during the month vs. a 2.0% increase in March. That piece gets put into PCE so it may help keep that gain more manageable. Keep in mind too that these price gains are before tariff expenses, so it reflects true offshore pricing for domestic purchasers. Any tariff impact will be in addition to the price gains listed here. Export prices showed huge price gains as well, with the monthly gain at 3.3% vs. 1.5% in March. The YoY gain was a stout 8.8% vs 5.4% the prior month. The April report shows clearly that price increases stemming from the Iran war are global in nature and not just a domestic story.

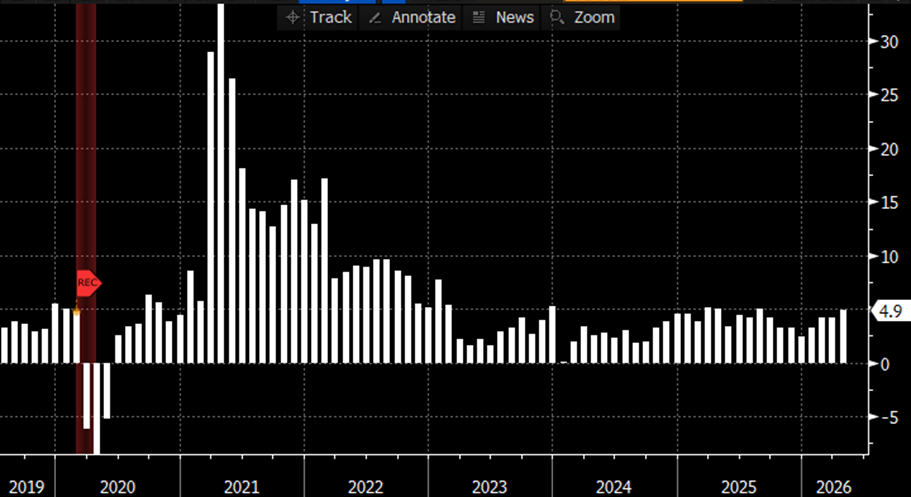

- Meanwhile, the latest Retail Sales Report was solid with no overt signs of the consumer buckling under the pressure of higher prices. Sales increased 0.5% for the month, matching expectations but were short of the 1.6% March gain. While higher gas prices are certainly a piece of that overall gain, sales ex autos and gas were still solid at 0.5%, beating the 0.3% expectation but short of the 0.7% March increase. The core spending category, Control Group, also posted a 0.5% gain, beating the 0.4% forecast but trailing the robust 0.8% in March. In summary, it was a solid if unspectacular month of spending by the US consumer, and while short of March gains were still respectable. That said, the spending was no doubt aided by tax refund checks, which will have less impact in May, but higher prices will remain. That’s something to be mindful of as we move into the summer months.

- Finally, Initial Jobless Claims remained relatively quiet with initial claims increasing from 199 thousand to 211 thousand with the 4-week moving average increasing slightly from 203.00 thousand to 203.75 thousand. While claims increased from the prior week, the weekly total remains low by historical standards and has yet to signal a material pick-up in layoffs. If there is another shoe to drop in labor market stability this indicator will be the first to signal that with a string of material increases that begin with a 3-handle and go up from there. Right now, the slight uptick in weekly claims is little more than the typical weekly variation but we’ll keep an eye on it in the weeks ahead.

- Continuing Claims were rather quiet as well with the May 2nd week seeing claims increase from 1.758 million to 1.782 million, just above the 1.780 million expectation. The series started the year at 1.900 million and has been in a gradual downtrend this year. Thus, while there were slight increases in both initial and continuing claims, the series has yet to signal a material increase in layoffs. Thus, the inflation hawks on the Fed will continue to point to labor market stability and keep rates unchanged for the foreseeable future.

30Yr Treasury Bond Yield Moves to 20Yr High Source: CNBC

Source: CNBC

Import Prices – Year-over-Year Change Moved into 2022 Territory Source: US Census Bureau

Source: US Census Bureau

April Retail Sales (YoY) – Consumption Remains Solid but Remember These Figures are not Inflation Adjusted Source: US Census Bureau

Source: US Census Bureau

PPI Components Used in PCE Calculation – While Headline PPI Was Hot, PCE Pieces Not So Much

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.