Is that Strait Open or Not?

- The week opens on a somber note with news of the passing of Alan Greenspan at the age of 100. Mr. Greenspan was the most influential Fed Chair of our lifetimes, and he left a legacy at the Fed that will last long after his passing. There will no doubt be plenty written this week on the legacy and accomplishments of the Chairman. Meanwhile, back to the here and now. While the MOU may have been signed, troubles have arisen almost immediately as Israel continues to hammer Hezbollah in southern Lebanon and that has the Iranians claiming a violation of the agreement, and thus, the Strait of Hormuz closed. At least that’s the Iranian version. The US insists the strait is open, so welcome to a new week, same as the old week? In any event, the new week does offer something of a reprieve on the data front and, of course, no FOMC meeting. The big report will be Thursday’s May PCE figures along with personal income and spending. Currently, the 10yr is yielding 4.48%, up 3bps on the day, while the 2yr is yielding 4.22%, up 4bps and the highest since Dec. 2024.

- After last week’s notably hawkish FOMC meeting, Fed speakers will be few this week with Fed Governor Chris Waller slated to speak this morning. He is scheduled to open a conference on the international role of the US dollar, so he may not offer thoughts on last week’s FOMC meeting, but he’ll no doubt offer up an opinion soon, if not today.

- New Fed Chairman Kevin Warsh surprised markets with a decidedly hawkish view of monetary policy, and one that may have surprised his boss. If one were paying attention, however, Warsh has been a noted inflation hawk from way back. We recall his time as Fed governor during the Great Financial Crisis. Then, the Bernanke-led Fed was engaged in moving rates to zero to provide a buffer for economic recovery during the depths of that crisis. Warsh, however, was a vocal critic against such a move, worrying about the potential inflationary impact it could have. Warsh eventually relented and voted for the cuts, out of respect for Bernanke he noted, and his fears over inflation turned out to be misplaced. In any event, his inflation-fighting bias should have been clear, despite more recent comments that may have been fashioned to boost his Chair nomination odds.

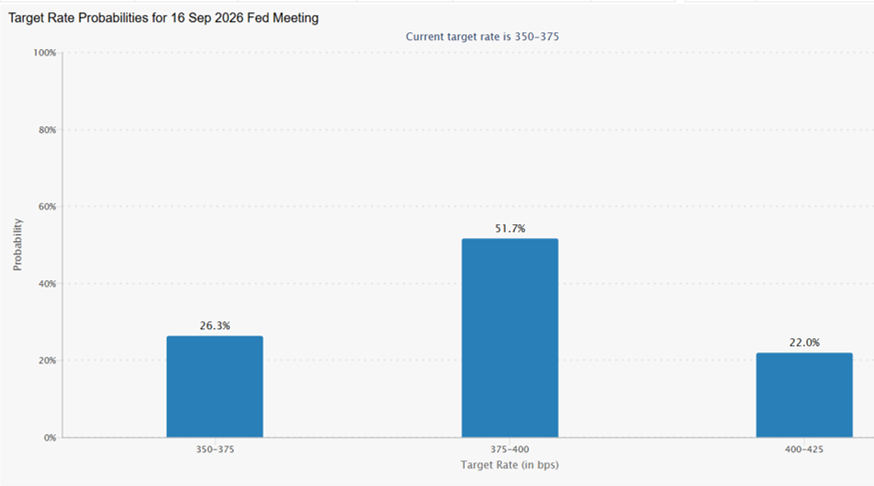

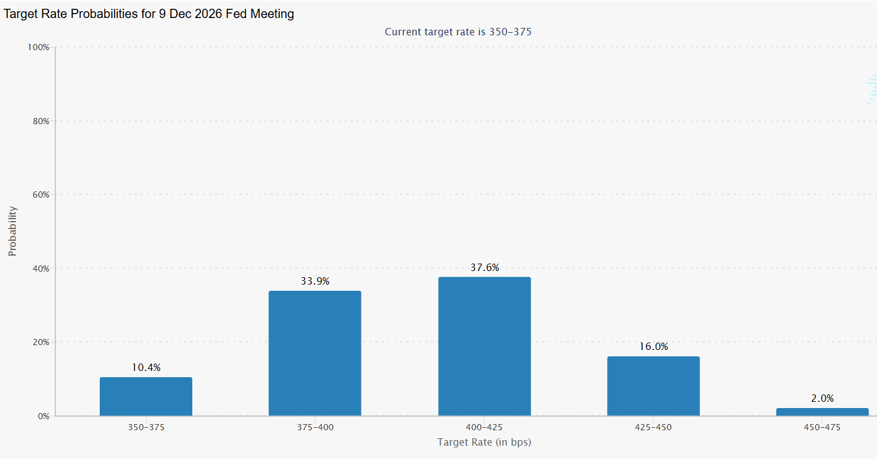

- There will be plenty more to digest on the Warsh front, but for now markets are settling into the view that the next move will be a hike, and it may come as early as September. The market has rate hike odds just over 50% for that meeting and are priced over 50% for two or more hikes by the end of the year (see graphs below). That has led to flattening in the 2-10s curve as short rates reprice higher, accommodating the more hawkish view, with longer rates biased lower due to the same inflation-fighting focus. With the status of the MOU and transits through the strait still in a fragile state, trying to game out when higher prices in the energy complex may begin to recede on a more permanent basis remains a game of chance more than anything else. Thus, moves on the longer end of the curve will be on a short leash until those uncertainties are resolved.

- While the big report this week will be the May Personal Income and Spending release, along with its PCE inflation series, an earlier report will get some attention with tomorrow’s S&P Global Preliminary PMIs for June. Last month, the Manufacturing PMI printed at 55.1, the Services PMI at 50.7, and the Composite at 51.5. Those levels will be compared to the latest findings in addition to the level of prices paid, employment, and new orders in each category. Continued price pressure and any indication of weakening orders and/or employment will be early yellow if not red flags.

- While the manufacturing headline was solidly in expansion territory, commentary noted much of that strength was pulling forward in orders as a precaution against further price increases. We’ll see if that activity persisted in June. Meanwhile, the previous strength in the services sector slipped, but remained just into expansion territory. A key question from this report will be if services rebounded in June, or whether momentum continued to slip.

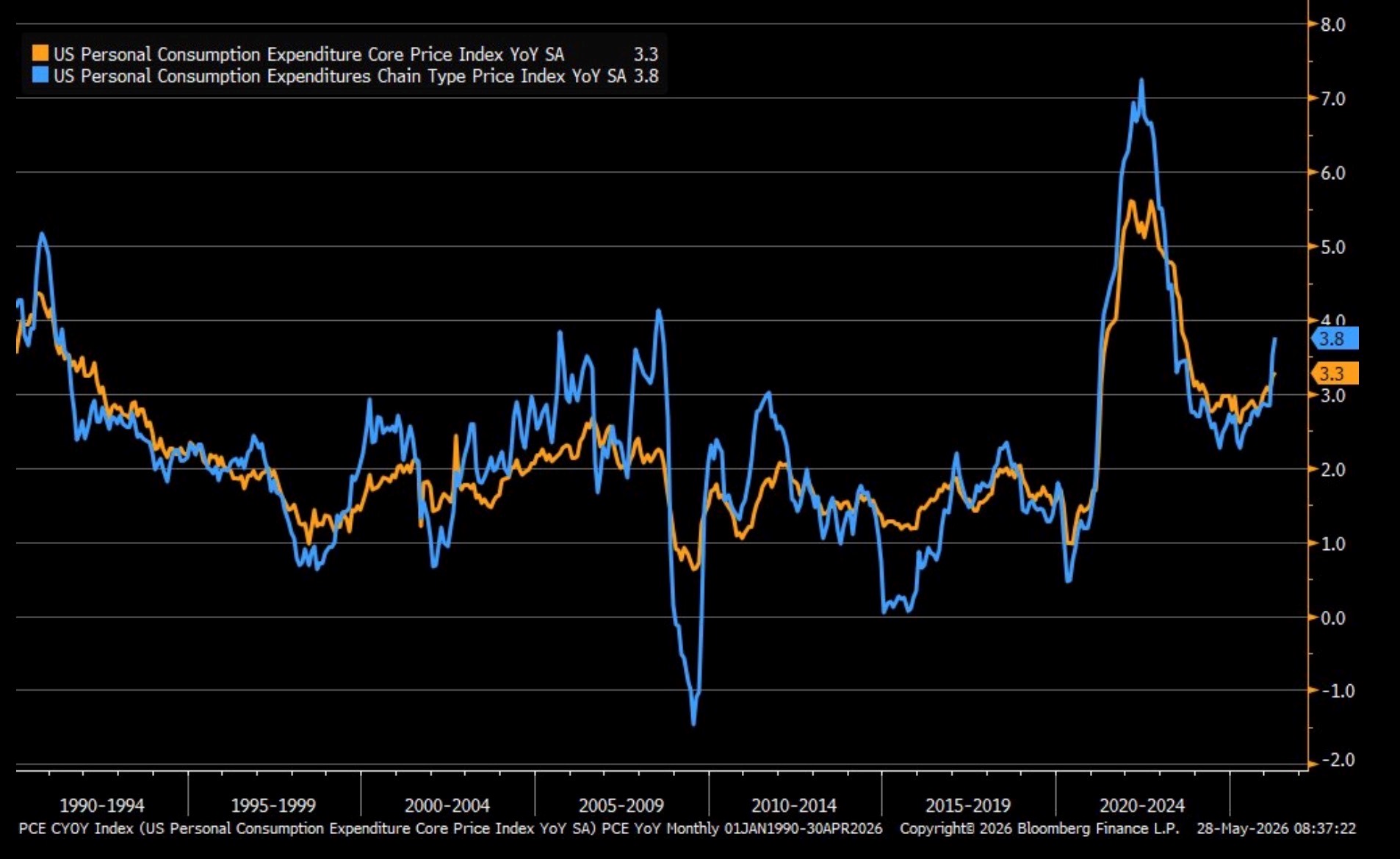

- Thursday brings the release of the personal income and spending numbers for June. Recall, in May incomes were flat due to softness in farm income, but wages/salaries continued to increase in the 0.3% to 0.4% range. Meanwhile, personal consumption was up a seemingly strong 0.5% but adjusted for inflation reflected a more pedestrian 0.1% increase. Headline PCE was up 0.4% in May and 3.8% YoY, while core PCE was up 0.2% and 3.3% YoY. It’s expected that core PCE will be up 0.3% in June, but could tick higher to 0.4%, with the YoY moving into the 3.5% range. So, a hotter inflation picture is expected, and one that plays into the hawkish FOMC message from last week.

- If it looks like ship/cargo traffic will resume shortly in the SoH, a hotter inflation report may be labeled as the eye of the storm passing, but any backsliding in the Middle East will keep rate-hiking odds for September and more in December firmly in place. Thus, the market remains in the grasp of Middle East developments rather than economic fundamentals. Sound familiar?

Futures Point to September Meeting for First Rate Hike Source: CME Group

Source: CME Group

Futures for December See Another Hike, or More Source: CME Group

Source: CME Group

Fed’s Preferred Inflation Measure Gets Updated on Thursday with Higher YoY Rates Expected

Source: BEA

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.