January CPI Cooler Than Expected

- With the brief government shutdown from two weeks ago, we had a unique experience with a jobs and inflation report in the same week. While both are not likely to alter a rate decision in March, it was a curious development to see the key reports for both the Fed’s dual mandates arrive within days of each other. We discuss the CPI report in detail below, along with a look at the latest jobless claims data. Currently, the 10yr is yielding 4.16%, down 1bp, while the 2yr is yielding 3.52%, also down 1bp on the day.

- Today’s January CPI was a positive affair, close to expectations with a slight downward tilt, that has investors focusing now on the labor market for clues regarding the next Fed rate move. Overall inflation increased 0.2% for the month vs. 0.3% expected with the YoY rate down three-tenths to 2.4%. Meanwhile, core CPI came in at 0.3% (0.295% unrounded) MoM, matching expectations with the YoY rate down a tenth to 2.5%, also matching expectations. The issue from here is that the next several months see a string of 0.1% and 0.2%MoM prints from last year rolling off and that will make it hard for YoY rates to improve unless the new prints come in lower and that will be a challenge.

- Shelter cost rose 0.2% vs. 0.4% in December as lodging expenses decreased 0.1% after jumping 2.2% the prior month. Meanwhile, Owners’ Equivalent Rent (OER) rose 0.2% vs. 0.3% the prior month. That puts it in the 2.5% to 3.0% annual range which is back to pre-pandemic levels. Some further improvement here is possible, but it will probably be grudging at best. One issue is the BLS decision coming out of the shutdown to roll forward pricing for 2 of the 6 geographic regions that didn’t get refreshed valuations in October and November. Thus, while the notoriously lagging OER has started to roll downward, the process was slowed due to the lack of data collection during the shutdown. The regions that weren’t updated must wait until April and May when the next semi-annual pricing refresh for their regions are conducted.

- One lingering concern is core services printed higher in January. For the month, core services rose 0.4% vs. 0.3% in December. With a combined weighting of 61% in CPI, it needs to fall into the 0.2% monthly range for the overall inflation level to continue to trend towards 2.0%. Core services ex-housing, the so-called Super Core, was 2.67% YoY, not dissimilar from the 2.70% in December. Bottom line, determining when the Fed will cut rates again is becoming more a function of the state of the labor market and less about prices as those are moderating with improvement likely in the months ahead.

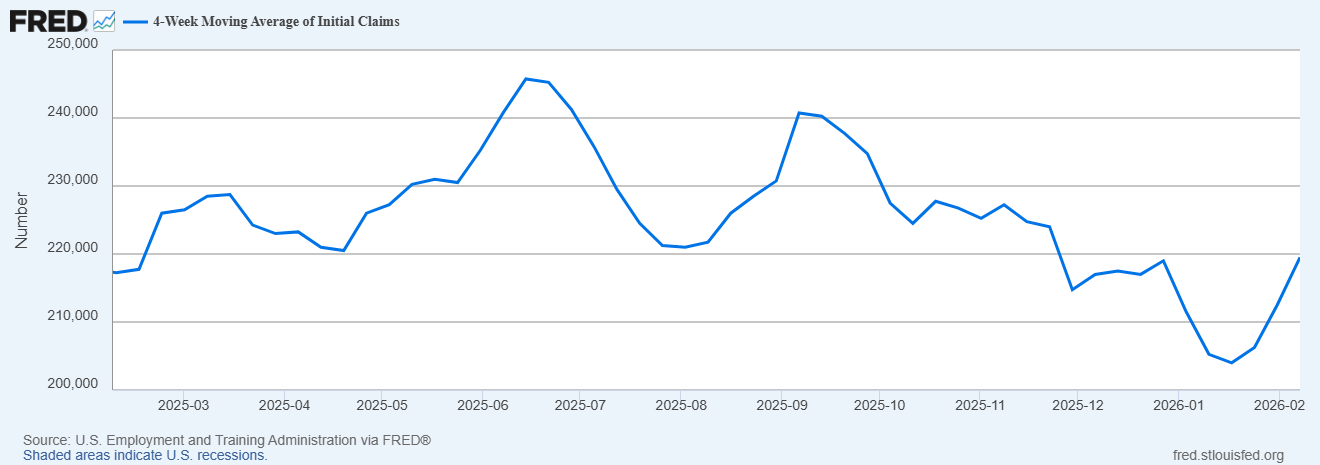

- Yesterday, we received the latest read on initial jobless claims. Recall, last week saw a moderate jump in claims for the week ending Jan. 30 so it came after the BLS survey period for January payrolls. Thus, watching weekly claims numbers to see if they continue to climb would be an early tell that the labor market is, despite the January payrolls print, losing momentum. With that backdrop, for the week ending February 7, initial jobless claims totaled 227,000, a decrease of 5,000 from the previous week’s revised 232,000 (up from 231,000 originally reported). The 4-week moving average was 219,500, an increase of 7,000 from the previous week’s revised average (see graph below).

- Continuing claims for the week ending January 31 was 1,862,000, an increase of 21,000 from the previous week’s revised level. The previous week’s level was revised down by 3,000 from 1,844,000 to 1,841,000. The 4-week moving average was 1,846,750, a decrease of 3,250 from the previous week’s revised average. This is the lowest level for this average since October 5, 2024, when it was 1,845,750. Thus, the low-hire, low-fire environment that we’ve been in for a year appears to be continuing.

CPI and Core CPI (YoY) – Move into the mid 2% Range

Super Core (Core Services Ex-Housing) – Prices Stable at 2.7% YoY

Source: BLS

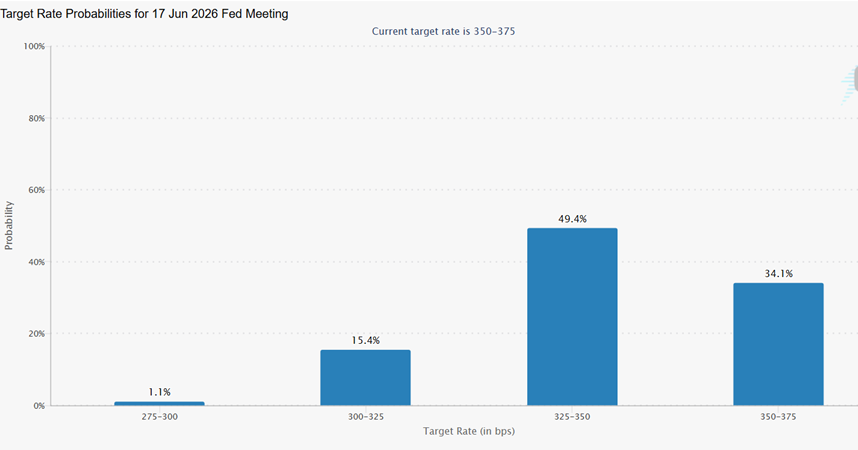

After CPI – Odds of a June Rate Cut at 66%

While Initial Claims Continues in Low 200K Level, 4-Week Average is Climbing

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.