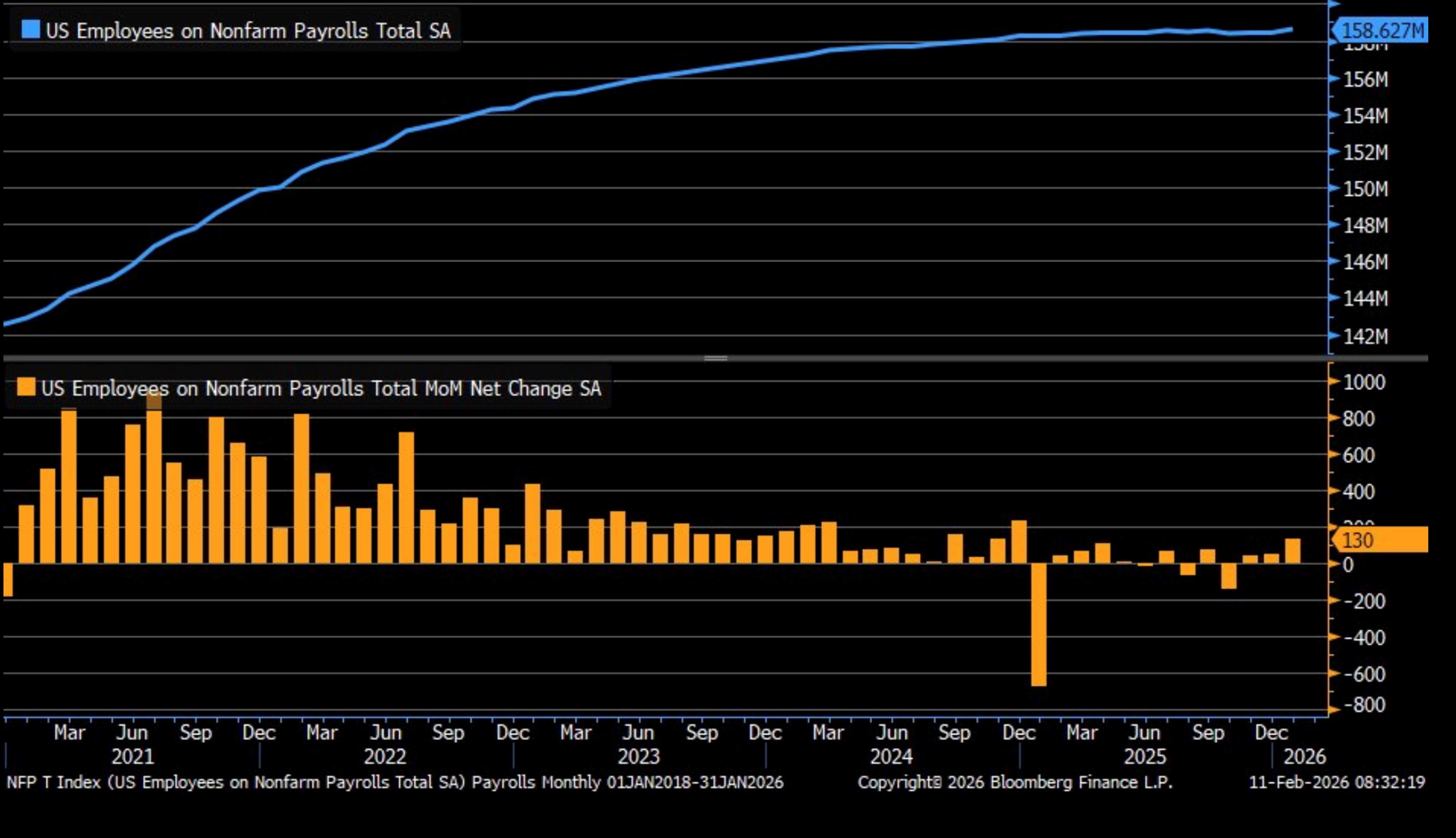

January Jobs Report Beats, Slicing Rate Cut Expectations

- January nonfarm payrolls rose 130 thousand, doubling the 68 thousand expected and 48 thousand gained in December (revised lower from an initial 50 thousand). Two-month revisions cut 17 thousand jobs from previous estimates with November revised 15 thousand lower and December 2 thousand lower. Private sector job growth was 172 thousand which is more than double the 70 thousand expected and 64 thousand increase in December. Fed Chair Powell recently said Federal Reserve staff estimated that BLS is overstating hiring by around 60 thousand per month; thus, the latest job growth number keeps us above water if that estimate is close to accurate.

- Speaking of revisions, this report carries the annual benchmarking revision for the 12 months ended March 2025. The initial estimate of the revision, released last fall, was for a 911 thousand reduction in previously reported job growth, or 76 thousand per month. Today, the actual revision is 862 thousand, or 72 thousand per month. The change in total nonfarm employment for 2025 was revised from +584,000 to +181,000 (seasonally adjusted). Thus, the average monthly change for 2025 was revised down to +15k from +49k before today’s update revision. The revisions have a few major sources, (1) low initial survey response rates from companies. They have three months to respond but the initial job estimates have been plagued by low responses that belatedly arrive, thus contributing to large revisions. (2) The BLS birth-death model of new and closing businesses has consistently overstated net business formation (and hence jobs) since the pandemic. (3) Seasonal adjustment changes given recent data patterns.

- The Household Survey, which is smaller than the Establishment Survey generates the unemployment rate, labor force participation rate, etc.. The survey reported an increase of 387 thousand people in the labor force (those employed and those not working but actively looking for employment) and a 141 thousand decrease in unemployed persons. The unemployment rate ticked a tenth lower to 4.3% (4.283% unrounded vs. 4.375% in December). Several Fed officials have pointed to this single metric as evidence of labor market stability so an improved figure will keep that group firmly in pause mode and that probably is the key takeaway from today’s report.

- Average Hourly Earnings rose 0.4% MoM, beating the 0.3% expectation which was also December’s gain. Despite the hourly beat, the year-over-year pace ticked lower to 3.7% from 3.8% in December. Average weekly hours ticked a tenth higher, beating the unchanged expectation, at 34.2 hours. Bottom line, with YoY wage gains moderating in the mid-3% range, wage-price inflation won’t be a Fed worry which also plays well with the rate pause crowd.

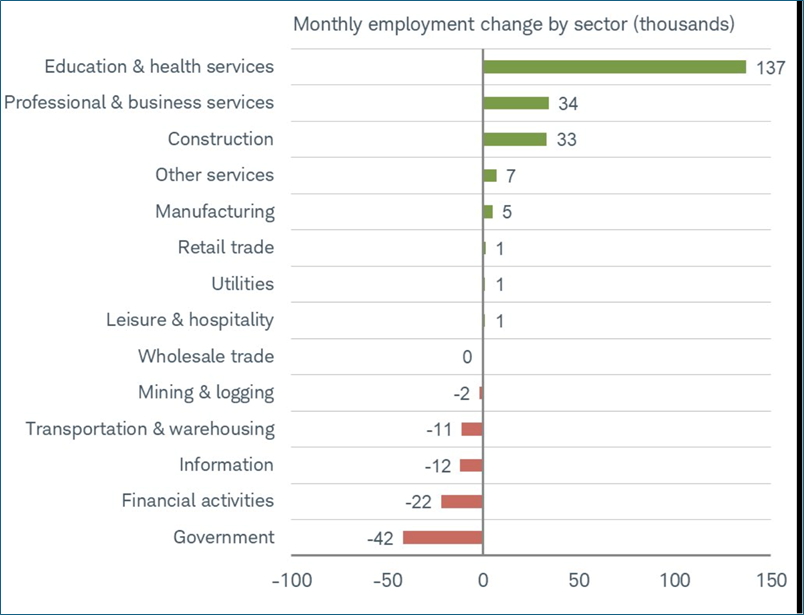

- The January jobs report beat expectations despite the myriad other reports that painted quite a different picture. The service sector continues to carry the bulk of job gains (136K service jobs vs. 36K in goods). The economy continues to lean on the mid to upper income consumer who continues to spend, although that seemed to be slipping some in December. Bottom line: the hiring machine rebounded in January and labor force growth returned as well which contrasts with recent trends of lower immigration totals and challenging domestic demographics. With those underlying fundamentals not changing, it does give one pause over this monthly rebound. That is, take it with a grain of salt. In any event, this report pushes any thought of a rate cut to a June or July event.

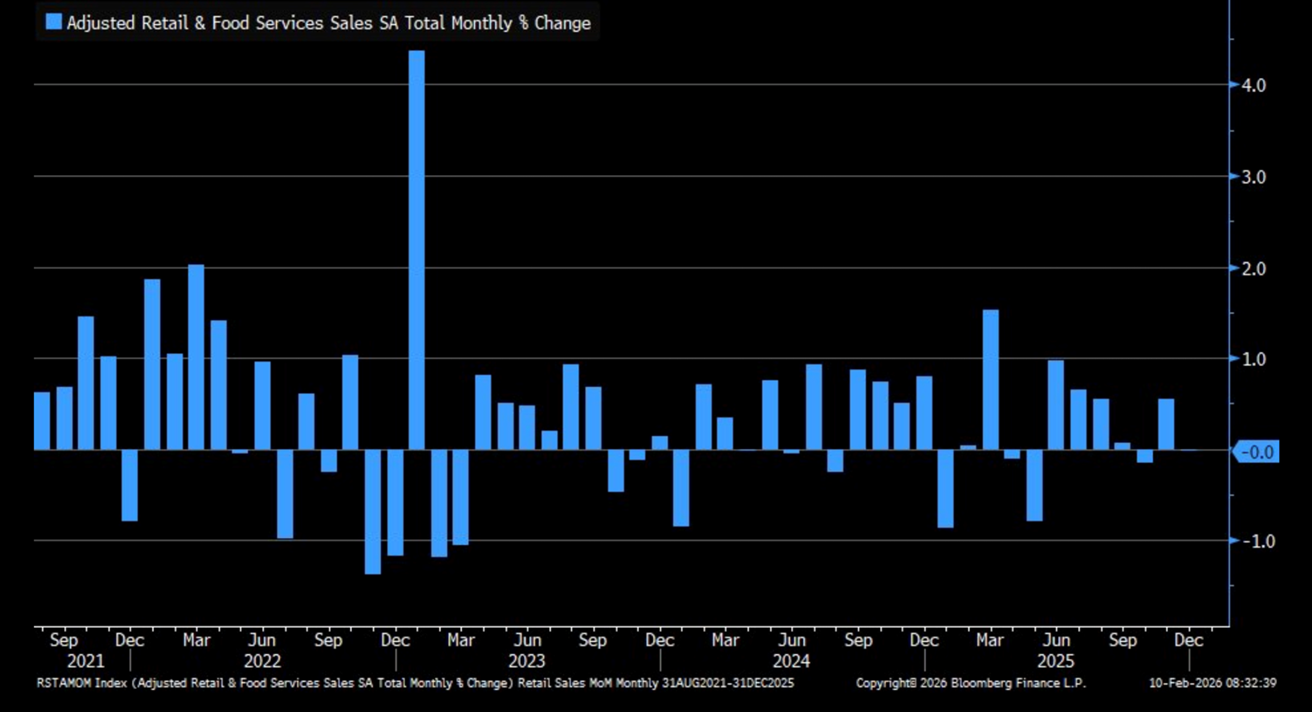

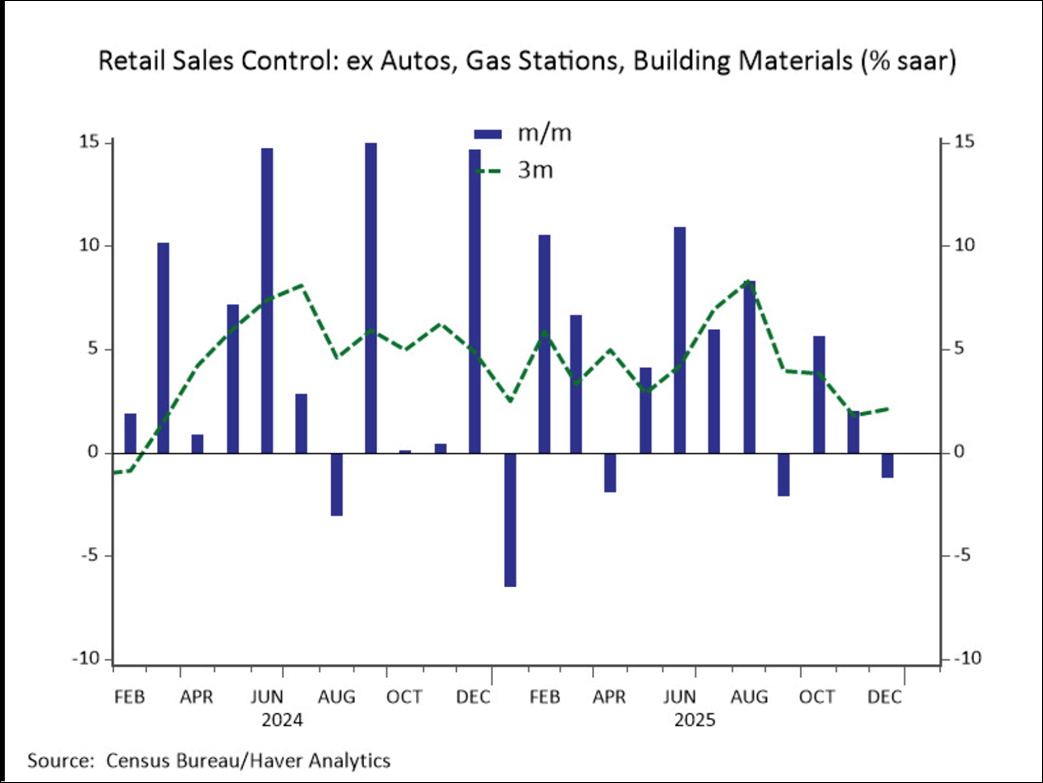

- As mentioned above, the economy has leaned on the consumer to carry the ball during the latest phase of this expansion. However, the December Retail Sales Report from yesterday painted a more sobering picture. Advance retail sales were unchanged for the month vs. 0.4% growth expected. Sales less autos were also unchanged as were sales less autos and gas. The Control Group, a direct GDP feed, fell -0.1% vs. 0.2% expected. In addition, the November result was revised from 0.4% to 0.2%. That combination put a dent in 4th quarter GDP estimates. The Atlanta Fed’s GDPNow Model now forecasts 4th quarter GDP at 3.7% from 4.2% prior. Thus, a shaky performance by the consumer in December for sure. The Census Bureau has yet to reveal a date for the January report as they continue to catch up from the October shutdown.

January Employment Gain Easily Beat Expectations

Service Side Jobs (Mostly Healthcare) Continue to Lead the Way

Source: BLS

Adjusted Retail Sales for December – Unchanged vs. 0.4% Expected

Retail Sales Control Group – Spending Slipping Lower

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.