January Personal Income, Spending, and Inflation

- With the Iran war looming over all aspects of trading, we finish the week with an important, albeit dated, report in the form of January Personal Income and Spending. The Fed’s preferred inflation measure is the headline feature of the report, but the personal spending numbers will get a once over too given the softening that was noted in the last two Retail Sales Reports and the December edition of today’s report. Currently, the 10yr is yielding 4.25%, down 2bps on the day, while the 2yr is yielding 3.70% down 6bps on the day.

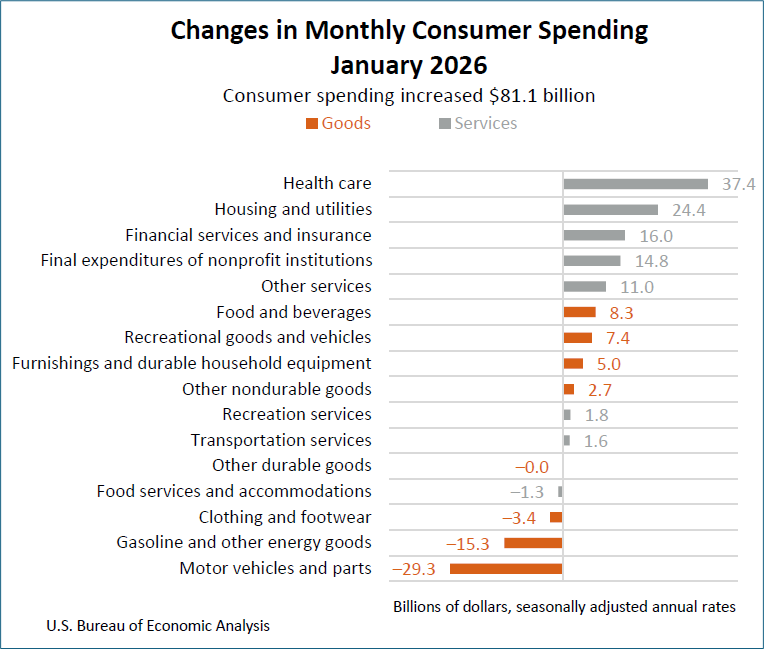

- As the agencies continue to play catchup with delayed reports from the October shutdown, today we received the January Personal Income and Spending Report. Personal income increased 0.4% vs. 0.5% expected and 0.3% in December. Personal spending increased 0.4% vs. 0.3% expected and 0.4% the prior month. Real spending – adjusted for inflation – was up 0.1% vs. 0.0% expected and 0.1% in December. Thus, today’s spending report was a bit stronger than the retail sales series as the top 5 categories of increased spending came in services (mostly essential vs. discretionary) while the retail sales report is heavier on goods reporting and less so on services.

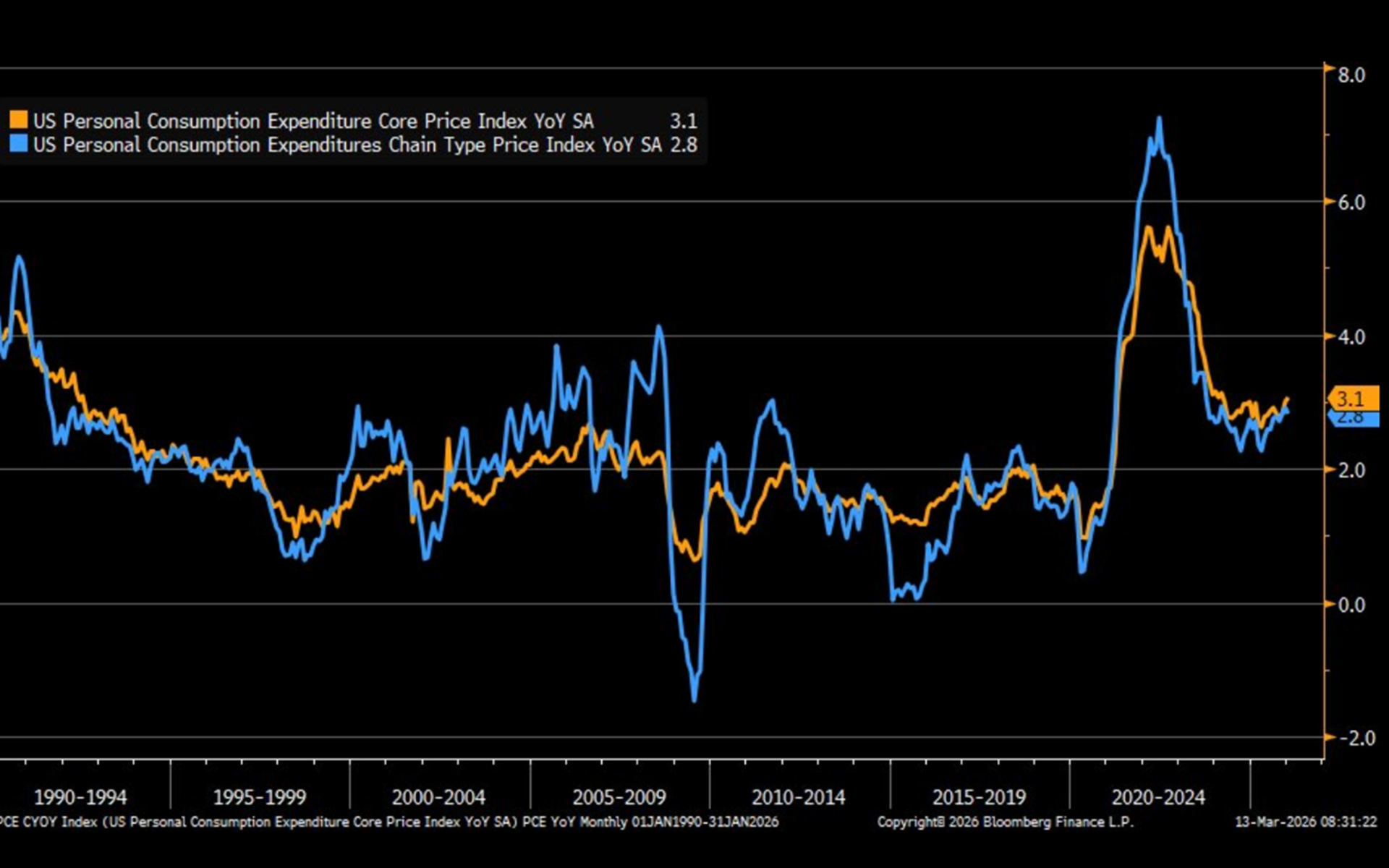

- On the inflation front, the Fed’s preferred inflation gauge, PCE, increased 0.3%, matching expectations and 0.4% the prior month. Core PCE (ex-food and energy) rose 0.4% (0.363% unrounded) vs. 0.4% expected and 0.4% in December. On a YoY basis, overall PCE advanced 2.8% vs. 2.9% expected and 2.9% in December. Core PCE YoY rose 3.1% vs. 3.1% expected and 3.0% the prior month. It’s the highest YoY pace since March 2024.

- YoY core PCE inflation bottomed last April at 2.61% and has been slowly climbing since and that upward bias continued into 2026. In addition, the YoY uptick in January occurred despite a 0.31% print rolling off from January 2025. February will see a 0.45% print roll off – highest in 2025 – but after that it’s a steady string of 0.1% or 0.2% prints; thus, lowering the YoY rate will by quite challenging after the February report. After the February CPI report, analysts are forecasting the February core PCE at 0.4%. And keep in mind, these reports are before any cost pressures from the war start to appear in the data. Thus, the inflation hawks on the FOMC appear to have the upper hand for the foreseeable future.

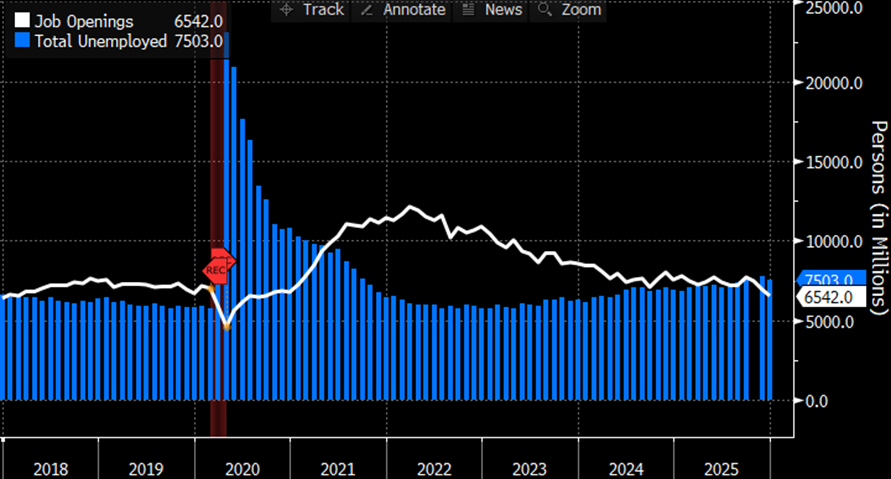

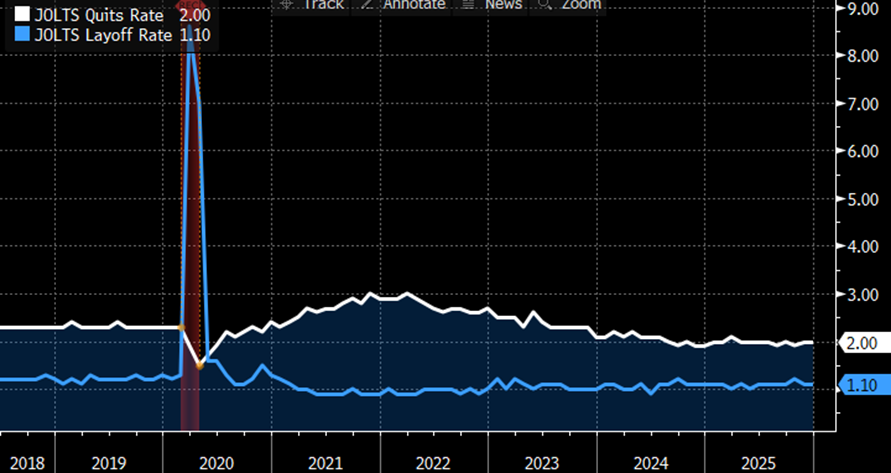

- At 10am ET, the other Fed mandate of full employment will get some attention with the January Job Openings and Labor Turnover Survey (JOLTS). Expectations are that job openings crept higher from 6.542 million to 6.750 million (see graph below). Job openings have been decreasing since early 2022 and the December print was the lowest openings number since September 2020. So, some type of rebound in the openings number would add credence to the Fed’s belief that the labor market is stabilizing. The Quits Rate (those voluntarily leaving as a percent of total employed) and the Layoffs Rate (layoffs as a percent of total employed) are both expected to hold steady at 2.0% and 1.1%, respectively.

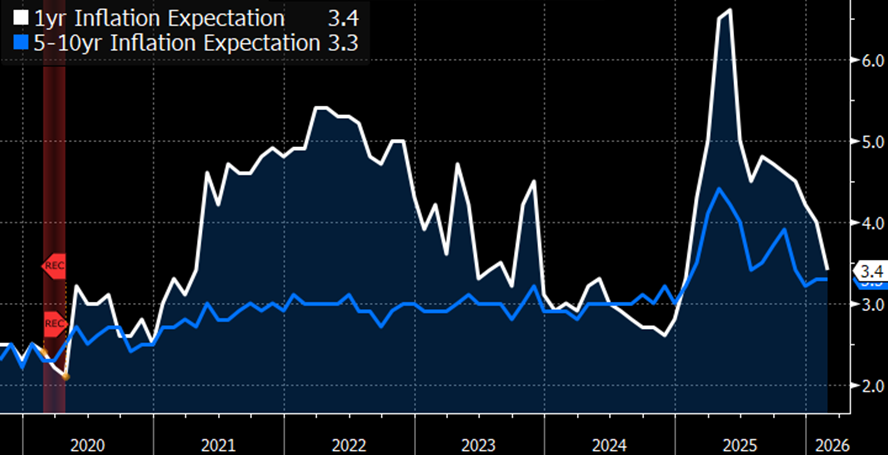

- Finally, the University of Michigan will release its preliminary March sentiment findings at 10am ET. Consumer sentiment is expected to slip from 56.6 to 54.6 with similar slippage in the Expectations and Current Conditions metrics. Year-ahead inflation expectations are expected to jump from 3.4% to 3.7% as war jitters start to arrive in the data. Long-run inflation (5yr – 10yr) expectations are forecasted to inch up from 3.3% last month to 3.4% (13-month low). In comparison, readings ranged between 2.8% and 3.2% in 2024 and were below 2.8% throughout 2019 and early 2020.

- That upward drift in long-run inflation expectations will be a concern for the inflation hawks at the Fed. That anxiety will only be amplified by the war impact as sharply higher oil prices recall the ‘70’s period of unanchored, spiraling inflation expectations. While this episode shouldn’t be a full repeat of that experience, the slight drift higher in expectations into what should be another dose of coming cost pressure will not sit well with the inflation-focused contingent. Thus, next week’s FOMC meeting will give them centerstage to express those concerns.

Overall and Core PCE Inflation at 2.8% and 3.1% YoY, Respectively

Largest Spending Gains in Essential Services vs. Discretionary Items

Job Openings Expected to Tick Higher for January Source: BLS

Source: BLS

JOLTS Quits and Layoff Rates – Expected to Hold Steady

Univ. of Michigan Inflation Expectations – Forecasted to Tick Higher for March Source: Univ. of Michigan

Source: Univ. of Michigan

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.