Jobs Report Headlines New April Data This Week

- This week brings the first substantial batch of April data after being teased on Friday with ISM Manufacturing. That report will be followed by the Services Survey due tomorrow, and of course the big report is the jobs numbers due on Friday. Expectations there are for 60 thousand new jobs and a stable unemployment rate of 4.3%. Of course, Middle East events have the potential to steal the headlines and the weekend news that the US will allow/protect ships from non-combatant states to leave the Strait has increased oil prices as it’s interpreted to mean the blockade will remain indefinitely, with all that that means regarding the restriction on oil flows. Currently, the 10yr is yielding 4.40% up 3bps on the day, while the 2yr is yielding 3.92% also up 3bps on the day, and the highest yield since March 26th.

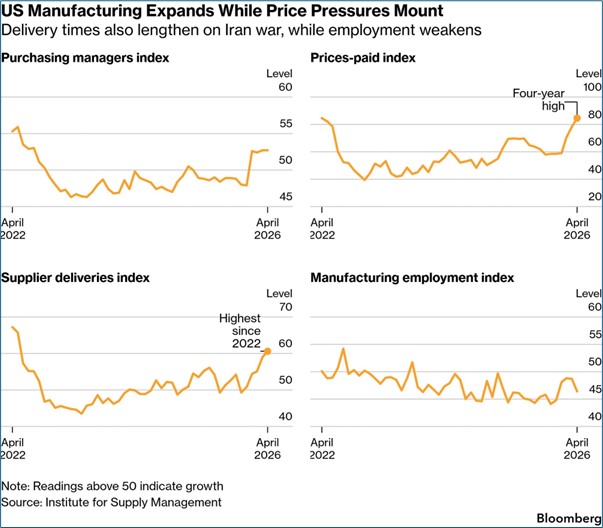

- The April ISM Manufacturing Index registered 52.7, unchanged from March but below the 53.2 expectation. The New Orders Index expanded for the fourth straight month, registering 54.1, up 0.6 percentage point compared to March’s figure of 53.5 but below the 54.7 expectation. The Prices Paid Index remained in ‘increasing’ territory registering 84.6, a 6.3-percentage point jump from March’s reading of 78.3 and easily above the 80.0 expectation. In the last three months, the Prices Paid Index has increased 25.6 percentage points to reach its highest level since April 2022. The Employment Index registered a disappointing 46.4, down 2.3 percentage points from March’s figure of 48.7. To summarize, an unchanged but expansionary headline reading boosted by new orders, but the prices paid index continues to reach new highs and employment continues to sag. To be sure, not a great picture in the manufacturing sector.

- In the commentary section, the second month of the Iran war, 31% of the comments were positive and 69% negative, with a positive to negative sentiment ratio of 1 to 2.2. Among comments, the war was mentioned in 47% and tariffs in 18%. As was the case last month, some panelists referenced both topics within a single comment or in mixed sentiment. So, it seems the war is dominating sentiment and commentary, but the tariff issue remains topical as well. This comment was typical of the report, “Demand for manufactured goods is trending higher versus last year; however, geopolitical uncertainty and rising oil and diesel prices continue to weigh on demand. Many customers are exercising caution and remain in a wait-and-watch mode.” Much like the S&P Global PMI series, the expansionary print was more due to precautionary purchases and inventory build before expected further price hikes and/or supply shortages. It doesn’t really represent a clear boost in orders driven by increased demand.

- Tomorrow, the ISM Services Index will be released with expectations for the headline reading to tick lower from 54.0 to 53.7. That would represent still solid expansion in the largest sector of the economy. Much like the manufacturing sector, the Prices Paid Index will get inflation scrutiny with the index expected to increase from 70.7 to 73.0. New Orders are expected to slow from 60.6 to 58.0 while the Employment Index is expected to improve to 50.0, right on the expansion/contraction dividing line from 45.2 March. The expectation overall is for continued expansion, albeit a tad slower, but with positive movement in employment but also facing increasing costs which is a familiar refrain at the moment.

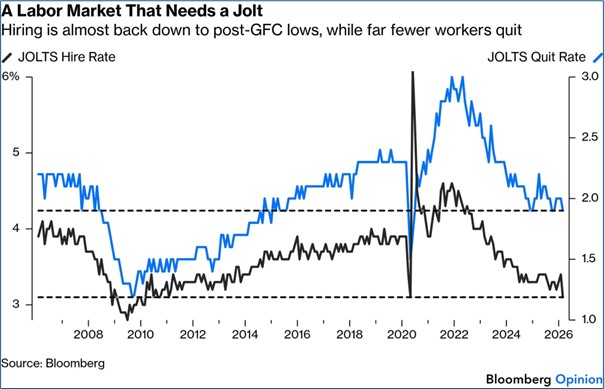

- Also tomorrow, the Job Opening and Labor Turnover Survey (JOLTS) for March will be released with job openings expected at 6.70 million vs. 6.88 million the prior month. As usual, the Quits Rate and Layoff Rates will be viewed for any break from their recent trends which have not signaled any new stress in the labor market. That’s been the case in most labor-related indicators as analysts look to see if the war impact and price hikes are starting to bite into the employment picture.

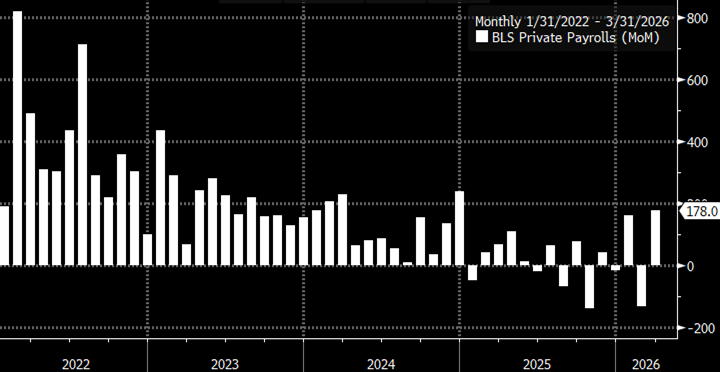

- The big report of the week will, of course, be the April Nonfarm Payrolls Report due on Friday. Expectations are for 60 thousand new jobs and 80 thousand in the private sector (meaning government jobs are expected to have fallen by 20 thousand). The unemployment rate is expected to remain unchanged at 4.3% with hours worked also stable at 34.2 hours. Average Hourly Earnings are expected to improve from 0.2% MoM to 0.3% with the YoY rate improving from 3.5% to 3.8%. The Labor Force Participation Rate is expected to improve slightly from 61.9 to 62.0.

- On net, employment expectations are for a decent to solid month in the labor market with increased hiring, increased labor participation (albeit slight), and increased wage gains. If that comes to pass it will put the Fed squarely in the pause camp as they wait on inflation data that is likely to get worse before it gets better. Still, with Kevin Warsh coming in as Trump’s hand selected new Fed Chair, any thoughts of rate cuts anytime soon seem a tall if not impossible order. On the other hand, the restive inflation hawks on the FOMC (remember those three dissents last week) will most likely push for a statement that mentions risks to policy are balanced with an equal possibility that the next move will be a rate hike just as much as it could be a rate cut. That’s not exactly what President Trump will want to see or hear, but that could be the case.

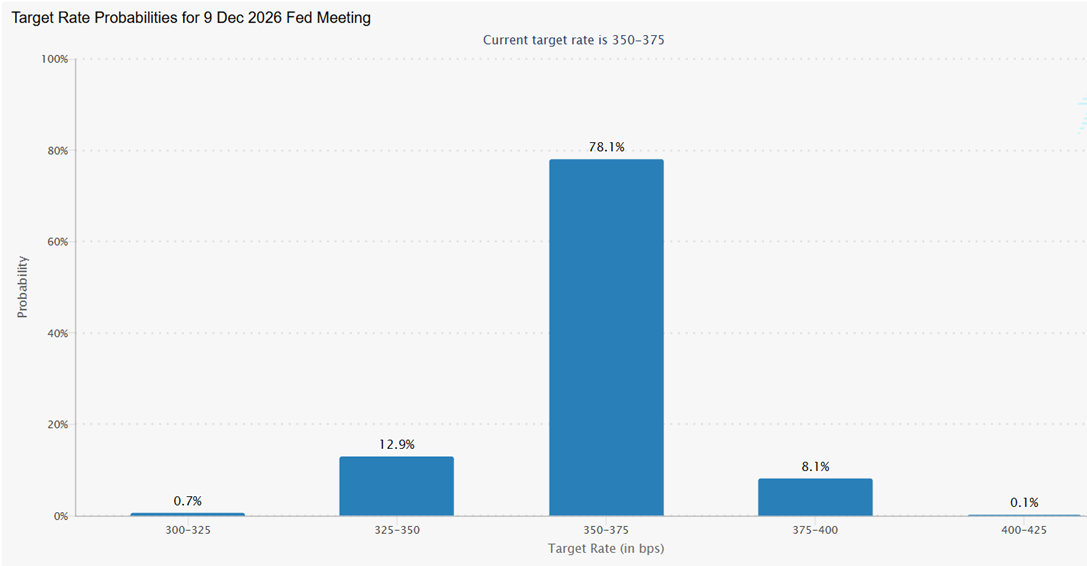

Fed Funds Futures Continue to Point to No Rate Cuts This Year

Source: CME Group

ISM Manufacturing – Prices Paid Index Moves into 2022 Territory

March Job Opening and Labor Turnover Survey (JOLTS) Due Tomorrow

April Jobs Report Due Friday – Expectation is for 60k New Jobs Source: US BLS

Source: US BLS

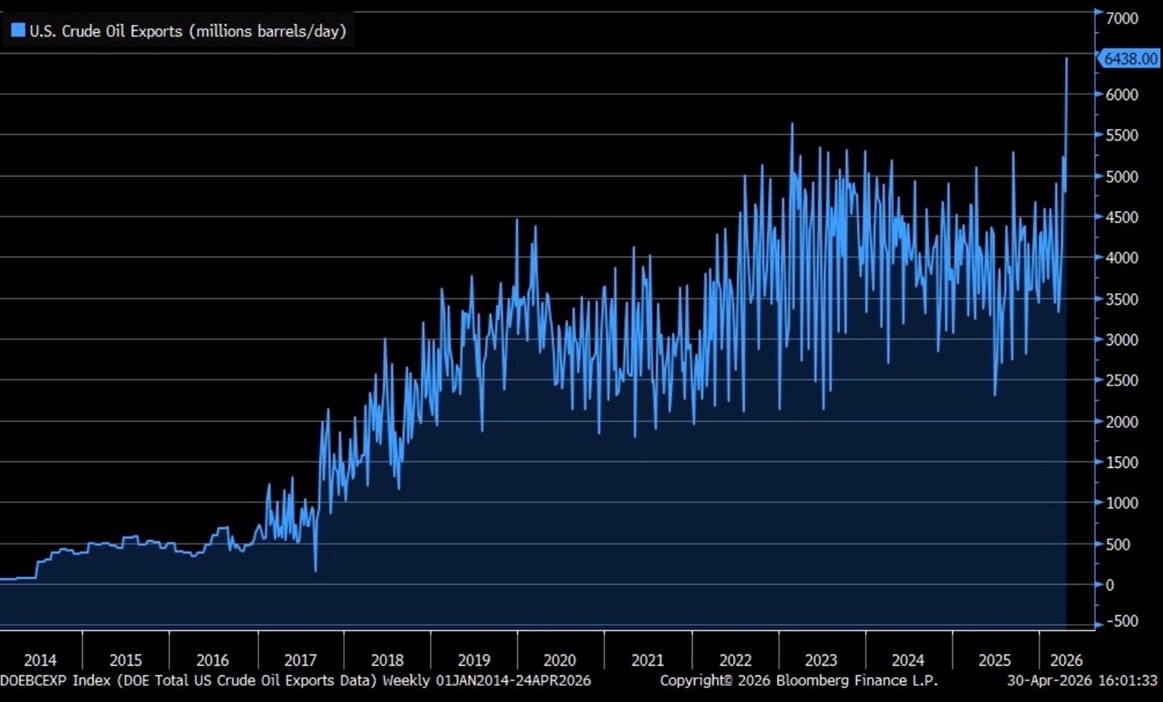

US Oil Companies Selling to the Highest Bidder

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.