Jobs Week Arrives

- We enter what should be a busy week of labor market data, but the government is in a partial shutdown. Sound familiar? Well, the good news is this shutdown shouldn’t last a month. The House will vote tomorrow on funding bills, and a 2-week extension of DHS funding, that the Senate approved late last week. If the House passes the legislation the shutdown will end and reports should flow this week without delay. Once again, we’re at the mercy of DC political machinations. Currently, the 10yr is yielding 4.24%, flat on the day, while the 2yr is yielding 3.54%, up 1bp on the day.

- Some of the Warsh trade is already upon us. The metals complex, led by gold and silver, were in the midst of an historic rally and with the Warsh news, that has come to a screeching halt. While Trump may want a central bank that is predisposed to lowering rates, Warsh is seen as more an inflation hawk from his previous stint at the Fed and has been quite vocal in wanting to shrink the balance sheet even more than what the Fed has been doing. That too is weighing on markets, particularly longer duration bonds that have been part of quantitative easing campaigns in the past, with the goal of lowering longer term (read mortgage) rates to spur economic growth. It’s early days yet, and Warsh won’t take the Fed helm until June, but we are seeing signs of the market repositioning with what they already know.

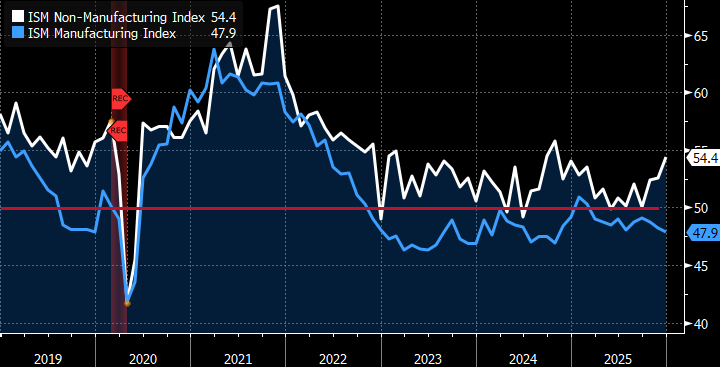

- The first week of the month always ships a flotilla of reports and this week is no different, assuming the government remains open and operating. First on the list is the ISM Manufacturing Survey at 10am ET with the headline reading expected to tick slightly higher from 47.9 to 48.3. That would keep the sector under the 50 dividing line between expansion and contraction and continue the manufacturing malaise despite nearly a full year into the Trump tariff regime. Other elements in the report like Prices Paid, New Orders, and Employment will also garner attention.

- Tomorrow brings the first labor market report with the Job Opening and Labor Turnover Survey for December. Expectations are for job openings to dip slightly from 7.146 million. The long-term trend has been for job openings to trend lower from the peak of 12 million openings back in 2022. It’s all part of the moderation in labor market momentum, but as long as the unemployment rate remains in the low 4% range, the Fed doesn’t seem overly concerned. The Quits Rate and Layoff Rate will be of interest too as both have been signaling a loss of momentum as well but nothing dramatic. We’ll see if that holds again for December.

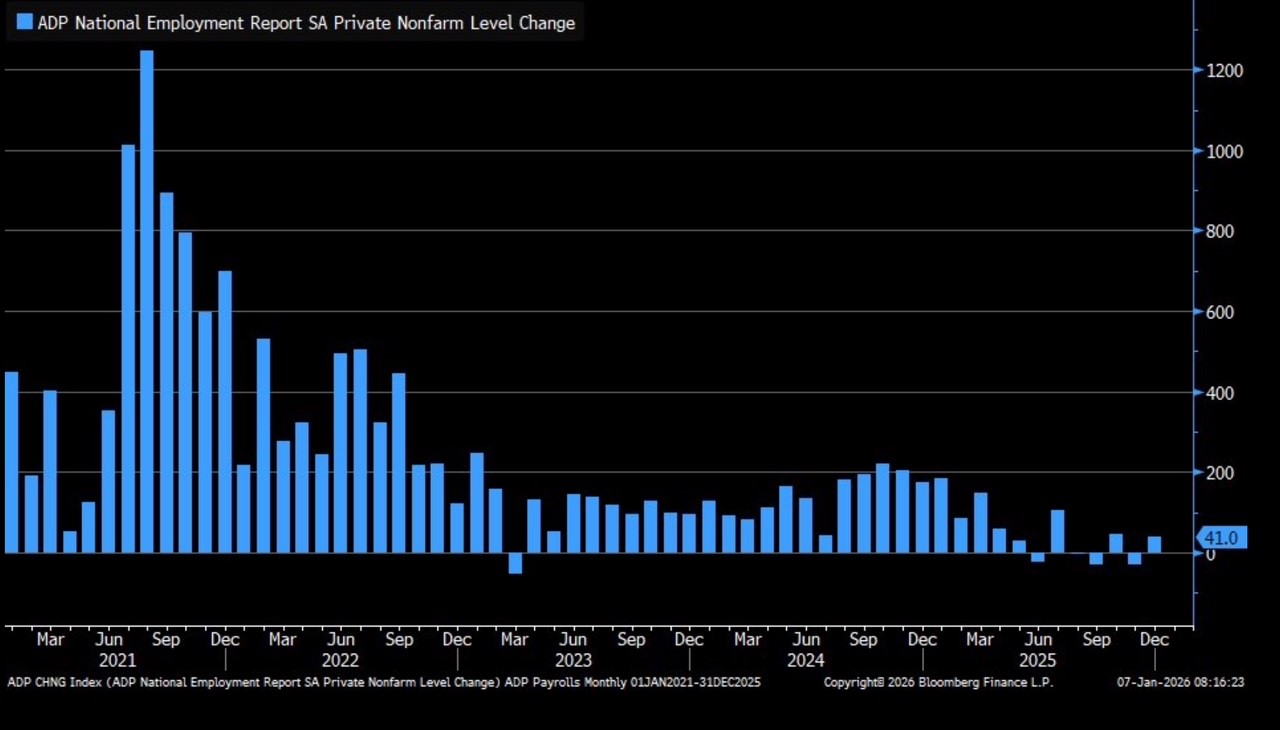

- Wednesday brings a pair of interesting labor market reads. First, ADP will publish its January Employment Change report with 45 thousand private sector jobs expected vs. 41 thousand in December. Later tomorrow morning, the ISM Services Index will be released with a slight dip expected from 53.8 to 53.3. That would still be in expansion territory but with some loss of momentum, nonetheless. Like the ISM Manufacturing release, the readings on Prices Paid, New Orders, and Employment will round out the picture of the dominant service side of the economy.

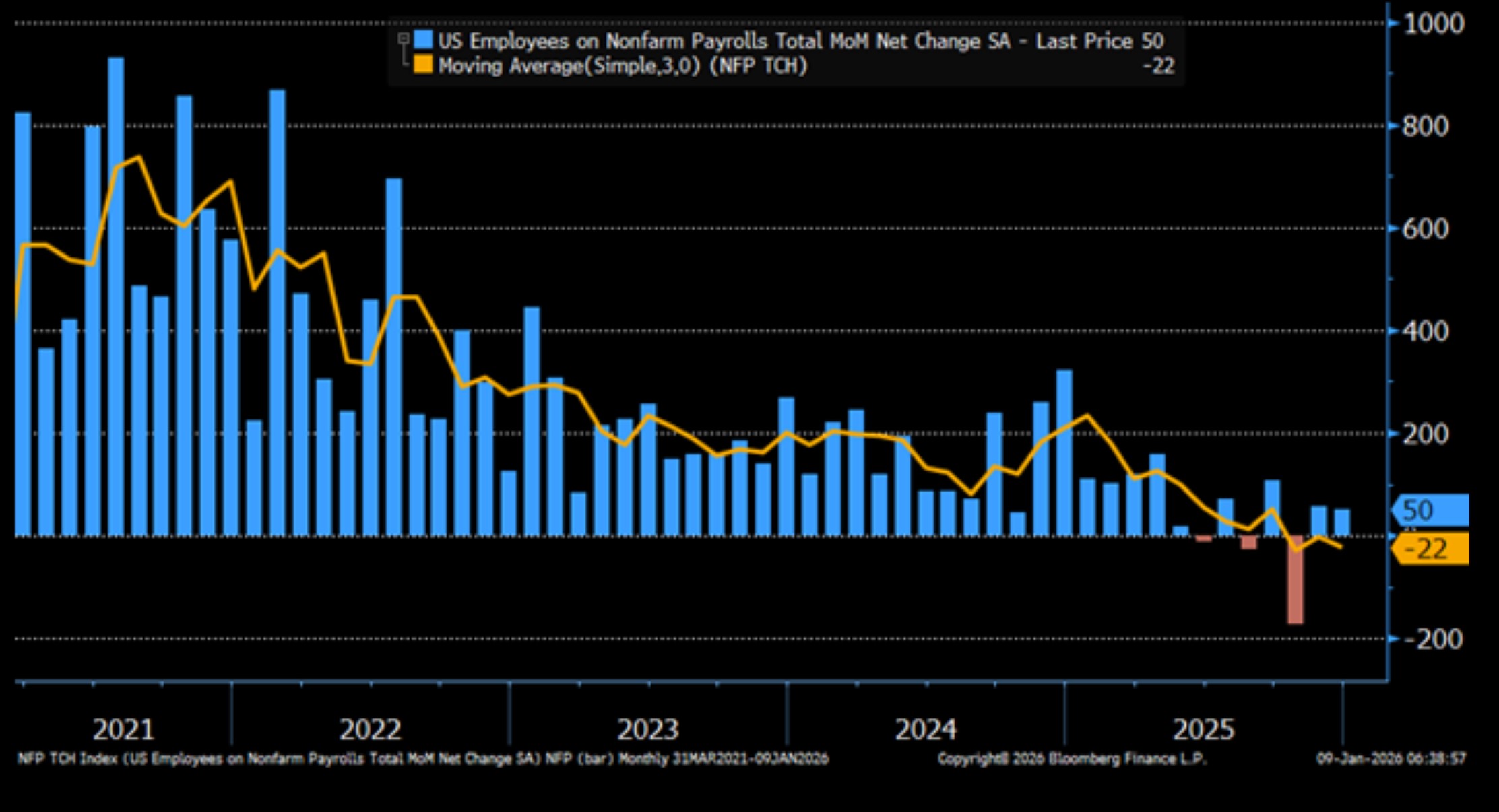

- Finally, the January employment report will be released on Friday. Expectations are for payrolls to increase by 70 thousand vs. 50 thousand in December. Private payrolls are expected to increase 73 thousand vs 37 thousand in December. Of course, downward revisions have been a feature of this report in the post-Covid environment, so we’ll watch for those in this update. The unemployment rate is expected to be unchanged at 4.4%, and that’s important to the Fed that seems a stable unemployment rate represents a stable labor market despite the slowing in new jobs to a near standstill.

- Average hourly earnings are also expected to be unchanged at 0.3%MoM with yearly gains stable at 3.8%. With the slowdown in immigration, the latest estimates of breakeven job growth are in the 25 to 50 thousand range, so job growth hitting the expected pace will keep the Fed fixated on inflation trending closer to the 2% target before entertaining another rate cut.

ISM Surveys Await Investors This Week – No Major Change is Expected Source: Institute of Supply Management

Source: Institute of Supply Management

ADP Employment Change for January Expected Similar to December Level Source: ADP

Source: ADP

BLS Nonfarm Payrolls for January Growth Expected to Improve on Dec.’s Modest Pace Source: BLS

Source: BLS

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.