Low-Hire, Low-Fire Economy Continues

- This week was dominated by geo-political events, culminating in the President’s address at the annual Davos World Economic Forum. While the issue of Greenland sovereignty was front and center Trump relented on his earlier demand for the island and that allowed some space for improved trading, both equities and fixed income. However, while yields are off the highs for the week they remain above the 4.10% – 4.20% range that prevailed prior to this week’s events. Next week will be dominated by the Wednesday FOMC rate decision with a pause in rate cuts widely expected. Currently, the 10yr is yielding 4.24%, down 1bp, while the 2yr is yielding 3.61%, unchanged on the day.

- While the week was mostly about geo-political events, we finally received the Fed’s preferred inflation measure for both October and November in the form of the Personal Income and Spending reports. On the inflation front, overall PCE increased 0.2% MoM in both October and November. Excluding food and energy, core PCE also increased 0.2% in both months. Year-over-year, PCE increased 2.7% in October, followed by an increase of 2.8% in November. Core PCE increased 2.7% followed by an increase of 2.8% in November.

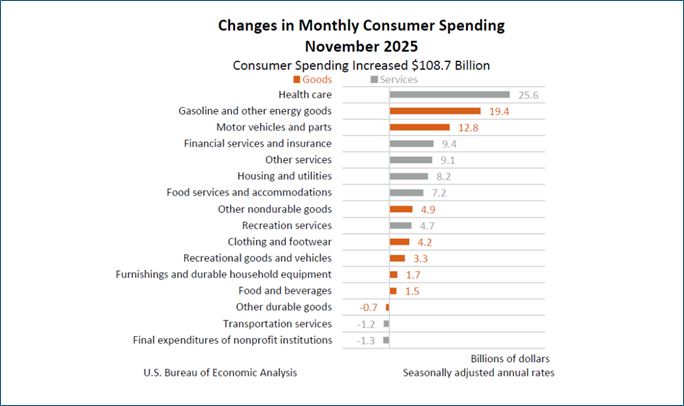

- Personal incomes increased 0.1% in October, followed by an increase of $80.0 billion, or 0.3% in November. Meanwhile, on the spending side, personal consumption expenditures (PCE) increased $98.6 billion or 0.5% in October. This was followed by an increase of $108.7 billion or 0.5% in November. The increase in spending was led by health care, financial services and insurance, and other services. Good side spending was led by gasoline and other energy goods as well as motor vehicles and parts (see spending table below).

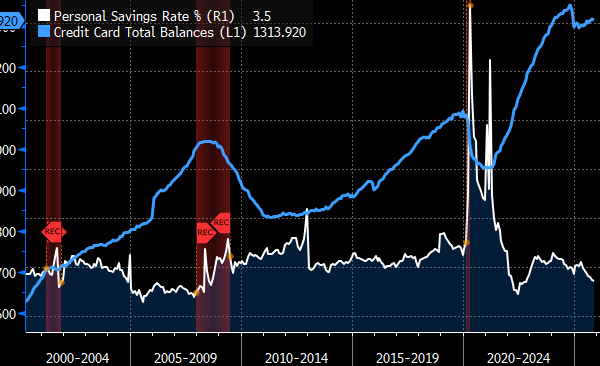

- The personal saving rate—personal saving as a percentage of disposable personal income—was 3.7% in October followed by 3.5% in November. The savings rate is at a three-year low while credit card balances continue to grow as a funding source (see graph below). Those who have been predicting the demise of the US consumer have pointed to the declining savings rate as a harbinger of slower consumption ahead, but the US consumer has found ways to continue funding their spending habits. The question is with wage gains moderating and job growth slowing, how long can debt financing keep the spending gains going?

- While the Fed can take comfort in the mostly benign inflation readings for October and November, the core measure is expected to increase by 0.4% for December, bringing the YoY rate up to 3.0%. That argues for patience at next week’s FOMC meeting. The Bureau of Economic Analysis has yet to reveal when the December data will be released. Typically, it’s at the end of the following month but that will likely slip into February given the delay with October and November, just another reason to expect a pause at next week’s meeting.

- In the week ending January 17, weekly initial jobless claims were 200,000, an increase of 1,000 from the previous week’s revised level. The 4-week moving average was 201,500, a decrease of 3,750 from the previous week’s average. This is the lowest average since January 13, 2024. For the week ending January 10, continuing jobless claims totaled 1,849,000, a decrease of 26,000 from the previous week’s downwardly revised level. The 4-week moving average was 1,870,750, a decrease of 16,250 from the previous week. This week’s data coincides with the survey period for the January employment report, so it has a bit more importance, yet it still reflects a labor market stuck in the low-hire, low-fire environment that has become a feature of this economy.

- On Wednesday, the Supreme Court heard the Fed Governor Lisa Cook termination case and given the justices questions and comments it seems likely they will rule against President Trump. Most of the concern centered on endangering Fed independence and whether an incorrect mortgage application filing rises to the necessary “for cause” termination standard. It’s not known when the Court will issue its ruling and, of course, we’re also waiting on the IEEPA Tariff ruling. If anything, this shows that the Court will not be hurried when they don’t want to be hurried!

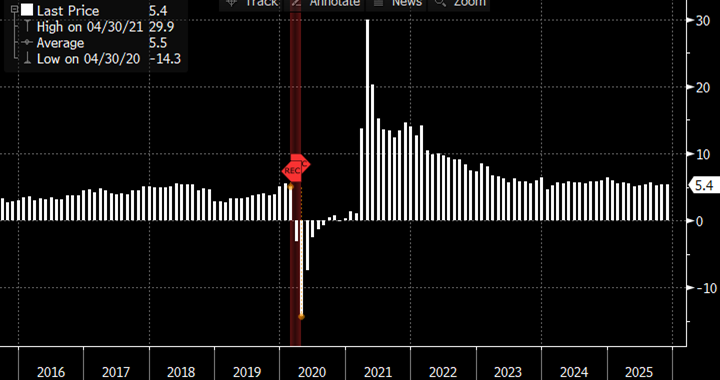

Annual Personal Consumption Has Been Steady and Strong (Personal Spending YoY)

Source: BEA

But Spending Gains Focused on Essentials and Less on Discretionary Items

But Savings Rate Decreases While Credit Card Balances Increase

Source: BEA & Bloomberg

Weekly Jobless Claims Reveal the Low-Hire, Low-Fire Economy Continues

Source: Dept. of Labor

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.