March Jobs Report Beats but Concerns Persist

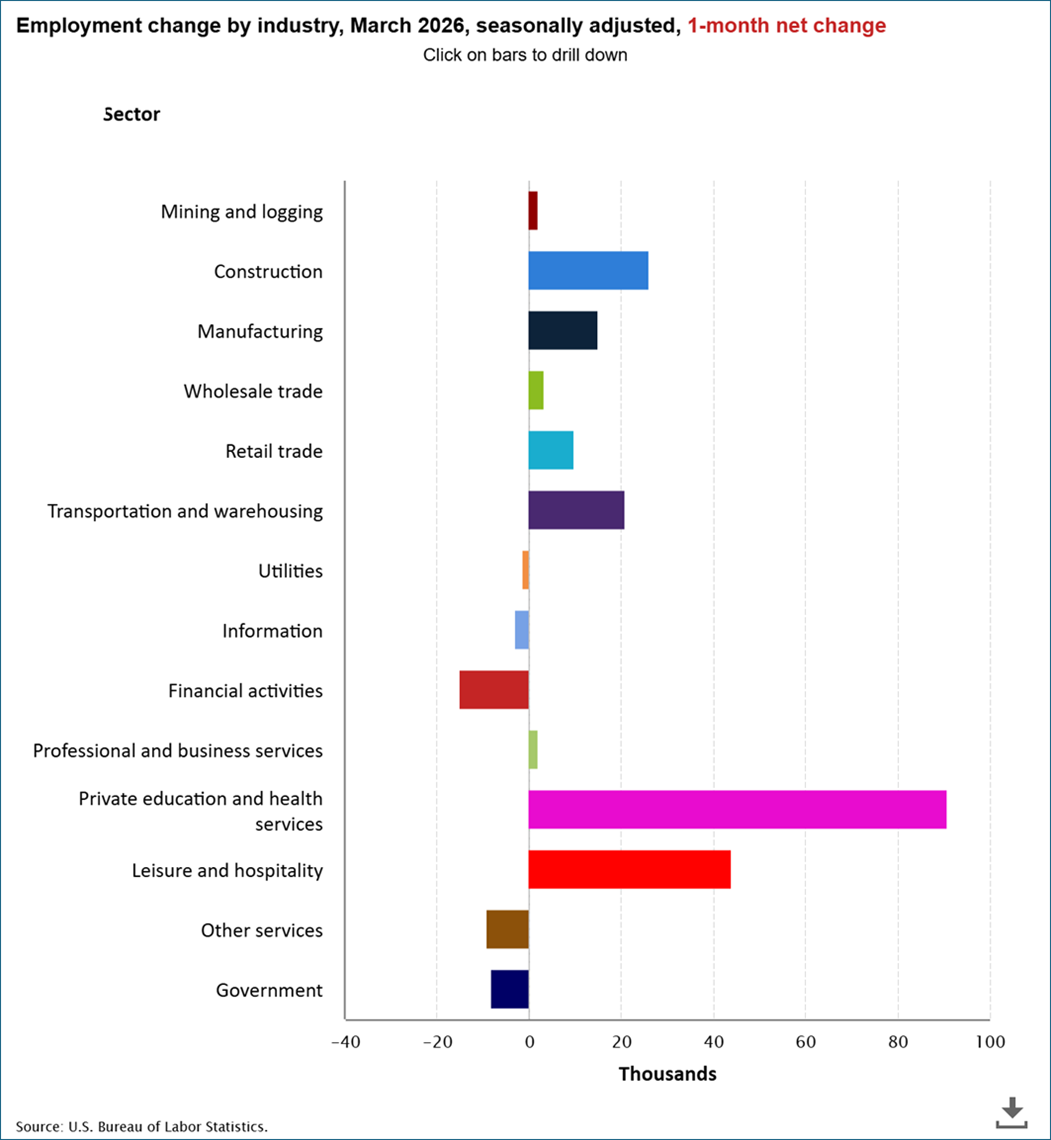

- March nonfarm payrolls rose 178 thousand, easily beating the 65 thousand expected and 133 thousand lost in February (revised lower from an initial -92 thousand). Two-month revisions cut 7 thousand jobs from previous estimates with January revised up 34 thousand and February 41 thousand lower. February was marked by weather issues along with a healthcare worker strike in California which slowed job growth in the strongest sector over the past year. As if on cue, the March bounce was keyed on strong healthcare (+76k) but leisure/hospitality (+44k) provided surprising strength too. The federal government continued to shed jobs with 18k lost during the month.

- The Household Survey, which is smaller than the Establishment Survey and thus subject to more volatility, generates the unemployment rate, labor force participation rate, etc.. The survey reported a decrease of 396 thousand people in the labor force (those employed and those not working but actively looking for employment) and a 332 thousand decrease in unemployed persons. You can read that as nearly 400 thousand people left the workforce with most of those unemployed but now electing out of the labor market. So, the unemployment rate ticked a tenth lower to 4.3% (4.26% unrounded vs. 4.44% in February), but I wouldn’t call that a “good” move lower. The smaller labor force also led to a drop in the Labor Force Participation Rate from 62.0% to 61.9%, that’s the wrong direction for that metric.

- Many Fed officials have referenced the stability in the unemployment rate as evidence of overall labor market stability, so a decrease in the rate, on the surface, conforms with that stability picture. That said, a shrinking labor force that signals many formerly unemployed have simply given up is not the type of stability I think the Fed is looking for, and that’s probably the key takeaway from today’s report.

- Another concerning point, Average Hourly Earnings rose 0.2% MoM, the lowest this year and missing the 0.3% expectation and trailing the 0.4% February gain. With the earnings downtick, the year-over-year pace dipped three-tenths to 3.5%, missing the pre-release 3.7% expectation. In addition, average weekly hours fell a tenth to 34.2 hours. Bottom line, with YoY wage gains now in the mid-3% area, wage-price inflation won’t be a Fed worry but the slippage in both the hours worked and monthly wage gain speaks to a slightly thinner wallet for the consumer.

- In summary, today’s release eased some fears from the miss in February and matches some of the other employment-focused reports received this week (ADP, JOLTS, ISM, Jobless Claims) that painted a picture of employment momentum holding somewhat steady and importantly not indicating an imminent leg lower. The healthcare sector returned as the leading job gainer and the buildout of AI data centers rebounded from weather-related slowing in February as construction jobs saw an 26k increase.

- Bottom line: with a Good Friday release this report was greeted by a smaller-than-usual audience, and the fact that with a stable unemployment rate and headline gain, the Fed remain patient and wait for inflation to improve. The latest oil price spike and the ongoing supply constraints through the Strait of Hormuz, that still has an uncertain duration, will dominate the factors in trading next week. April is expected to see physical shortages manifest from the shipping blockage, first in east Asia then spreading west during the month. Thus, the inflation/growth questions will continue dominating trading this month with 2H26 policy expectations being driven by that dynamic and not today’s jobs report.

- Next week’s highlights will be the February Personal Income and Spending Report on Thursday and the March CPI release on Friday. Given the war began as February ended, the PCE inflation numbers will be discounted as stale but the spending numbers will get some attention, and the expectation is they will confirm the strength as reported this week in the Retail Sales Series. Again, though, this is February numbers so even a decent read will be treated with kid gloves.

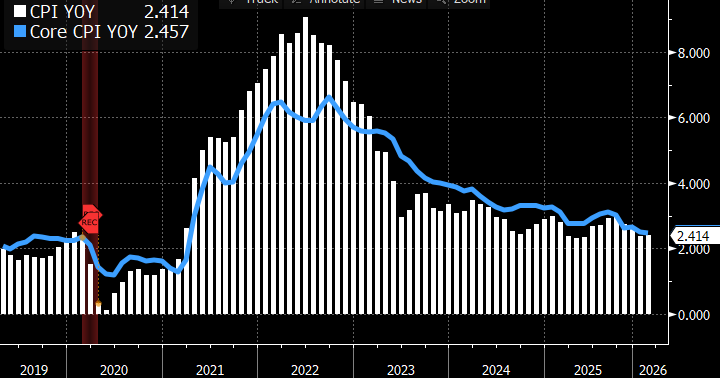

- The bigger report will be Friday’s March CPI where headline inflation is expected spike from 0.3%MoM to 0.9% with the YoY rate jumping from 2.4% to 3.4%. That would be the highest overall CPI rate since April 2024. Core CPI is expected to increase a more modest 0.3% from 0.2% and the YoY rate is expected to increase from 2.5% to 2.7%. The Fed wants to “look through” the energy complex spike, but the longer the war and the shortages/blockages persist the harder that becomes, especially with memories of transitory price spikes post-pandemic still fresh in the minds of consumers and Fed officials.

- While not on par with the CPI release, the University of Michigan will be back again on Friday with its first look at April sentiment. The survey period encompasses the entirety of the war vs. last month when the survey period was split between pre-war and war. It won’t be surprising to see sentiment continue to move lower and approach the 2022 and 2025 lows. Also, the longer-term inflation expectations that ticked a tenth lower to 3.2% last month are expected to move higher, given the early price moves in gas, etc.. The Fed likes to see these long-run expectations “well anchored” but how high they drift will be a key item for the Fed.

- Housekeeping Note: I’ll be off next week for spring break. The next edition of the Market Update will be Monday, April 13th. Please keep things in order while I’m gone! See you then.

Healthcare Continues to Dominate New Hires

Annual Average Earnings Dips from 3.8% to 3.5% – Lowest Since 2021

March CPI and Core CPI will be the Key Release Next Week (Friday) Source: BLS

Source: BLS

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.