March Retail Sales Headlines a Light Data Week

- While this week is a rather dull one for economic news it highlights that trading will once again be dominated by war news, and the latest there is the US firing on and seizing of an Iranian cargo ship headed towards Iran. With US officials traveling to Islamabad, Pakistan for another round of talks, the original ceasefire agreement ends tomorrow with the outcome very much up in the air. The twists and turns of the Middle East conflict, however, has the market trading in less extremes. For example, oil is up $4/bbl on weekend events but at $88/bbl that’s well under the $100/bbl we saw earlier in the conflict. This week will also feature Senate confirmation hearings for Fed Chair Nominee Kevin Warsh. What’s unknown is whether Senator Tom Tillis from NC will allow a vote due to the pending DOJ litigation regarding the Federal Reserve’s renovation project. He’s previously threatened to hold up the vote until the litigation is dropped. So, some non-Middle East drama is possible. As they say, never a dull moment. Currently, the 10yr is yielding 4.26% up 1bps on the day, while the 2yr is yielding 3.73% up 3bps on the day.

- As mentioned above, it’s another quiet week as far as new data goes but the headline will be the March Retail Sales Report due tomorrow. Expectations are that topline sales will increase 1.2% vs. 0.6% in February. We’ll remind everyone that this report is not inflation adjusted so keep that in mind given the surge in gas prices that occurred during the month. Sales ex-auto are expected to increase 1.3% vs. 0.5%. That solid number implies it’s not auto sales that drove the expected uptick from the prior month, so maybe it’s those surging gas prices?

- Well, sales ex-autos and gas are expected to be up just 0.2% vs. 0.4% in February, so indeed it does seem any headline surge will be mostly a gas price story. Finally, the GDP included Control Group (which is net autos, gas, building materials and few other miscellaneous items) is expected to increase a modest 0.2% vs. 0.5% in February. Think of the Control Group as “core” spending and the expected downtick is probably the takeaway from the report, if expectations are met.

- Much has been said about the K-shaped economy and the well-to-do consumer continuing to spend with gusto, aided by the wealth effect of record stock market gains. The Retail Sales Report is more goods-based rather than services and those well-heeled consumers, while certainly buying “stuff”, are also keen on travel experiences, food, drink, and entertainment and those aren’t picked up in this report as much as they are in the more comprehensive Personal Income and Spending Report due April 30th. This is a long-winded way of saying don’t write-off the consumer if the Retail Sales Report disappoints, that judgment will have to wait until that second more comprehensive report is released.

- The Fed’s latest Beige Book of Economic Conditions was released last week and words like slight to modest growth were used to characterize economic activity. Uncertainty was mentioned often in regard to the Middle East conflict with many contacts reporting a “wait-and-see” posture. On balance, consumer spending increased slightly with higher-income consumers exhibiting more resilience while lower income groups were increasingly more cost conscious. Commercial real estate saw some positive trends with most of that involving AI-related data center projects. One interesting but perhaps foreboding note was agriculture contacts reported higher crop prices were helping to offset higher fertilizer and fuel costs. Expect those higher costs to appear in the produce section of your grocery store soon if they haven’t already.

- Another report of note is due Thursday with the S&P Global Preliminary PMI series for April. Recall that in March the manufacturing PMI was in solid expansion mode at 52.3 while the services sector contracted slightly to 49.8 resulting in the Composite PMI at a near standstill of 50.3. These will be the first of the PMI numbers for April so it will garner some interest, assuming war headlines don’t push these reports to the sidelines.

- Finally, the final University of Michigan April Sentiment Survey will be released on Friday. Recall, the preliminary report saw all measures of sentiment dipping to lows last approached in Covid times. Overall sentiment registered a 47.6 reading with Current Conditions at 50.1 and Expectations at 46.1. Inflation expectations over the next year were 4.8% with longer-term (5-10yrs) inflation expectations were a more moderate 3.4%.

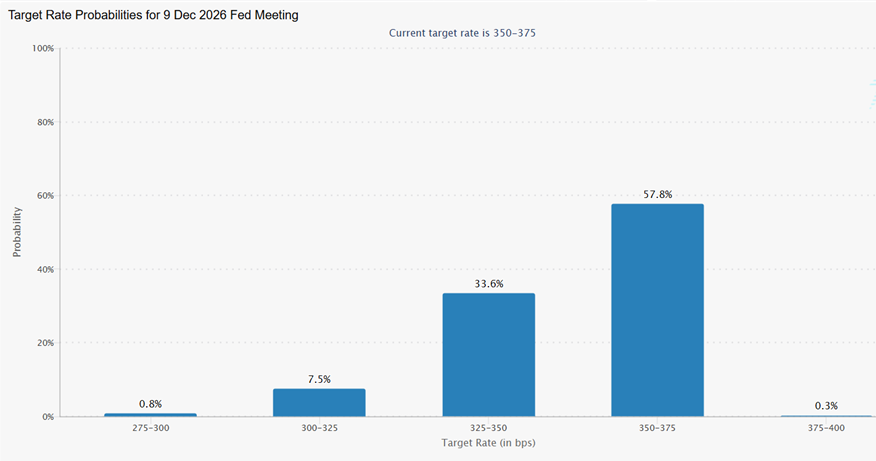

Futures Market Favors No Rate Cut This Year

Source: CME Group

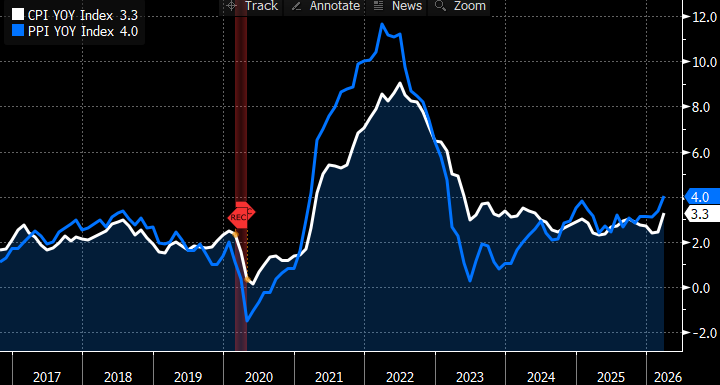

PPI Used to Lead CPI Lower, Now it’s Leading it Higher

Source: BLS

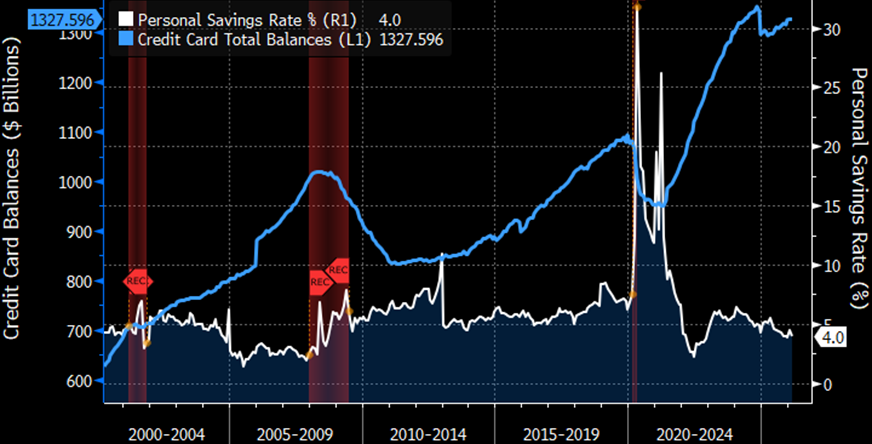

While the Wealth Effect is Boosting the Upper Income Group, the Rest are Relying on Credit Cards Source: Bloomberg

Source: Bloomberg

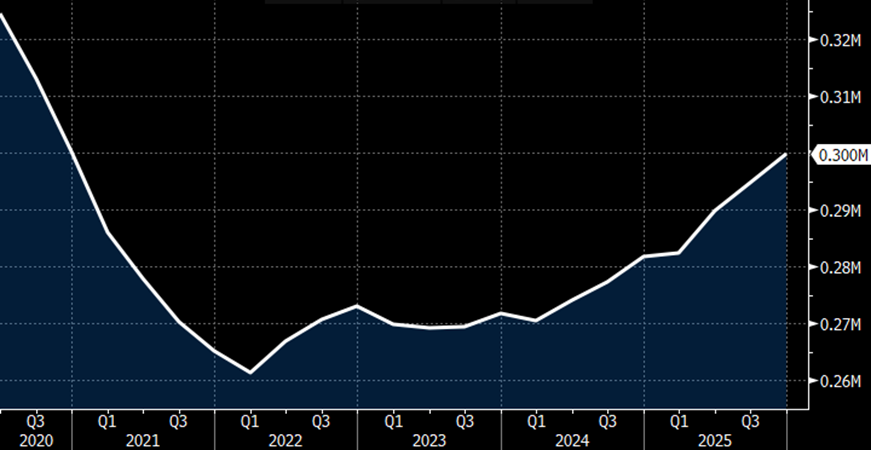

Tapping Home Equity Loans is Becoming a Thing Again Source: FDIC

Source: FDIC

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.