March Retail Sales Show Surprising Strength

- Tuesday was probably peak info day for the week with a Fed confirmation hearing competing with a round of plentiful economic data, and, of course, Middle East news. On that front, Trump’s talk of an open-ended ceasefire has the temperature down, along with oil prices firmly below $100/bbl and that is providing a quiet open. Yesterday’s March retail sales were surprisingly solid, even after accounting for higher fuel prices, ADP reported another solid week of job gains, and the Warsh confirmation hearings allowed him another shot at Fed blaming, which he has perfected over the years, but Senator Thom Tillis continues to bottle up a confirmation vote anytime soon. Currently, the 10yr is yielding 4.27% down 2bps on the day, while the 2yr is yielding 3.76% also down 2bps on the day.

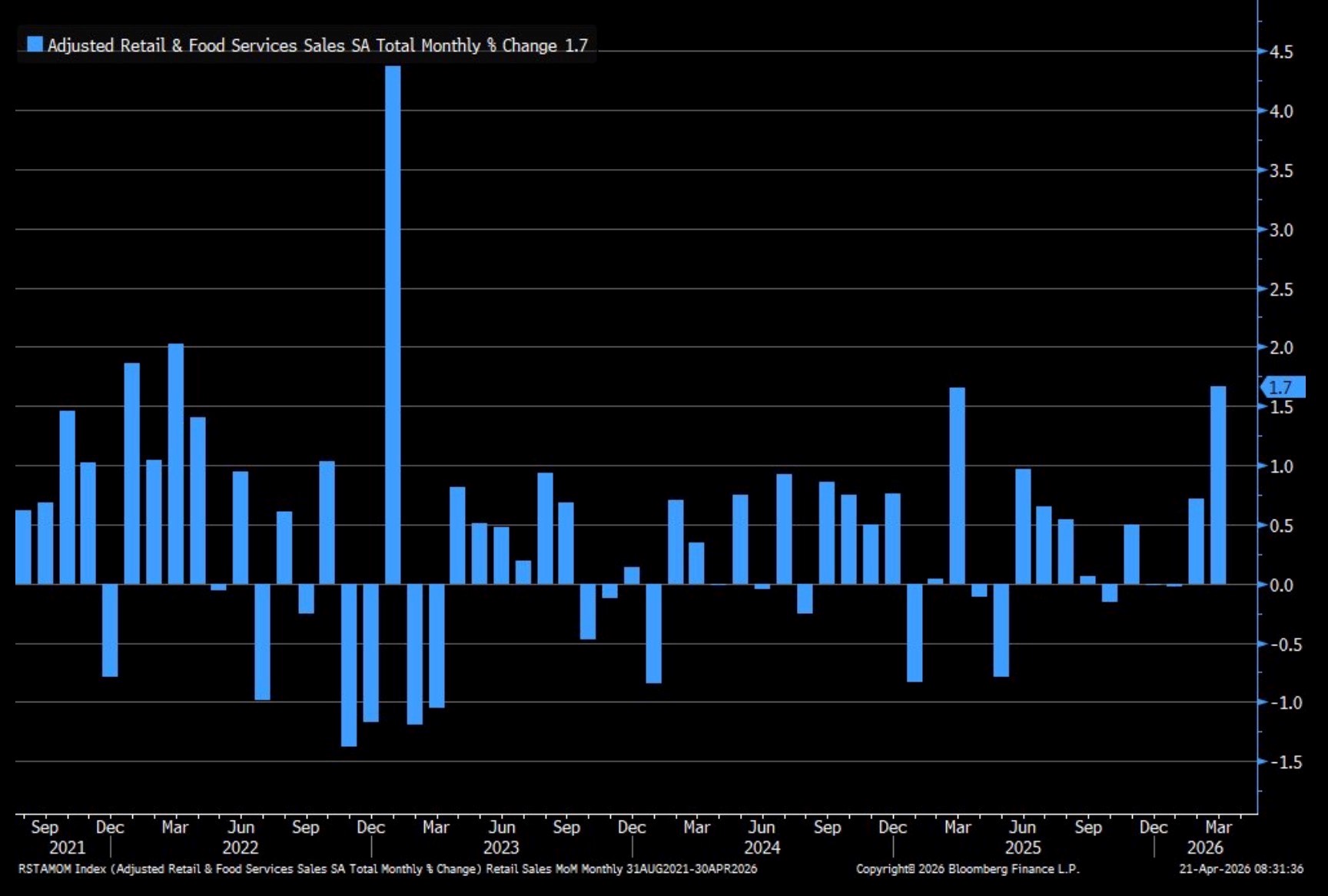

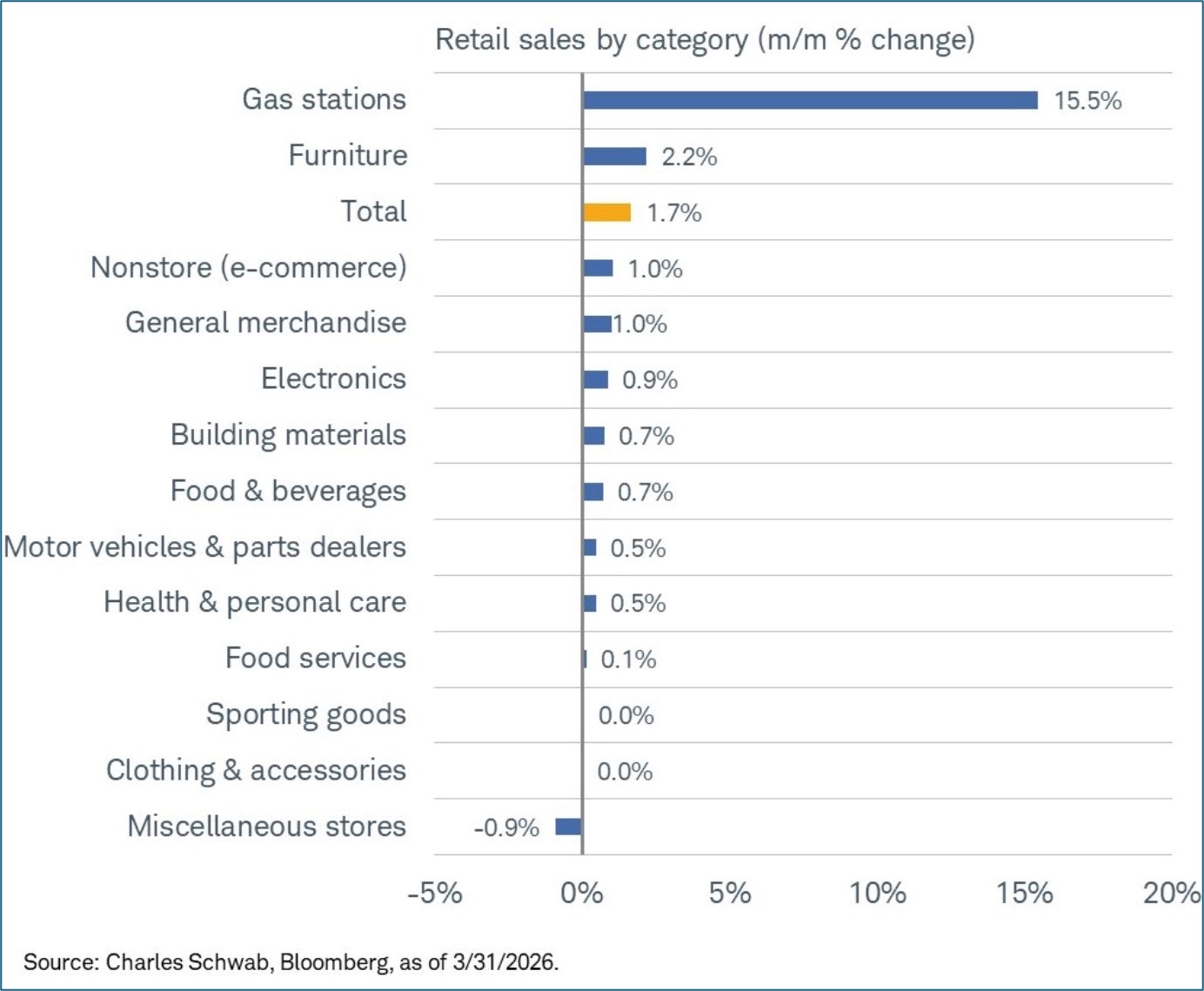

- As mentioned above, retail sales for March were better than expected, even after accounting for the surge in gas prices. Overall sales were up 1.7% MoM vs. 1.4% expected and 0.7% prior. Sales ex-autos and gas were up 0.6% vs. 0.2% expected and 0.6% the prior month. The Control Group – a direct GDP feed and considered “core” spending – rose 0.7% vs. 0.6% in February and 0.2% expected.

- So, a solid report across the board. Keep in mind it’s not inflation adjusted but for March the CPI saw little outside of the energy/fuel sector with real gains. It’s expected those will spread to other areas in the months ahead. But in summary, a solid showing by the consumer that will wait to be verified by the more comprehensive and inflation-adjusted Personal Income and Spending Report due on April 30th.

- We made note on Monday about the K-shaped economy and the well-to-do consumer continuing to spend with gusto, aided by the wealth effect of record stock market gains. The Retail Sales Report is more goods-based rather than services and those well-heeled consumers, while certainly buying “stuff”, are also keen on travel experiences, food, drink, and entertainment and those aren’t picked up in this report as much as they are in the more comprehensive Personal Income and Spending Report due April 30th. Thus, the impressive Retail Sales Report seems to indicate that the more comprehensive spending report due later this month should be a solid read as well. (See graph below).

- In the Kevin Warsh confirmation hearings, he started off where he usually does with criticism of the Fed’s past actions or inactions. He said today’s inflation is a residual of the Fed’s past mistakes, “The Fed missed its mark, and we are still dealing with the legacy of the policy errors in 2021 and 2022.Once you let inflation take hold in the economy, it’s more expensive and harder to bring it down. The fatal policy error…is still a legacy that we’re dealing with.”

- But Warsh softened his tone and said he is committed to ensuring that the conduct of monetary policy “remains strictly independent.” He also quickly added the Fed shouldn’t get the same deference on banking or international finance matters. Warsh framed the independence as something that is not threatened by politicians’ statements. Prediction markets put only a 33% chance that Warsh is confirmed by May 15, when Powell’s term ends (see graph below). The risk of delay comes from opposition by Senator Thom Tillis, who is blocking the nomination pending resolution of the litigation into Powell’s handling of the Fed building refurbishment. Tillis wants the matter dropped before proceeding to a vote.

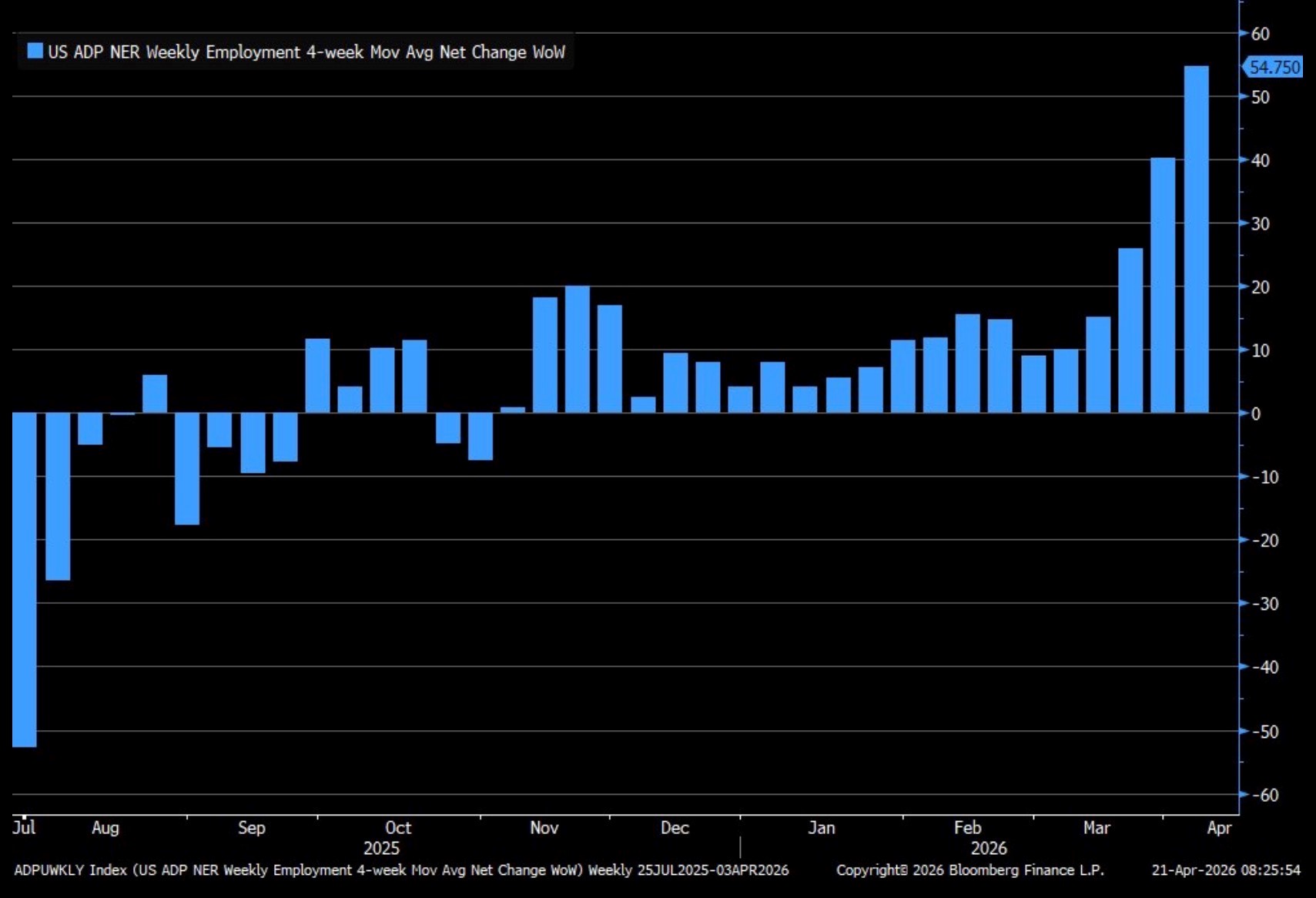

- The weekly ADP Pulse Report of hiring in April showed private payrolls added an average of 54,750 jobs per week for the four-weeks ending April 4. That’s the fifth consecutive week of hiring improvement and certainly not indicative of a labor market that is rolling over. That strength will allay Fed fears and with the stability in the unemployment rate, the Fed will have every reason to feel comfortable in its pause mode (see graph below).

March Retail Sales Post Solid Results and it’s not all from Higher Gas Prices

Predictable Jump in Gas Sales, but Every Category but One Showed Sales Growth

Warsh Confirmation Could Drag Into the Summer per Odds Markets Source: Kalshi

Source: Kalshi

ADP Weekly Job Report Shows Continuing Hiring Strength

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.