May Jobs Report Headlines Week Full of Data

- This week brings the first substantial batch of May data, mostly of the labor market variety. The big report is the jobs numbers due on Friday. Expectations there are for 95 thousand new jobs and a stable unemployment rate of 4.3%, the third straight month at that rate. Of course, Middle East events have the potential to steal headlines and influence rates, but the week will be chock full of first-tier reports starting with today’s ISM Manufacturing Index and continuing into Friday’s jobs report. The consensus view is that the labor market will display enough resilience to allow the Fed to remain in pause mode until lower inflation readings arrive. We’ll see if this week’s data conforms to that view. Currently, the 10yr is yielding 4.45% unchanged on the day, while the 2yr is yielding 4.02%, up 2bps on the day.

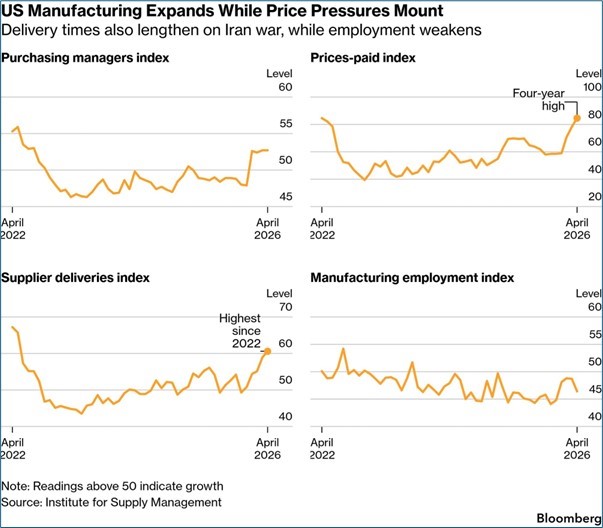

- The May ISM Manufacturing Index is due at 10am ET today with expectations of a 53.1 print vs. 52.7 in April. The New Orders Index, Prices Paid, and Employment indices will get plenty of attention too as investors try to determine both the price pressures still evident in May as well as the pace of ordering activity and hiring.

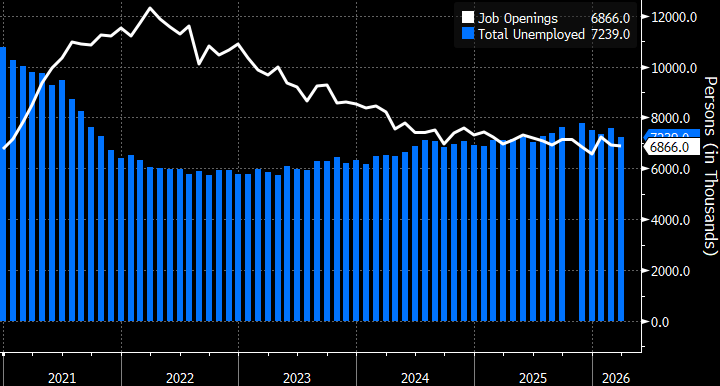

- Tomorrow, the attention shifts squarely to the labor market with the Job Opening and Labor Turnover Survey (JOLTS) for April with job openings expected at 6.80 million vs. 6.87 million the prior month. As usual, the Quits Rate (2.0%) and Layoff Rate (1.2%) will be viewed for any break from recent trends which have not, up until now, signaled rising stress in the labor market. That’s been the case in most labor-related indicators as analysts look to see if the war impact and inflation pressure are starting to bite into the employment picture. So far, it’s been a story of softer growth, but growth, nonetheless.

- On Wednesday, the ISM Services Index will be released with expectations for the headline expected to be unchanged from its April reading of 53.6. If expectations are met, it represents solid expansion in the largest segment of the economy. Much like the manufacturing sector, the Prices Paid Index will get inflation scrutiny with the index expected to increase from 70.7 to 71.0. New Orders are expected to be similar to April’s 53.5, while the Employment Index is expected to improve from 48.0 to 50.0, right on the expansion/contraction dividing line and continuing the improvement from March’s 45.2. Thus, between the manufacturing and services sectors, the expectation is for continued expansion, albeit a tad slower, but with positive movement in employment but ongoing price pressures will be a familiar refrain at the moment.

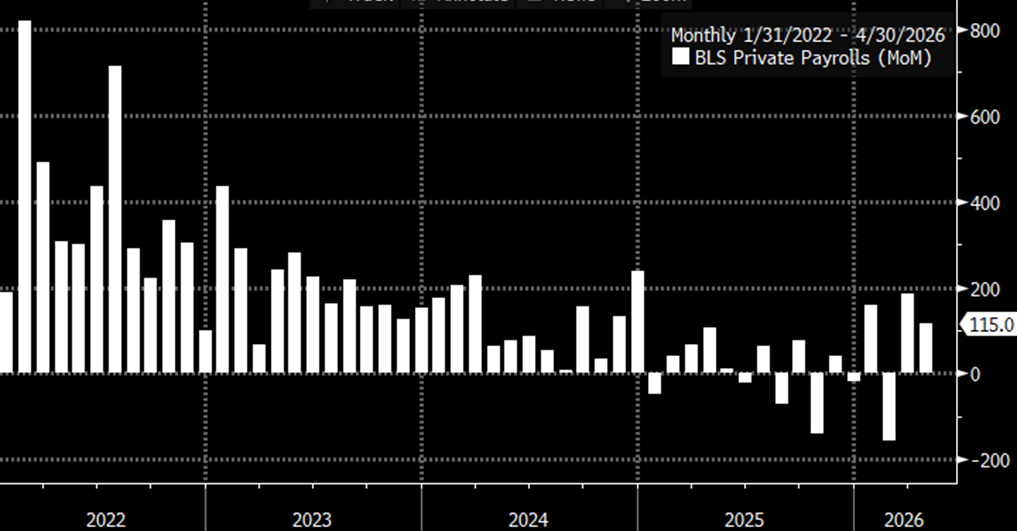

- The big report of the week will, of course, be the May Nonfarm Payrolls Report due on Friday. Expectations are for 95 thousand new jobs and 100 thousand in the private sector (meaning government jobs are expected to have fallen by 5 thousand). The unemployment rate is expected to remain unchanged at 4.3%, for the third straight month, with hours worked also stable at 34.3 hours. Average Hourly Earnings are expected to improve from 0.2% MoM to 0.3% with the YoY rate improving from 3.6% to 3.7%. The Labor Force Participation Rate is expected to remain unchanged at 61.8.

- On net, much like April, employment expectations are for a decent to solid month with increased hiring, and a slight increase in wage gains. If that comes to pass it will put the Fed squarely in the pause camp as they wait on inflation data that is likely to get worse before it gets better. We don’t need to remind readers that the June FOMC meeting will be the first with Kevin Warsh at the helm, but possible rate cuts will have to wait until either better inflation numbers, or a more dramatic weakening in the labor market, and neither of those appear likely anytime soon.

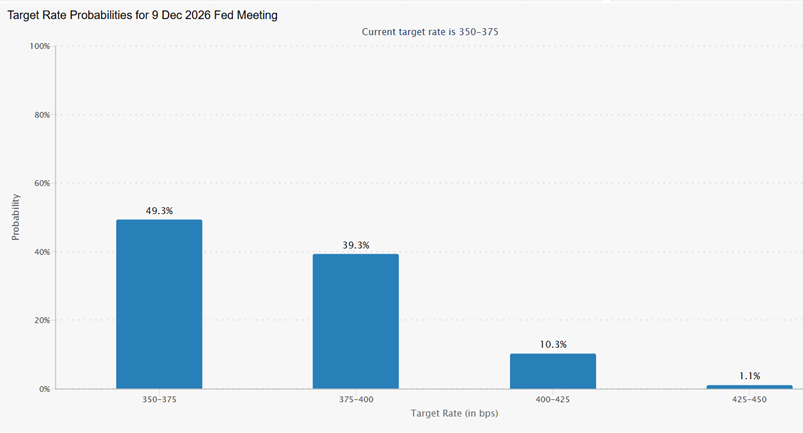

Fed Funds Futures Continue to Point to No Rate Cuts This Year with Rate Hiking Odds Increasing

Source: CME Group

ISM Manufacturing – Prices Paid Index Moves into 2022 Territory

April Job Opening and Labor Turnover Survey (JOLTS) Due Tomorrow Source: BLS

Source: BLS

May Jobs Report Due Friday – Expectation is for 95k New Jobs

Source: BLS

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.