Rate Hiking Odds Start to Appear

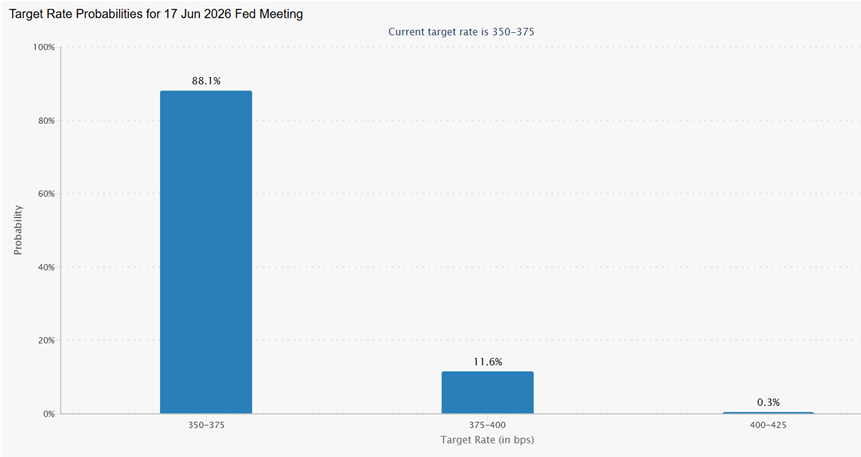

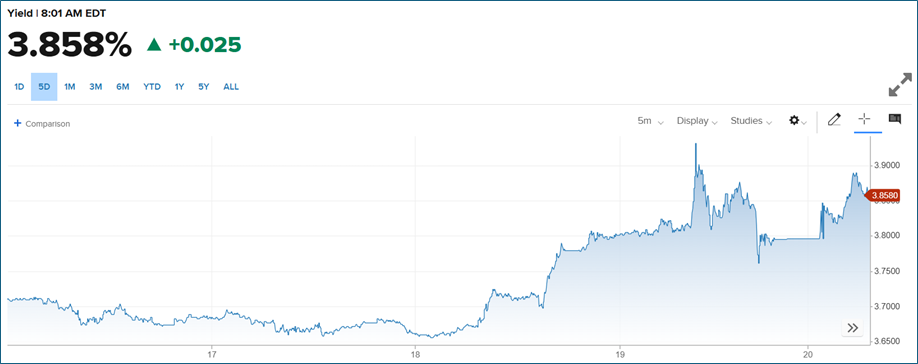

- Uncertainty created by the war in Iran continues to swirl, and the Fed has decided that it’s best to sit on the sidelines until more is known about the economic impact, and that has investors revisiting their expectations for monetary policy this year. The immediate result of the uncertainty is to price out any rate cuts for this year. Not only that, but odds of a rate hike are also starting to appear in futures markets, albeit tentatively. There is an old saying of uncertain origin that essentially says, “may you live in interesting times” and while the original expression was meant for turbulent, chaotic periods, I think it is an apt description of our current environment. Currently, the 10yr is yielding 4.30%, up 2bps, while the 2yr is yielding 3.85%, up 1bs on the day.

- The market continues to grapple with Powell’s Wednesday comments along with trying to game out the potential impact of the Iran war. The message from Powell was that the Fed will be in pause mode until inflation moves materially closer to 2%. With the impact of higher energy prices and second order pricing pressures yet to be felt in inflation reports, markets took the news and priced out any rate cuts this year.

- That had quite the impact on short end Treasury yields with the 2yr moving 15bps higher since the FOMC announcement. At 3.86%, the 2yr now yields above the current Fed Funds range of 3.50% – 3.75%, normally a ceiling, indicating the market is beginning to see a risk of rate hikes, not cuts. While we give a low likelihood to rate hikes, the realization that rate cuts will be few and far between this year has fed into the bearish tendencies that have prevailed since hostilities erupted in Iran, and with no economic news due today, war developments will dictate trading not to mention fear of event risk erupting over the weekend.

- Yesterday, sales of new single-family houses slowed dramatically in January to a seasonally adjusted annual rate of 587 thousand vs. expectations of 723 thousand. This is 17.6% below the December 2025 rate of 712 thousand and is 11.3% below the January 2025 rate of 662 thousand. The seasonally adjusted estimate of new houses for sale at the end of January 2026 was 476 thousand, or 0.4% above the December 2025, but 4.0% below the January 2025 estimate. This represents a supply of 9.7 months at the current sales rate. The record high was 12.2 months of supply in January 2009, during the depths of the housing crisis. The all-time record low was 3.3 months in August 2020. The current 9.7-month rate is above the top of the normal range (about 4 to 6 months of supply is normal).

- The median sales price of new houses sold was $400,500. This is 4.5% below the December 2025 price and 6.8% below the January 2025 price. The average sales price of new houses sold was $499,500, 5.9% below the December 2025 price and 3.6% below the January 2025 price. Slowing sales, increasing inventory, and decreasing sales prices are not examples of a healthy housing market. The bleak times in housing continue and that is before the higher rates coming on the heels of the Iran war.

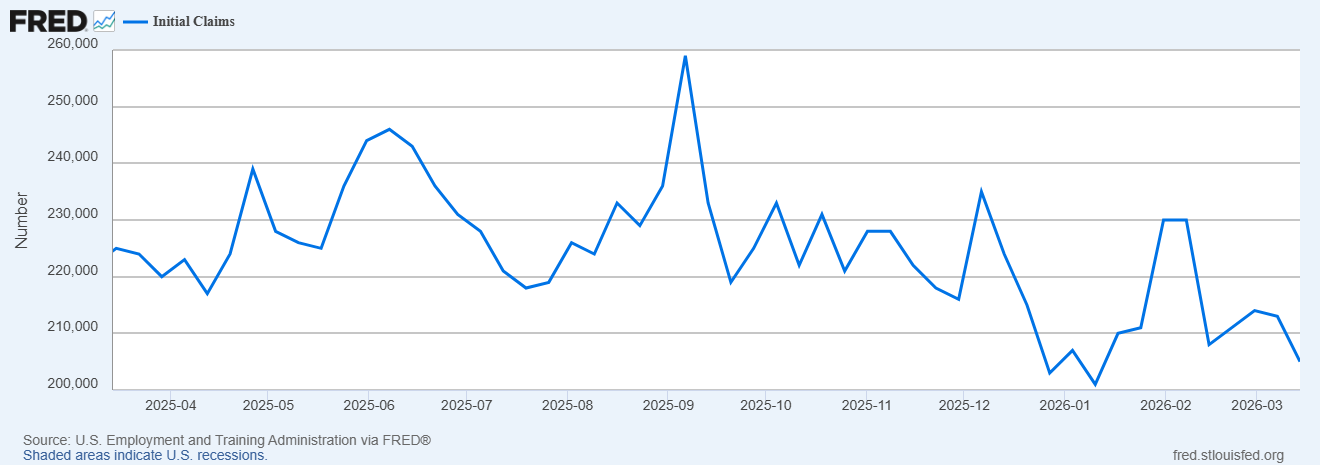

- Meanwhile, the weekly Initial Jobless Claims series printed another docile read on the state of the labor market. That is, the low-hire, low-fire environment continues. In the week ending March 14, seasonally adjusted initial claims totaled 205,000, a decrease of 8,000 from the previous week’s 213,000. The 4-week moving average was 210,750, a decrease of 750 from the previous week’s revised average.

- Continuing claims for the week ending March 7 was 1,857,000, an increase of 10,000 from the previous week’s level. The previous week’s level was revised down by 3,000 from 1,850,000 to 1,847,000. The 4-week moving average was 1,850,500, a decrease of 2,000 from the previous week’s revised average. Thus, while uncertainty abounds employers seem to be following the Fed and sitting on their collective hands hoping the uncertainty will soon clear, but at least they are waiting and not increasing job cuts into the uncertainty.

Rate Hiking Odds Now Appear for June FOMC Meeting Source: CME Group

Source: CME Group

2Yr Yield Moves Above Fed Funds Range of 3.50% – 3.75%

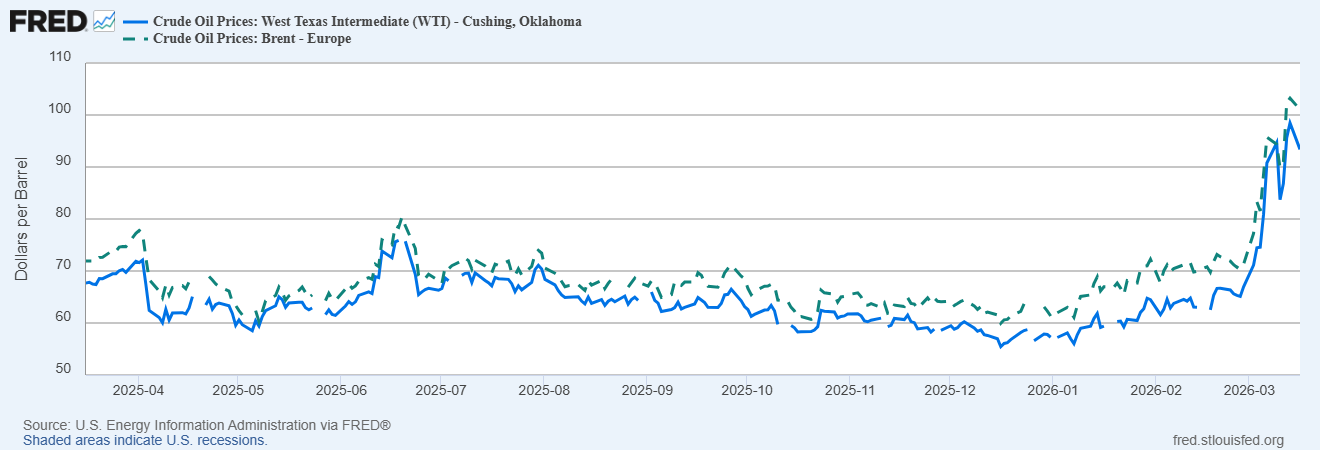

Brent Crude and West Texas Intermediate Prices Diverge Some in the Wake of the Iran War Impact

Initial Jobless Claims Quiet – Reflecting No Increase in Layoff Levels

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.