Retail Sales Rebound in February

- Reports that the Iranian President was seeking a resolution to the war led to a furious rally in financial markets yesterday as both Treasuries and equities rallied first and apparently asked questions later. While the war news has and will dominate trading, we were greeted with more reports of so-so consumer confidence and a labor market that continues to lose momentum, albeit gradually. This morning the February Retail Sales Report is the lead economic story with ISM Manufacturing coming a bit later in the morning. Currently, the 10yr is yielding 4.33%, up 2bps, while the 2yr is yielding 3.81%, up 1bp on the day.

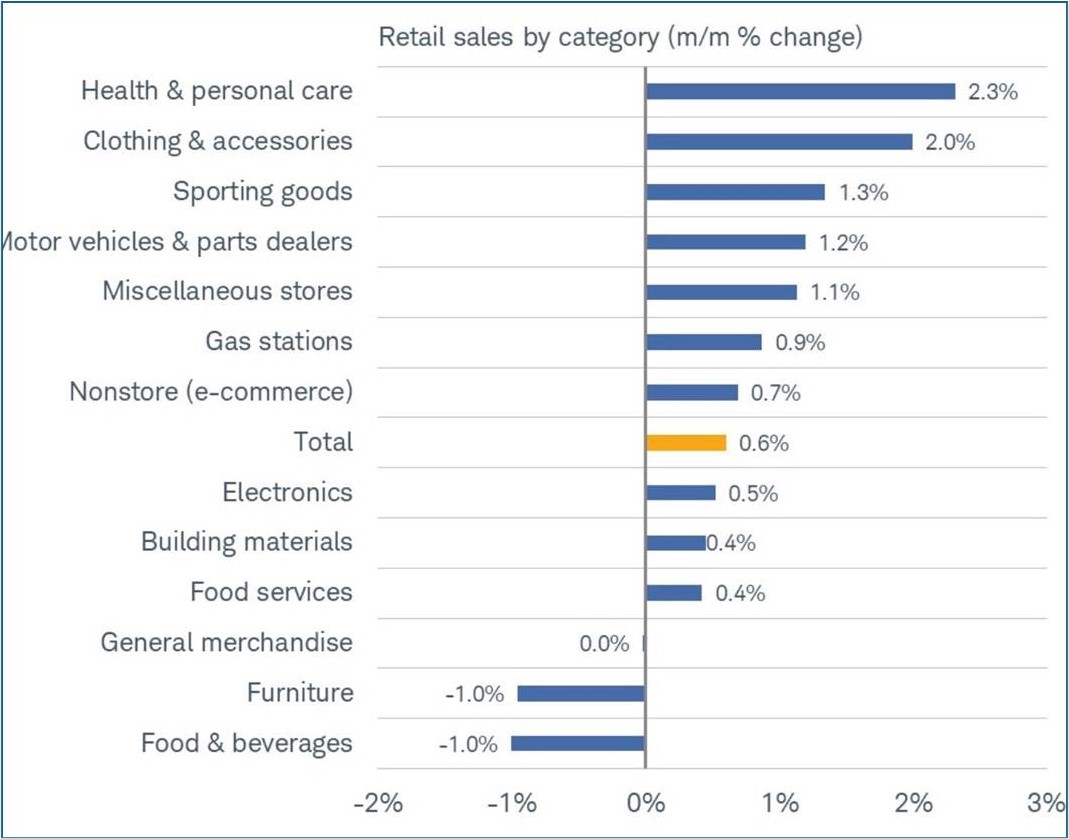

- Retail sales for February increased 0.6% for the month, offsetting a soft -0.1% contraction in January and above the 0.5% expectation. Sales ex autos were up 0.5% vs. unchanged in January and 0.3% expected. Sales ex autos and gas were up 0.4% vs. 0.3% expected and 0.2% in January. The direct feed into GDP, the so-called Control Group (sales net of autos, gas, building materials, food and drink services, and some small misc. categories), was up 0.5% vs. an expected 0.3%, and a downwardly revised 0.2% in January and matching the 0.3% expectation. The Control Group is thought to provide a “core” view of spending. Gains were heaviest in health and personal care and clothing and accessories. While February did rebound from the winter-affected January results, it will be considered somewhat stale coming before the Iran war. The other caveat we always offer is the report is presented in nominal terms (i.e., not inflation adjusted), and it’s more goods-focused than the broader and inflation-adjusted personal consumption number that comes in the Personal Income and Spending Report.

- Also, ADP reported 62 thousand new private sector jobs were created in March. That was above the 40 thousand expected but similar to the 63 thousand reported in February. The job gains were split almost evenly between goods-producing (30k) and service jobs (32k). The smallest firms (<20 employees) were by far the largest gainers at 119 thousand jobs, whereas medium (50-500 employees) and large firms ( >500 employees) lost 20k and 4k, respectively. The annual pay increase for job-stayers was unchanged for the third month at 4.5% while job-changers year-over-year pay gains improved slightly to 6.6%. The Friday BLS Nonfarm Payrolls March Report is expected to show 75 thousand new private sector jobs.

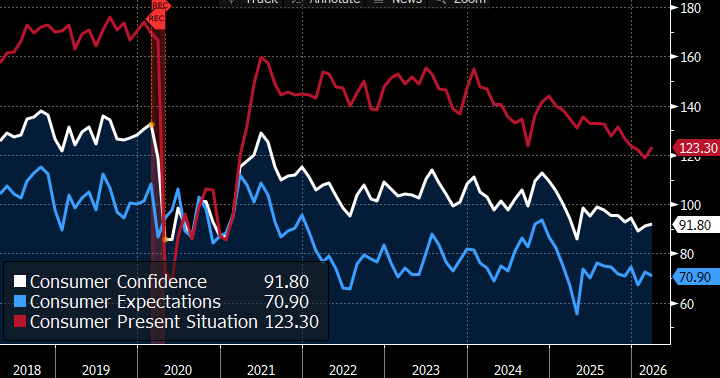

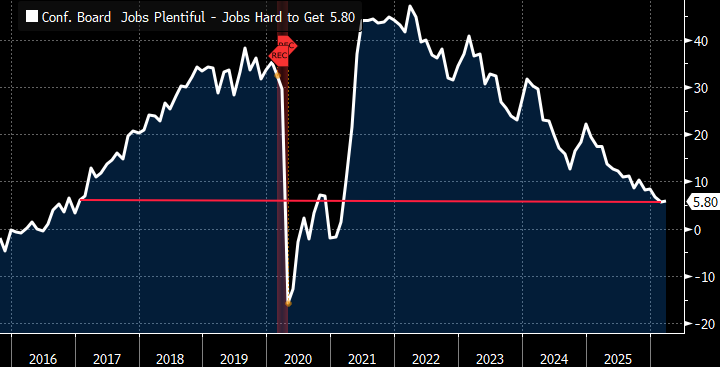

- If you recall, the University of Michigan Sentiment Survey last Friday was a rather discouraging read on consumer confidence, especially in the survey period encompassing the beginning of military operations in Iran. Yesterday, the Conference Board issued its Consumer Confidence Report for March, and it wasn’t great but not quite as discouraging as the Michigan results. In fact, consumer confidence unexpectedly improved to 91.8 in March vs. 91.0 in February and better than the 87.9 expectation. The Present Situation metric improved to 123.3 vs. 118.7 prior and 118.0 expected. The Expectations metric slipped to 70.9 vs. 72.0 in February but above the 68.4 forecast. The Labor Differential (Jobs Plentiful – Jobs Hard to Get) inched up to 5.8 from 5.7. Admittedly that’s minimal improvement and remains near the bottom of the range as labor market momentum continues to struggle (see graph below). Unsurprisingly, year-ahead inflation expectations jumped to 6.2% from 5.5%, the highest since May 2025. Unlike the Univ. of Michigan series, the Conference Board doesn’t provide a longer-run inflation outlook which the Fed likes to see “well anchored.” In summary, it’s a slightly better view of the consumer than Michigan.

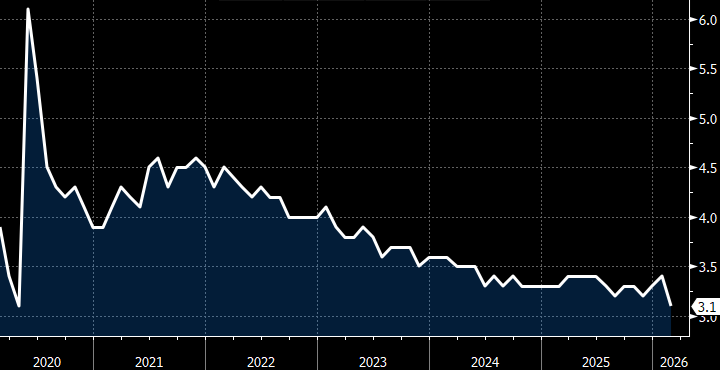

- Another February release from yesterday, this time on the labor side, reported a low energy view of the labor market which confirms what we’re seeing in a host of labor-focused reports. The Job Openings and Labor Turnover Survey (JOLTS) saw Job Openings slip to 6.882 million in February vs. 7.240 million in January (revised up from 6.946 million) and 6.890 million expected. The job openings/jobless ratio ticked down to 0.91 from 0.98, making it the eighth consecutive print below the 1 to 1 job opening to unemployed level. Meanwhile, the Hiring Rate (number of hires/total employed) fell to 3.1% from 3.4%. Excluding the pandemic period, it’s the lowest hiring rate since January 2011 and a clear sign of the low-hire environment. The Quits Rate (voluntary separations/total employed) declined to 1.9% from 2.0%, making it the lowest reading since October and below the level that prevailed pre-pandemic. The Quits Rate is a measure of worker confidence in finding a more desirable job. The declining rate indicates a slightly lower level of worker confidence and the slippage in job openings speaks to additional slowing in labor market momentum. Keep in mind too, these are February numbers, before the Iran war, so expect further slippage in the March report.

- The final report of the day will be at 10am ET with the March ISM Manufacturing Survey. Expectations are for the headline survey to be unchanged at 52.4, which indicates solid expansion that started in February and is expected to carry through March. The Prices Paid component, however, is expected to move even higher from 70.5 to 73.8 which if confirmed will begin the pricing in of higher costs stemming from the early effects of the Iran war. Other metrics, like New Orders (55.8 prior month) and Employment (48.8 prior month) will also reveal early impacts from military operations and shipping constraints.

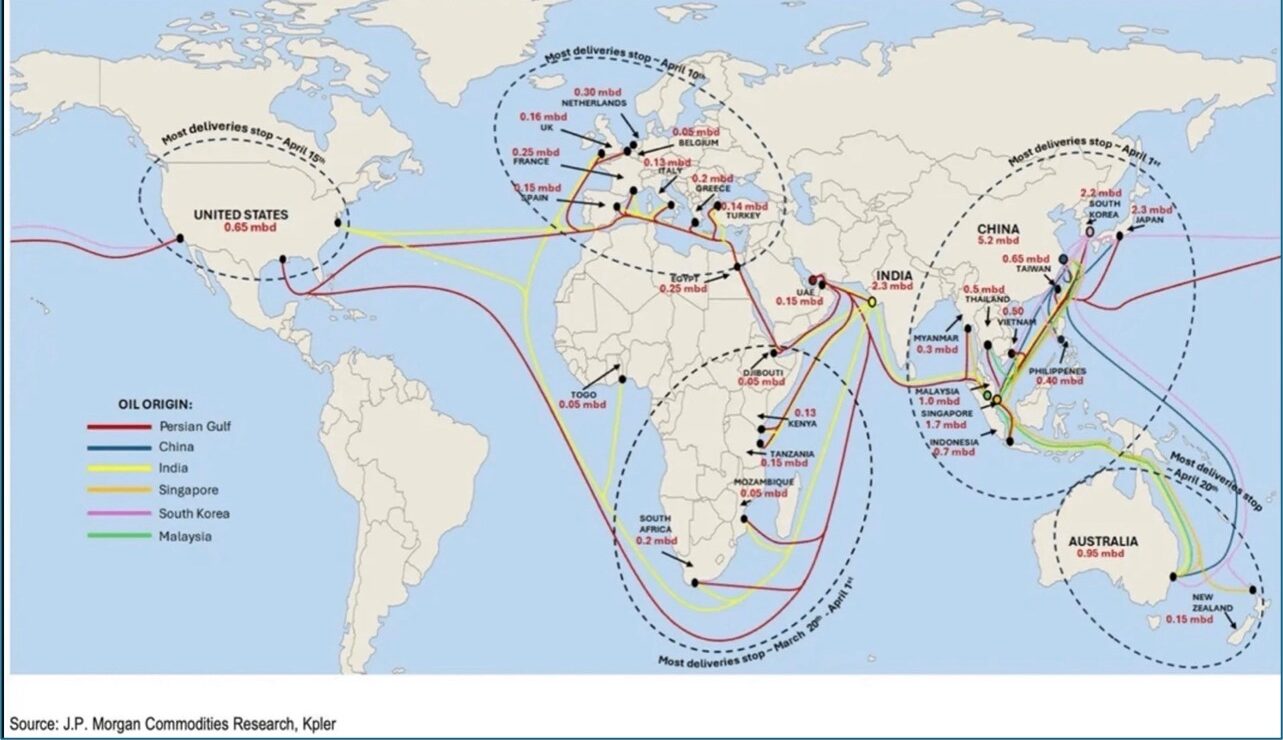

- Not to sound overly alarmist but shipping-related executives and industry experts seem to be more concerned over the shutting of the Strait of Hormuz than financial markets are pricing in. Sure, oil and related prices are higher, and equities have struggled, but in some views, the impact of the shipping blockage hasn’t really begun to be felt yet, but that’s about to change. JP Morgan analysts prepared a global view of when different areas will receive their final pre-war shipments through the strait. East Asia (China, Japan, Korea, etc.) will feel it starting today as the final pre-war shipments arrive with little behind them. The wave then spreads west to Europe in another week and finally North America a couple weeks after that. Keep an eye on markets and pricing in April as this wave slowly spreads across the globe (see graph below).

- Last Call. Last week I sat down with Billy Fielding, head of our Asset Liability Service and discussed what he is seeing in the latest AL reports and what he’s hearing about examiners as they review the latest AL results and procedures. It was an interesting discussion, so give it a listen here.

February Spending Strongest in Health & Personal Care

Source: US Census Bureau

Conference Board March Consumer Confidence Improves Slightly

Source: Conference Board

Conference Board Jobs Plentiful Minus Jobs Hard-to-Get: Improved a Tenth but Still Near a 10-Year Low

Source: Conference Board

February JOLTS – Hire Rate (New Hires / Total Employed) Dips to Lowest Since Covid-Era

Source: BLS

The Last Pre-War Shipments Through the Strait of Hormuz Arriving This Month

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.