Strength in April PMI’s Points to Cautious Inventory Building

- Retail sales strength earlier in the week was followed by solid preliminary April PMI numbers yesterday, but a more cautious take was it had more to do with building some safety into inventory levels ahead of possible price hikes and/or supply shortages. Thus, the Iran war and shipping blockage continues to dominate trading and now corporate actions. Tuesday’s release of March retail sales was surprisingly solid, even after accounting for higher fuel prices; meanwhile, ADP reported another solid week of job gains, and the latest initial jobless claims remain docile. Yet, the Iran war uncertainty looms. Later this morning, we’ll get the final numbers from the University of Michigan April Sentiment Survey and next week the FOMC will hold rates steady. Currently, the 10yr is yielding 4.31% down 1bp, while the 2yr is yielding 3.82% also down 1bp on the day.

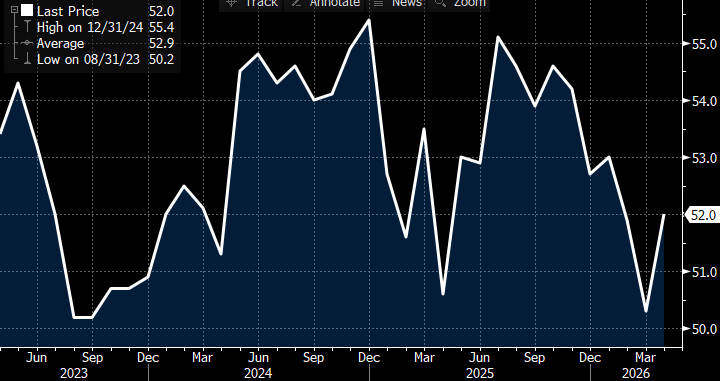

- The first report on April activity arrived yesterday and the S&P Global Flash PMI readings beat expectations and March results, but the chief economist for the group added a note of caution. The manufacturing segment registered a 54.0 vs. 52.3 in March and represents a 47-month high. Meanwhile, the services sector printed at 51.3 vs. 49.8 in March. The composite index rose from 50.3 to 52.0. This series operates similarly to ISM in that 50 represents the dividing line between an expanding and contracting sector.

- Chris Williamson, Chief Economist at S&P Global, painted a more sober view of the report, “A rebound in business output growth in April is good news after the near-stagnation seen in March, but over the past three months we have seen the weakest expansion of output recorded since the start of 2024 with the war in the Middle East squarely to blame. The report is broadly consistent with the economy struggling to manage annualized growth of more than 1%, with the vast service sector acting as the principal drag. Orders for services ranging from travel and tourism to financial products barely rose as the war caused hesitancy for spending among both household and business customers, with surging prices and the prospect of higher borrowing costs acting as a further deterrent.”

- He did note better performance in the manufacturing sector but remained cautious. “There was better news from manufacturing, but here an expansion of output and orders could be partly traced to the building of safety stocks, with survey respondents reporting “panic” and “emergency” buying ahead of price hikes and supply shortages in echoes of the problems seen during the pandemic. Not surprisingly, prices are already spiking higher in this environment, and not just for energy but for a wide variety of goods and services. The overall inflation picture is now the most worrying for almost four years.” In essence, Williamson identifies the pick-up in activity as more a strategy to build inventories ahead of what could be higher prices and/or supply concerns.

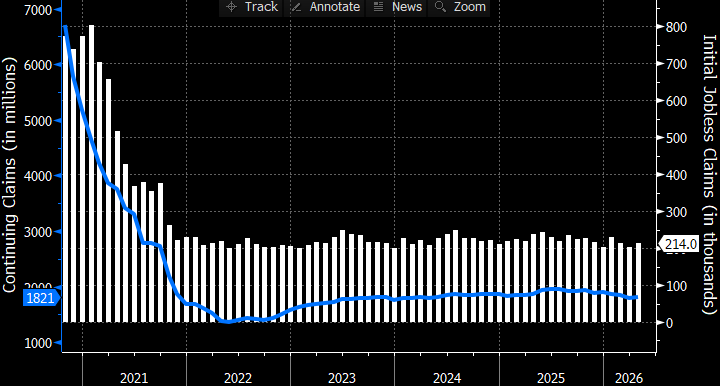

- Meanwhile, initial jobless claims and continuing claims continue with the low-fire theme even as hiring appears (per ADP) to be gaining some renewed momentum. Initial claims for the week ending April 18 rose slightly from 207 thousand to 214 thousand. The 4-week average ticked gently higher from 209.75 thousand to 210.75 thousand. Continuing claims for the week ending April 11 rose slightly from 1.818 million to 1.821 million. As the graph below shows, however, little has changed between the two measures for months now as companies may have slowed hiring but they seem content to hang onto employees through the current war-induced uncertainty.

- At 10am ET, the final University of Michigan Sentiment Survey will be released. Last week’s preliminary numbers saw sentiment fall to new lows but a slight improvement off those levels is expected in today’s final look, but not by much. The inflation outlook will get some attention as well but with stability expected there with 1yr expectations unchanged at 4.8% and 5-10yr inflation expectations also unchanged at 3.4%.

- The highlight next week will be the Fed’s rate decision on Wednesday with no change in rates the expected outcome. Also, the Personal Income and Spending Report for March will follow on Thursday, April 30. Spending gains are expected, like what we saw earlier this week in the Retail Sales Report, and overall PCE inflation is expected to increase from 2.8% to 3.5% YoY and core PCE from 3.0% to 3.2% YoY.

- Finally, while next Friday is May 1st, the April BLS Nonfarm Payrolls Report won’t be released until the following Friday, May 8, leaving next week clearly in the grip of the Fed and Iran war news with a side of March PCE inflation and spending data.

S&P Global Preliminary April Composite PMI Moves Higher. Is it Cautious Restocking? Source: S&P Global

Source: S&P Global

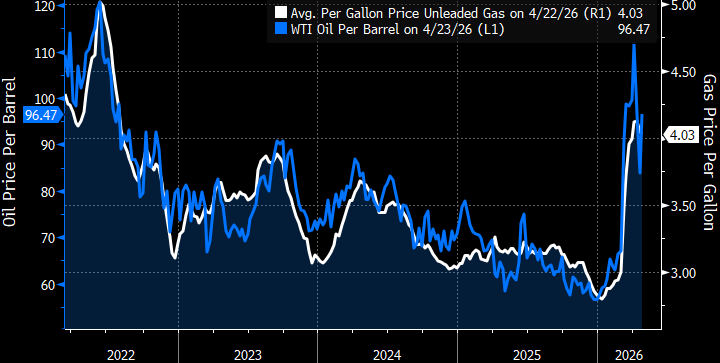

Oil Prices Off their Highs, Gas Prices Not so Much Source: Bloomberg

Source: Bloomberg

Weekly Jobless and Continuing Claims Show the Low-Fire Economy Continues Source: Dept. of Labor

Source: Dept. of Labor

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.