Tariff Ruling Reaction

- This week was supposed to be something of a placeholder with mostly second-tier economic releases but the Supreme Court’s tariff ruling from Friday adds an element of intrigue into the week. With the Court declaring the use of IEEPA to implement tariffs as unconstitutional, markets are poised for a reaction from the White House. While the ruling was expected, which explains the muted reaction on Friday, it created immediate uncertainty regarding how the administration would react, and they reacted almost immediately with new tariffs. That should spice up what initially was looking like a slow February week. Currently, the 10yr is yielding 4.07%, down 2bps, while the 2yr is yielding 3.48%, unchanged on the day.

- As we mentioned above, while the Supreme Court tariff ruling was not a surprise, it does add uncertainty to the future direction of trade policy. While the administration can use other legal authorities to implement tariffs, those are more limited and circumscribed compared to the use of IEEPA which the administration tried to use for most of the tariffs imposed in the past year. The administration wasted no time in replying Friday afternoon as President Trump signed an executive order imposing a new 10% “global tariff” that was quickly bumped to 15%.

- The new tariffs will come on top of the existing levies that remain intact following the high court’s decision. The new duties, which are being invoked under Section 122 of the Trade Act of 1974, can only last for 150 days, with any extension requiring congressional approval. Trump also declared that all the tariffs currently active under statutes known as Section 232 and Section 301 will remain “in full force and effect.” The administration is also wielding Section 301 to launch several investigations into potentially unfair trade practices, which could result in additional new tariffs. Expect more to come on this subject during the week.

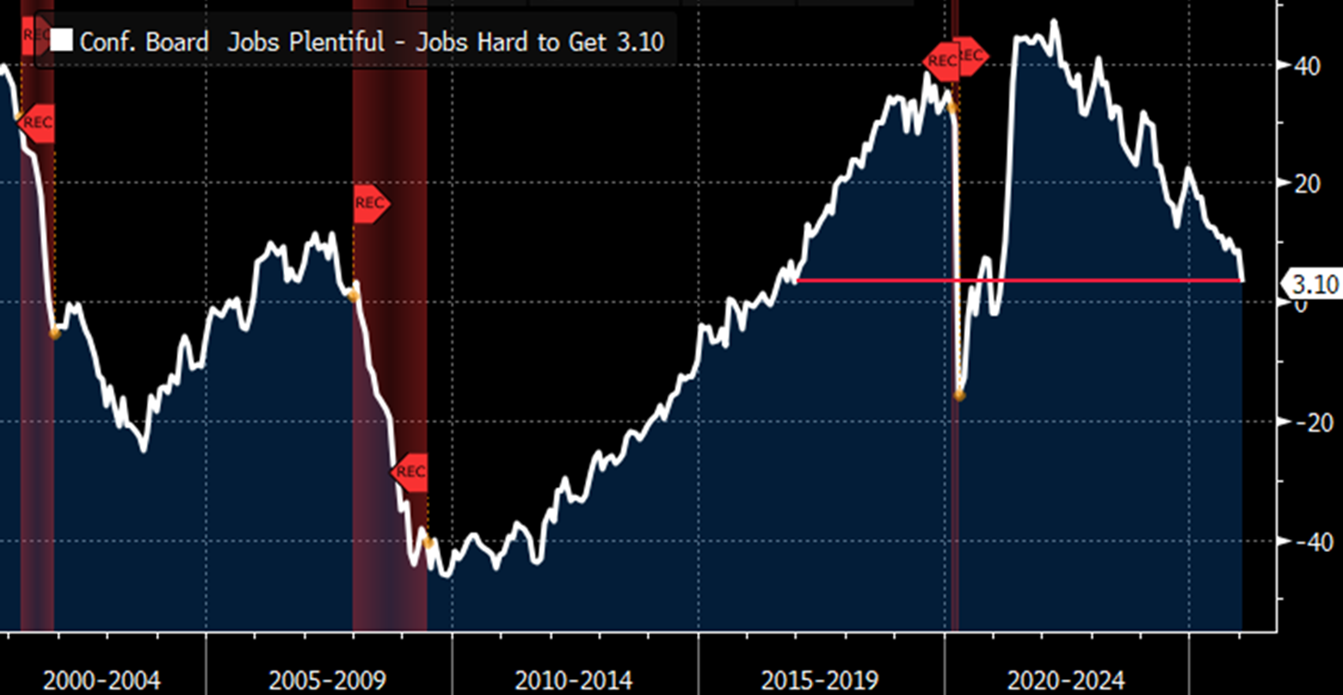

- As for data this week, it’s light with the headline release being the Conference Board’s Consumer Confidence Survey for February due tomorrow. While consumers, in various surveys, have been rather dour in their sentiment it hasn’t dented spending much, at least by the higher income cohort. But with spending easing slightly at the close of the year, any further deterioration could add more caution for investors. The Labor Differential (Jobs Plentiful – Jobs Hard to Get) will garner attention as it has been trending in the harder-to-get direction for months now. Does that continue in February? We shall see.

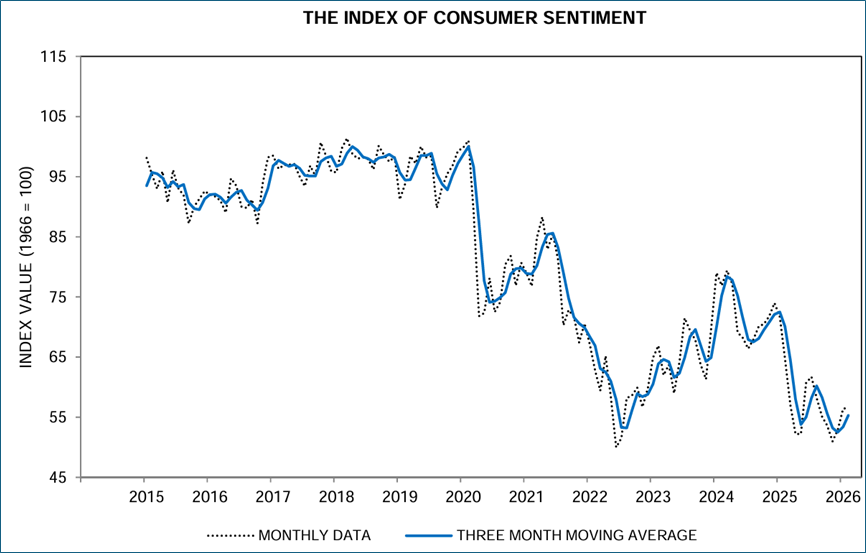

- Speaking of consumer sentiment, on Friday the University of Michigan released its final February report. Not surprisingly, consumer sentiment stagnated with very little change, just 0.2 index points higher than January. That said, sentiment is about 13% below a year ago and 21% below January 2025. That said, the outlook varied considerably across the population. A sizable month-to-month increase in sentiment for the largest stockholders was fully offset by a decline among consumers without stock holdings. Similar divergences were seen across income and education, where higher-income or college educated consumers exhibited increases in sentiment while lower-income or less-educated counterparts did not. With their much stronger income prospects and investment portfolios, wealthier and higher-income consumers feel better insulated from any possible risks to the economy.

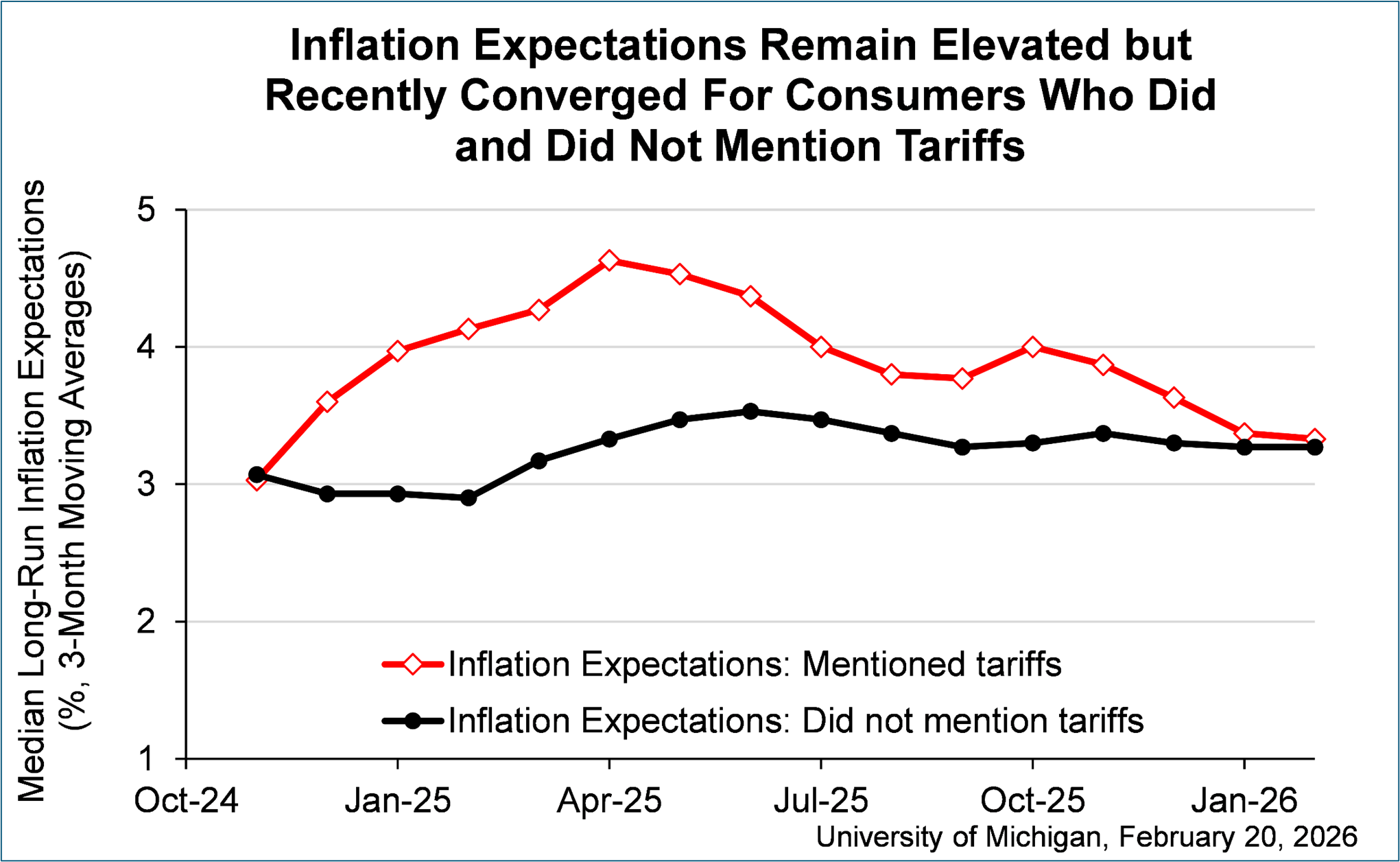

- Given the latest reading of FOMC minutes that confirmed the Fed is firmly fixed on inflation as guiding future policy moves, inflation expectations are a critical piece of information. In that regard the Michigan survey found year-ahead inflation expectations fell from 4.0% last month to 3.4% this month, the lowest reading since January 2025. This month’s reading still exceeds those seen in 2024 and remains well above the 2.3-3.0% range seen in the two years pre-pandemic. Long-run inflation expectations held steady at 3.3%, just above the 2.8% and 3.2% range seen in 2024. In 2019 and 2020, long-run inflation expectations were consistently below 2.8%. Uncertainty, as measured by the middle 50% of expectations, is now its lowest since December 2024 for the short run and October 2024 for the long run. Bottom line here is that while inflation expectations are moderating from recent spikes, they are still above pre-pandemic levels but uncertainty regarding direction is falling, and that is a good thing.

- Finally, year-ahead inflation expectations fell from 4.0% last month to 3.5% this month, the lowest reading since January 2025. This month’s reading still exceeds those seen in 2024 and remains well above the 2.3-3.0% range seen in the two years pre-pandemic. Long-run inflation expectations inched up for the second straight month, from 3.3% last month to 3.4% this month. In comparison, readings ranged between 2.8% and 3.2% in 2024 and were below 2.8% throughout 2019 and 2020. That “stickiness” in long-run inflation expectations will be a concern for the inflation hawks at the Fed.

- While we have January CPI in hand from nearly two weeks ago, on Friday we’ll get January PPI with expectations centered around 0.3% MoM increases for both Final Demand and Final Demand ex-Food and Energy. While the wholesale inflation numbers may be somewhat anti-climactic coming so late after CPI, the report does fill in some key pieces that feed into the PCE report. Given the hottish readings from December PCE how those components look in January will allow analysts to finalize estimates for January PCE which the BEA has yet to announce a release date.

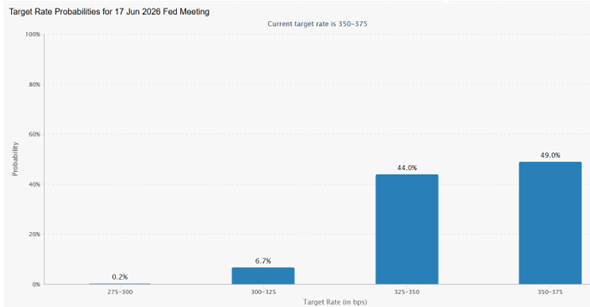

Odds of a June Rate Cut Now Only 50-50 Source: CME Group

Source: CME Group

Univ. of Michigan Sentiment Survey Finds Long-Run Inflation Expectations Trending Slightly Lower Source: Univ. of Michigan

Source: Univ. of Michigan

UMich Sentiment – Off the Lows but Still Pretty Pessimistic Source: Univ. of Michigan

Source: Univ. of Michigan

Conference Board’s Labor Differential (Jobs Plentiful – Jobs Hard to Get) Heading Below Zero? Source: Conference Board

Source: Conference Board

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.