The Davos Catalyst

- The range trade for the past month was decisively broken yesterday, driven by geopolitical events, and the resolution has been for higher yields as the Greenland dust up rekindled another round of the “Sell America” trade. With Trump scheduled to speak within the next hour at the Davos World Economic Forum, there’s potential for more volatility. So far, the 10yr has touched 4.31% which is the highest since August, but 4.50% remains a nearby psychological target. Meanwhile, if diplomatic efforts prevail, a rally is likely to stall around 4.23% which represents the 200-day moving average. With data flow slow this week all eyes and ears will remain fixed on the Davos conference. Currently, the 10yr is yielding 4.29%, down 1bp, while the 2yr is yielding 3.58%, down 2bps on the day.

- As we so presciently mentioned last Friday, there was little on the calendar before the January 28 FOMC meeting, thus, the range trading that defined the action this year was likely to continue. Our caveat to the range trade was the potential for geopolitical events to flip the script. Well, we got that. The Trump administration’s weekend notice that Greenland will be part of the US one way or the other was enough to set off the next “Sell America” trade including Treasuries.

- As an aside, we mentioned last week that the 10yr Treasury had traded between 4.10% and 4.20% for weeks such that the two standard deviation Bollinger Band measure drifted inside 10bps. The previous five times the Bollinger Band measure was less than 10bps it resolved with an upside yield break, averaging 20bps. Well, make that six straight times, with a high just over 4.30%. That still leaves it shy of the 20bps average move. That average, if hit, would put the yield near 4.40%, with 4.50% a clear psychological target if the Greenland impasse continues.

- While there are plenty of worse-case scenarios that one can envision for this situation, one of the uglier ones is that Europe collectively holds around $8 trillion in US Treasuries out of about $28 trillion publicly marketable (vs. $38 trillion total outstanding). Thus, selling down some of this would obviously weigh heavily on the market and boost yields higher. That’s the bazooka that Europe has, but doesn’t want to use.

- Speaking of tariffs and Greenland, the Supreme Court has yet to issue a ruling on the legality of the IEEPA tariffs, so that uncertainty continues. Thanks guys and gals for not wanting to be rushed into a hasty decision, jeez. Today, they are busy hearing the Lisa Cook termination case, so that likely pushes the tariff decision away for another day.

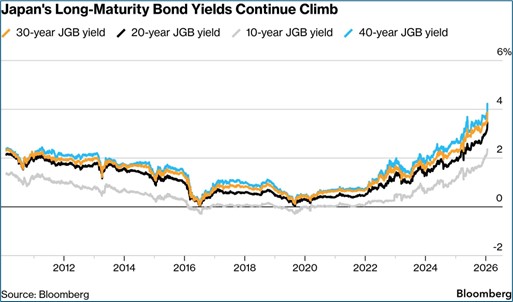

- The backup in yields isn’t all about Greenland. Most of it yes, but a little push was provided by Japan as their new prime minister is promoting the idea of a new tax exemption on food to improve affordability and promote consumption. It’s part of a larger plan to boost spending and cut taxes to stimulate the economy but it brings with it fiscal concerns. That has Japanese yields hitting multi-year highs which is contributing to the global bond selling, but on a second-order level.

- While we’ve mentioned the data void, there is one report, the October and November PCE release, that will finally be published tomorrow. The stale nature of the release, not to mention current events, dims some of the luster from what is usually an intensely followed report. Expectations are for a docile read on core inflation at 0.2% MoM and 2.8% YoY. Income for November is expected to have increased 0.4% MoM and spending 0.5% or 0.3% after inflation. The 8:30am ET release tomorrow will get market attention as the Davos news continues.

- Also, yesterday the ADP Weekly Pulse Report found 8 thousand new private sector jobs for the week ending Dec. 27th (based on a four-week moving average). That level, spread across a month, is mid 30’s to 40 thousand jobs which is like the 37 thousand private sector jobs reported for December. So, the most current read on jobs continues to reflect a labor market essentially stuck in neutral.

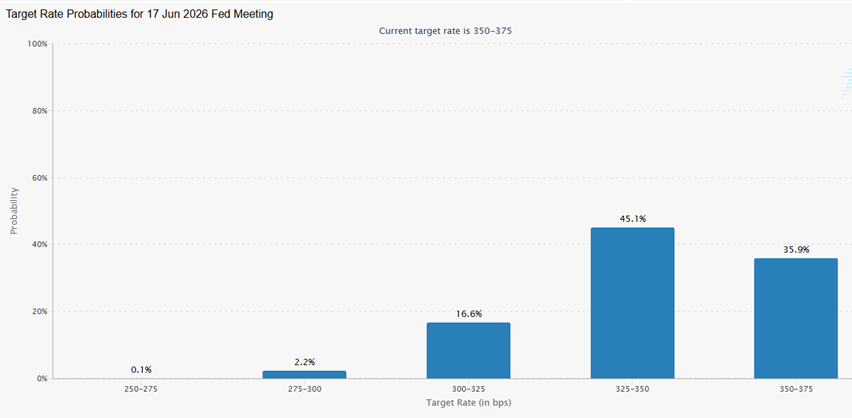

Through it All, Futures Still Still See June Meeting for Next Cut

Source: CME Group

Source: CME Group

10Yr Treasury Range Trade Resolves to the Upside with Geopolitics Stoking the Move

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.