The Range Trade Continues

- With first-tier economic reports done for a while, and a holiday-shortened week upcoming, there’s little on the horizon that could be identified as a possible catalyst to upset the range trade we’re in. That means more emphasis on potential geopolitical events to upset the apple cart, and, if anything else, this administration knows how to engage in geopolitical machinations. The Supreme Court ruling on tariffs and the Iran protest situation are two potential sources of vol, but for now they have receded slightly from the scene. Currently, the 10yr is yielding 4.19%, up 3bps, while the 2yr is yielding 3.58%, up 1bp on the day.

- There remains little on the calendar between now and the next FOMC meeting on January 28th, thus, the range trading that we’ve witnessed so far in 2026 is likely to continue. In fact, the 10yr Treasury has traded between 4.10% and 4.20% such that the two standard deviation Bollinger Band measure is inside 10bps. The two bands sit at 4.11% and 4.19%, or 8 bps, the narrowest since January 2021. The last five times that the Bollinger Band measure has been less than 10bps it’s resolved with an upside yield break averaging 20bps. Keep that in mind if you’re planning to deploy some capital in the near future. Of course, the question is do you expect that the sixth time will break the streak, or continue to resolve with higher yields?

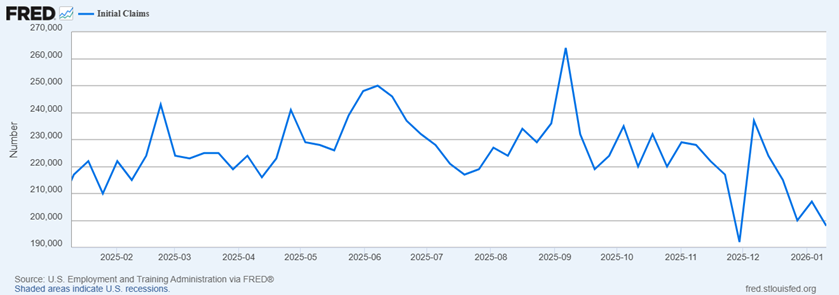

- Meanwhile, initial jobless claims continued with the low-hire, low-fire routine. In the week ending January 10, initial jobless claims totaled 198,000, a decrease of 9,000 from the previous week’s revised level. The previous week’s level was revised down by 1,000 from 208,000 to 207,000. The 4-week moving average was 205,000, a decrease of 6,500 from the previous week’s revised average and the lowest since January 20, 2024.

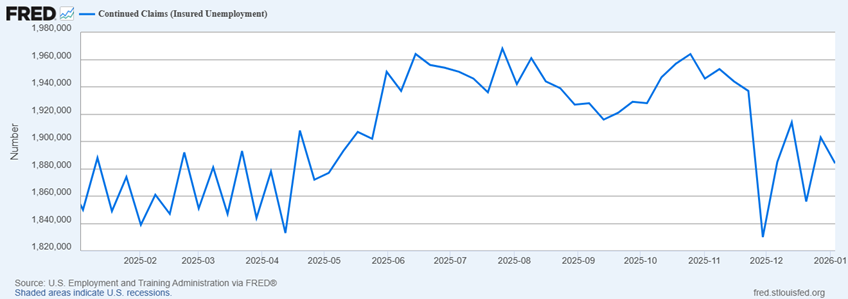

- During the week ending January 3 continuing jobless claims totaled 1,884,000, a decrease of 19,000 from the previous week’s revised level. The previous week’s level was revised down by 11,000 from 1,914,000 to 1,903,000. The 4-week moving average was 1,889,250, a decrease of 250 from the previous week’s revised average. Thus, the latest real-time read on jobless claims continues the 2025 trend with no pick-up in layoffs noted, while continuing claims remains somewhat elevated. That illustrates the challenging nature of finding new employment, and while not moving dramatically higher, the elevated state of continuing claims indicates something of a weakening equilibrium in the labor market.

- In line with the jobless claims data, the latest Fed Beige Book of economic conditions across the 12 Federal Reserve districts noted little change in activity. In fact, 8 of 12 districts saw only slight to moderate increases in economic activity since the December FOMC meeting. Three districts noted no change in activity and the New York Fed noted a decrease in economic activity. So, the so-so state of economic growth combined with little change in jobless claims indicates an economy that’s shifted into a lower gear, but still moving forward.

- Also, yesterday the November Import and Export Index was released and came in a little hotter than expected and probably represents the final nail in the coffin for those still hoping/positioning for a rate cut later this month. Import prices rose 0.4% for the month and 0.1% YoY. Import prices ex-petroleum rose 0.6%. Keep in mind, these price changes are before any tariffs, so if you were expecting the exporter to shoulder some of the tariff hit via lower selling prices we’re not seeing that. Export prices also rose during the month 0.5% MoM and 3.3% YoY.

- Later this morning, we’ll get December Industrial Production numbers along with capacity utilization followed by the National Association of Home Builders Index for January. For the home builders, a depressed level of 40 is expected (it uses the same 50 dividing line between expanding and contracting sectors like the ISM reports. The dog days of 2025 seem to be following the housing market into early 2026. That’s it for the week and frankly next week offers up only second tier reports that are unlikely to move the market out of its recent range-trading mode.

Initial Jobless Claims Drop Below 200 Thousand – The Low Hire, Low Fire Economy Continues

Continuing Claims Remain Elevated but not Increasing from Recent Levels

The Range Trade and Low Volatility Continues with Little on the Horizon to Upset the Trend

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.