The Tax Man Cometh

- Today marks the deadline to file your 2025 tax return, and for all those owing Uncle Sam some more money I imagine at some point today the return will be reluctantly placed in the mailbox, or the send button on the computer grudgingly pressed. Apart from our collective fiscal obligations, the war story continues and the final bits of March inflation data dribble in (more on that below). For now, markets are behaving with WTI oil back under $100 ($91 to be exact) despite the double blockade of the Strait of Hormuz. It’s a tentative start to the day, however, with equity futures vacillating around unchanged and Treasury yields in familiar territory. Currently, the 10yr is yielding 4.27%, up 1bps on the day, while the 2yr is yielding 3.76% also up 1bps on the day.

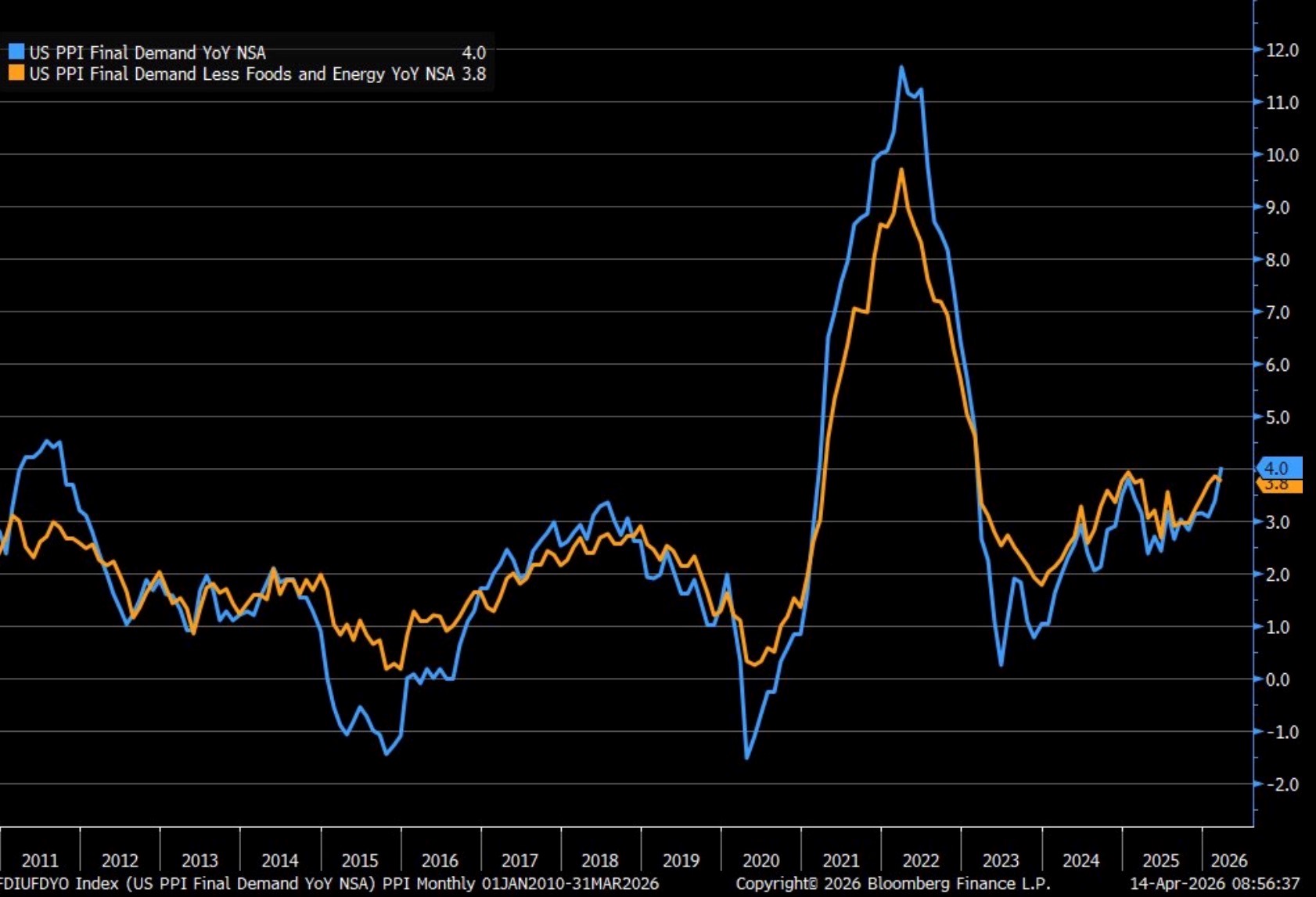

- As mentioned above, the March PPI numbers were received yesterday and the expected surge in energy costs were on display, little else, however, exhibited much upward pressure. That will come in later reports. Final Demand PPI rose 0.5% vs. 1.1% expected and 0.6% in February (revised down from 0.7%). The YoY rate increased from 3.4% to 4.0%, and while it’s the highest annual rate in three years it still trailed the robust 4.6% expectation. PPI ex-food, energy, and trade rose a modest 0.2% vs. 0.4% expected and 0.5% the prior month. The YoY rate increased from 3.5% to 3.6%. Expectations were for 3.8%. Those YoY rates, however, seem destined to move up to levels last seen coming off the peak rates following the post-lockdown surge in prices in 2022-23 (see graph below).

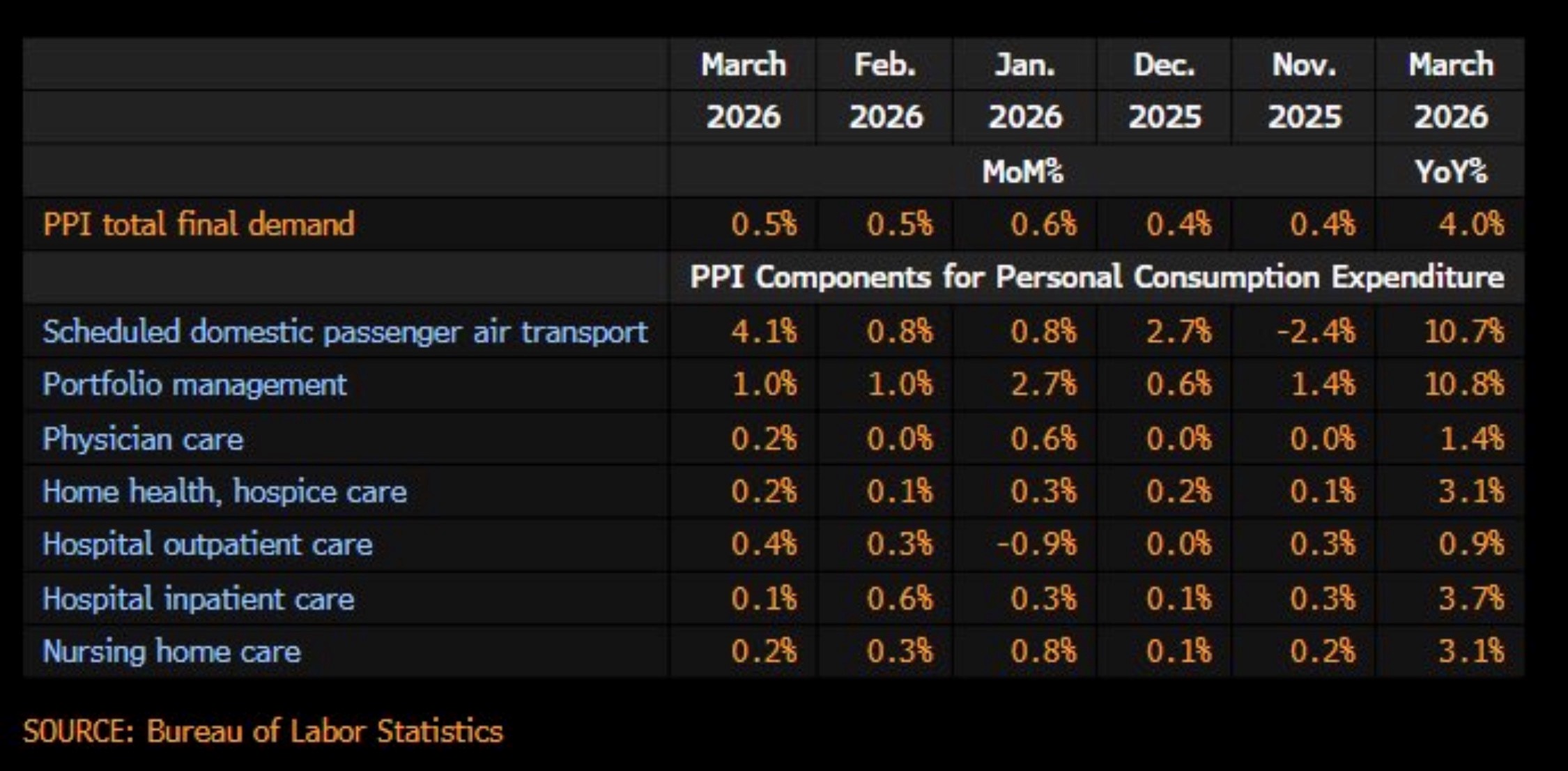

- Wholesale inflation was almost all on the goods side as that rose 1.6%, with energy (+8.5%) accounting for the bulk of the goods-side increase. The service side was unchanged, but that will change in future months if energy costs remain elevated. Thus, the wholesale inflation story looks a lot like what we saw in the retail-level CPI readings; big moves in the energy/gas sector but little other pricing pressure. Much like CPI, that will change if energy costs remain elevated. Also, five of seven sectors that feed into the PCE inflation series were higher in March vs. February which doesn’t bode well for the next PCE inflation report due at month end (see graph below).

- We’re reminded of how the tariff story played out last year with nary a big jump from one month to the next. Rather, it was more drips of cost pressure that showed in puddles rather than pools over many months as tariff rates changed and/or implementation dates delayed and sellers developed other workarounds. The oil and gas cost pressures are more sudden and pervasive, so we suspect cost pressure will arrive sooner for those using just-in-time inventory. Others, with pre-war stockpiles of cheaper inventory, can delay price increases temporarily, but not forever. This is a long way of saying that even if the war stopped today, and normal shipping resumed, the cost impact will continue to ripple across the global landscape for months to come.

- And while we wait for more price pressure to show itself, the latest ADP Pulse report showed an increase of 39,250 new private sector jobs for the week ending March 28th. That’s the largest weekly total this year and represents the fourth straight week of increasing job gains. While hiring plans don’t change on a dime, it is encouraging to see solid job growth in March despite the recent onset of hostilities with Iran. We should note too, this is survey week for the BLS as it begins compiling April job numbers. With the positive backdrop from ADP, and the docile weekly jobless claims, it seems April could be another decent month for jobs, but we’ll try and not get too far over our forecasting skis.

- We’ll also add another nugget to mix in that the Sunday screening totals provided by TSA were the highest this year, approaching 3.0 million with a recent range in the 2.0 – 2.7 million level. That strongly hints at another solid month of consumption, at least by the traveling class, which means the upper arm of the K-shaped economy seems to be staying in the consumption game, despite higher gas and airfare costs.

- The caveat here is that the war came suddenly, as did the energy/gas price impact. Trips and plans reserved months ago most likely were not cancelled, at least not in sizeable numbers. It’s the tentative plans for the summer season that may be curtailed if fuel and travel costs remain elevated. That’s all to say any downside impact to demand will probably happen in the second half of 2026 which is why we are keeping our call for a fourth quarter 25bps cut intact.

- A final piece that feeds into the Fed’s preferred PCE inflation measure was released this morning with the March Import Price Index. Prices rose 0.8% vs. 2.0% expected and 0.9% the prior month. Ex-petroleum, prices increased 0.6% vs. 0.5% expected and 0.8% in February. On a YoY basis, import prices rose 2.1% vs 3.9% expected and 1.3% the prior month. That’s the highest YoY rate since Dec. 2024. Ex-petroleum, YoY import prices rose 2.8%, the highest since Oct. 2022. Shipping costs are a big part of import pricing, but March was too early to see rates significantly higher since most goods travel on contracts negotiated well before the Middle East war. However, spot rates have increased, and the longer the war drags on fuel costs and elevated insurance rates will eventually drive import prices higher, and as we see in today’s report we’re already dealing with multi-year highs.

- Thus, we see the cost impact from the war coming in waves for months, possibly into 2027. Absent a real downturn in the labor market, that will keep inflation rates well above the Fed’s 2% target thus limiting the possibility of anything more than a cut or two at the most in a real economic softening scenario.

PPI – Final Demand and Final Demand Less Food and Energy (YoY): Notice the Trend?

PPI Components Feeding into PCE – See Airfares

Iran Wants Ships to Transit Near its Islands to Collect Tolls – Either in Crypto or Chinese Yuan

Source: Marine Traffic

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.