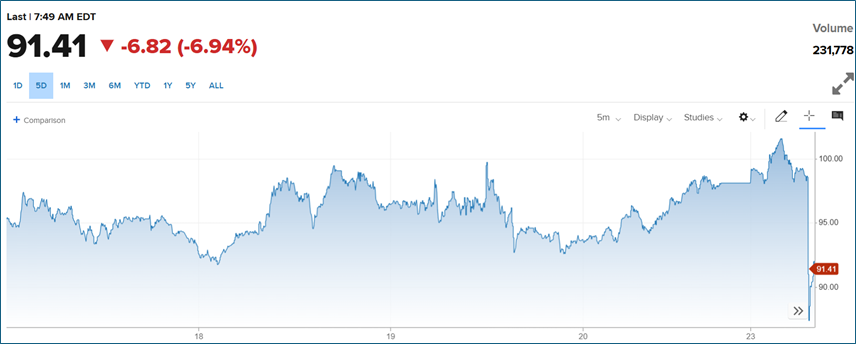

Trump Announces Optimistic Talks with Iran, Oil Prices Fall

- Oil prices tumbled this morning after President Trump said the U.S. and Iran had productive talks, leading him to order a halt on strikes against key energy infrastructure in the country. West Texas Intermediate futureswere down 7% at $91 per barrel. Brent crude lost around 8% as well to trade at $104. Risk-on is the early theme of the day with Dow futures up over 700 points. This week the economic calendar is light on first-tier reports so war news will dominate headlines and trading as we’re seeing this morning. One thing we’ve learned with this administration is that headlines and events can change on short notice, so strap in! Currently, the 10yr is yielding 4.38%, down 2bps, while the 2yr is yielding 3.90%, up 1bp on the day.

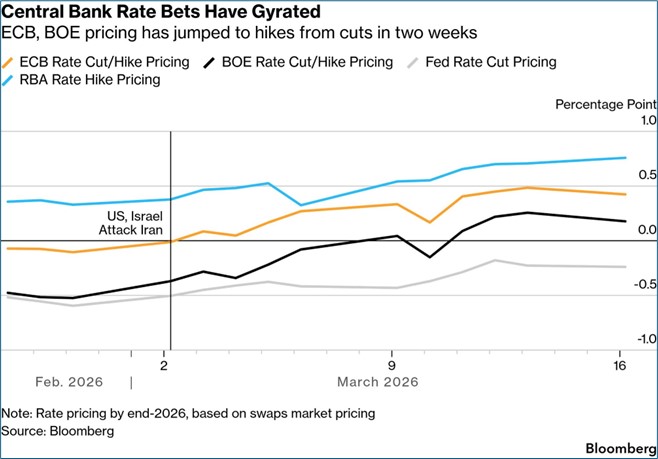

- One of the factors pushing short end yields higher is the “help” from Europe. Both the Bank of England (BoE) and European Central Bank (ECB) had meetings last week, like the Fed, and both paused, like the Fed, but their commentary was much more hawkish with less than veiled threats of rate hikes to come. A couple factors are driving that outlook. First, those central banks only have a single inflation mandate unlike the Fed’s dual mandate to also consider full employment. Second, Europe is facing a more critical increase in petro-related costs. Brent crude is trading higher than the normal spread to our West Texas Intermediate and natural gas and other fuels like diesel have risen much more than our gas prices domestically. So, look to Europe for another reason for the upward yield pressure.

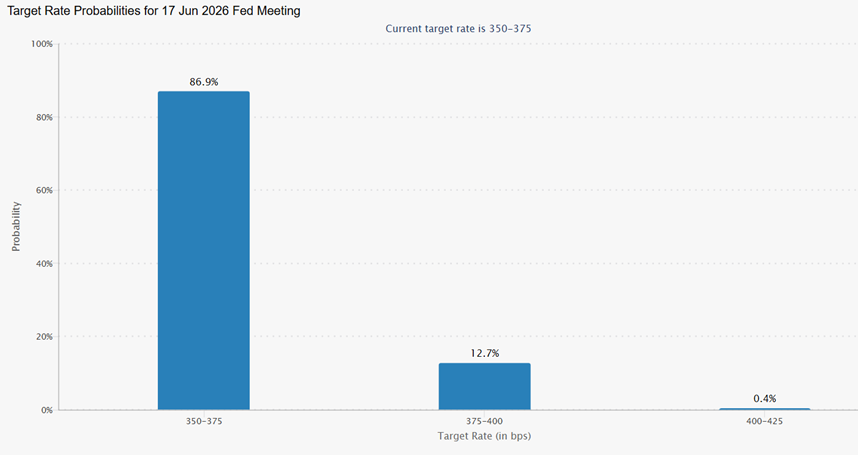

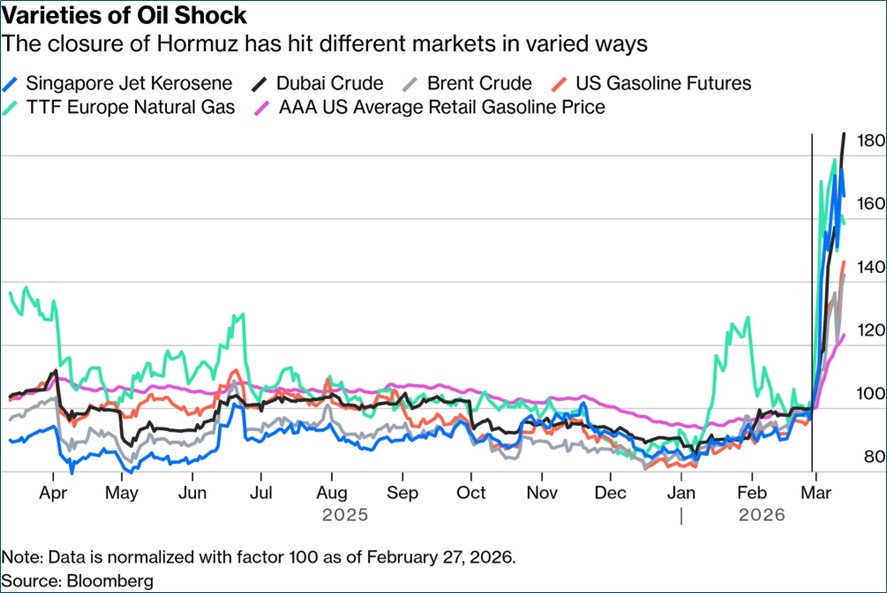

- With rate hikes odds now starting to appear in futures pricing, and the 2yr yielding above the Fed Funds range of 3.50% – 3.75%, the next technical support level sits at 4.00%. While we are hard-pressed to envision a rate hike anytime soon, it does speak to the markets obsession at the moment over the inflationary implications of increased energy costs. As long as the Strait is effectively blocked, energy costs will continue higher and spread further into other aspects of production, some of which are fertilizer, helium, which is critical to semi-conductor production, and ingredients for pharmaceuticals that are more and more manufactured in India.

- That spreading of costs across multiple products will eventually engender demand destruction, and with the consumer already faltering a bit entering 2026 concerns over slowing consumption will begin to enter the trading calculus. That would seem an antidote to higher yields. While Powell was quick to dismiss characterizing our economic situation as stagflationary at last week’s FOMC press conference, the ingredients for such are increasingly being added to the mix.

- As mentioned above, this week is thin on economic reporting which will only make war news even more the driving of trading this week. The few highlights on offer will be the S&P Global Preliminary PMI series for March. While not as famous as the ISM series, it is well regarded and will be the first tell on March activity. The February readings were 51.6 for manufacturing and 51.7 for services. Just like the ISM series 50 represents the dividing line between an expanding sector above and a contracting sector below. So, both were expanding in February but down from earlier levels so this will be a key report due tomorrow morning.

- The other report of note will be the Import/Export Price Index for February. While it’s another report coming before the beginning of war operations, it will provide a benchmark from where those war costs will start to appear when the March report is released. Import prices rose 0.2% in January which pushed the YoY rate to -0.1%. Import prices ex-petroleum were up 0.4% in January. That number will obviously be heading higher in the months ahead.

- The high frequency weekly reports like ADP Pulse due tomorrow and jobless claims on Thursday will add some color to how the labor market is holding up under the uncertainty of a war-time economy. Last week both indicated that hiring continued at a decent pace per ADP and jobless claims remained quiet, indicating layoffs remain muted.

- Finally, I sat down with Joe Keating from our Wealth Management Group last Thursday to talk the Fed meeting and, of course, the implications on the economy from the war with Iran. While events are happening fast, and changing just as fast, you’ll want to listen to our discussion and outlook for the balance of 2026. You can find the discussion here.

Rate Hiking Odds Now Appear for June FOMC Meeting

Source: CME Group

Oil Prices Dip After Trump Announcement of Productive Iranian Talks

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.