Trump Taps Warsh as next Fed Chair

- President Trump announced he is nominating former Fed Governor Kevin Warsh to be the next Fed Chairman when Jerome Powell’s term expires in May. Warsh comes from Wall Street (Morgan Stanley) but sat on the Fed Board from 2006 to 2011 during the depths of the Great Financial Crisis. At that time, I recall Kevin being uncomfortable with rate cuts to support the ailing economy and more concerned with inflation. But that was another time, and another president, so I assume those tendencies are no more. Anyway, we’ll have more to say on Warsh, but with that bit of intrigue settled our attention turns to a possible deal to avoid another government shutdown. This time the impasse is over DHS funding. Democrats say they have secured an agreement from Trump for a two-week DHS funding extension allowing a vote on five other non-controversial spending bills before month end. The Senate needs to approve the deal, and after stalling last night, a vote is expected today. In the meantime, next week brings a host of new January data, headlined by the jobs report on Friday. Hopefully, we’ll have a functioning government to see that the report is released. Currently, the 10yr is yielding 4.24%, up 2bps, while the 2yr is yielding 3.54%, down 1bp on the day.

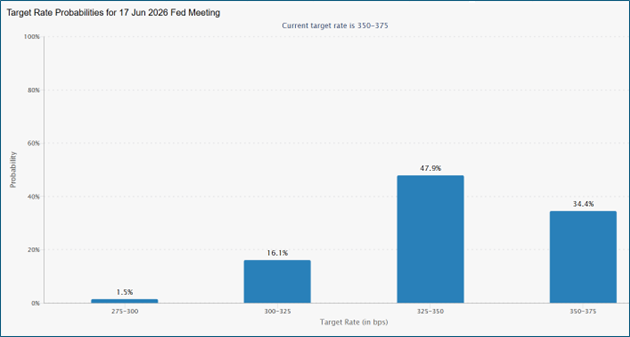

- The Fed delivered an as expected pause on Wednesday, recognizing some stabilization in the labor market (a slightly improved unemployment rate), along with the decent economic growth, but inflation remains elevated. It’s that last point that makes the decision, and Powell commentary, imply the pause may be stickier than a one or two-meeting respite. Despite that slightly more hawkish take, futures see 66% odds for at least a 25bps cut (see bar chart below).

- The other point to consider regarding future meetings is that only two members dissented: Miran and Waller. Miran is a serial dissenter, while Waller is holding out hope for the Fed chair nomination. Even with a newly installed, cut-seeking chair it will take some hefty rhetorical gifts to convince a majority to cut rates in the face of current economic conditions. Of course, conditions can change, but absent a significant deterioration further rate cuts will be quite the lift.

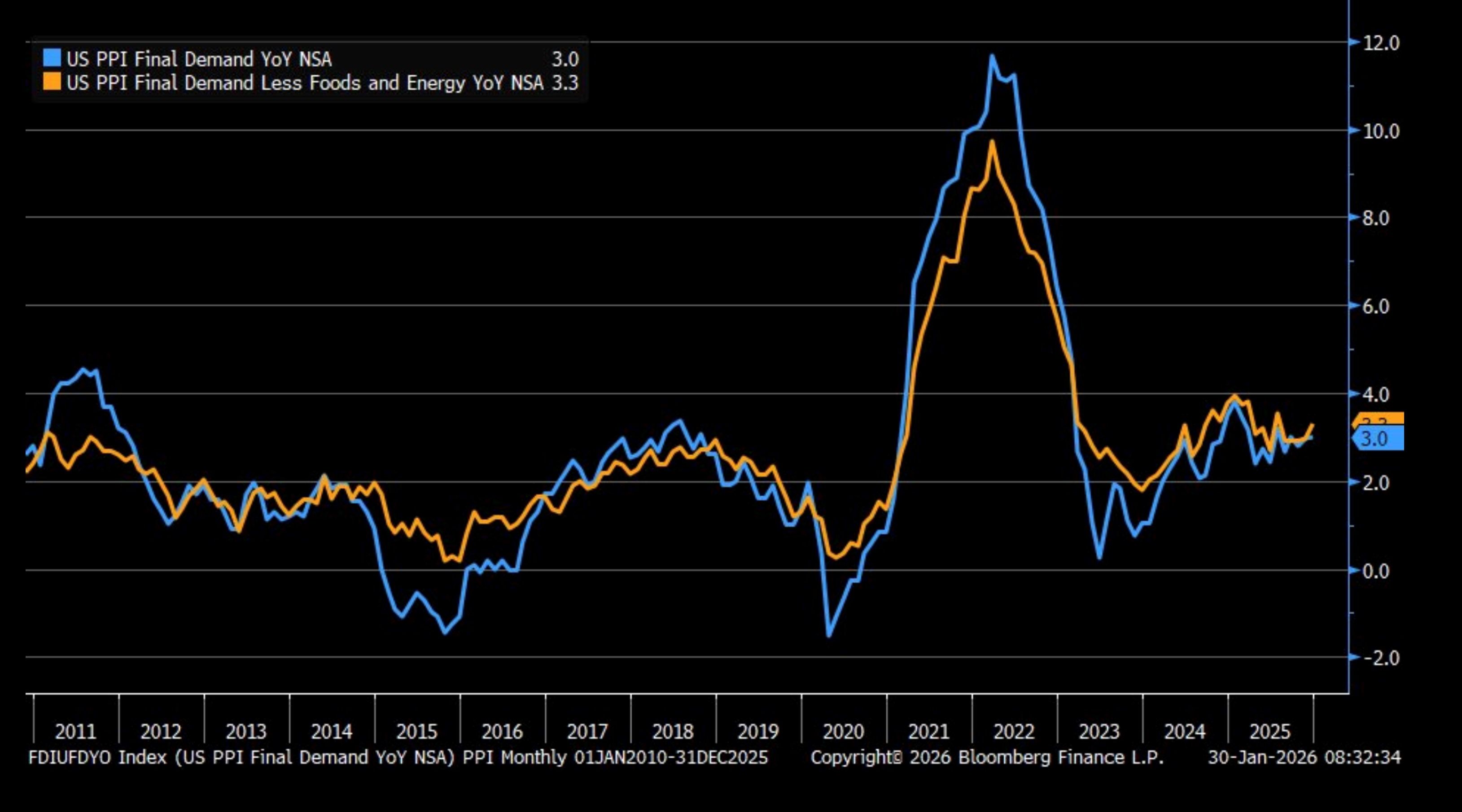

- The last of the meaningful releases this week is out this morning with December PPI. While December CPI was released two weeks ago PPI carries importance as some of the metrics for the Fed’s preferred inflation measure, PCE, are pulled from this report. Headline PPI increased 0.2% MoM, matching expectations with the YoY rate dipping from 3.0% to 2.8%. PPI ex-food and energy also increased 0.2% MoM matching expectations with the YoY rate moving from 3.0% to 2.9%. Specific items, like health insurance and airfares, are two of the more notable items that flow into PCE and for December health insurance increased x.x% and airfares were up x.x%. December PCE is expected to be released on Feb. 20, with current expectations for headline and core at 0.2% MoM and 2.8%YoY for both. The inflation hawks at the FOMC will want to see those YoY levels moving towards 2.0% before another rate cut will be entertained.

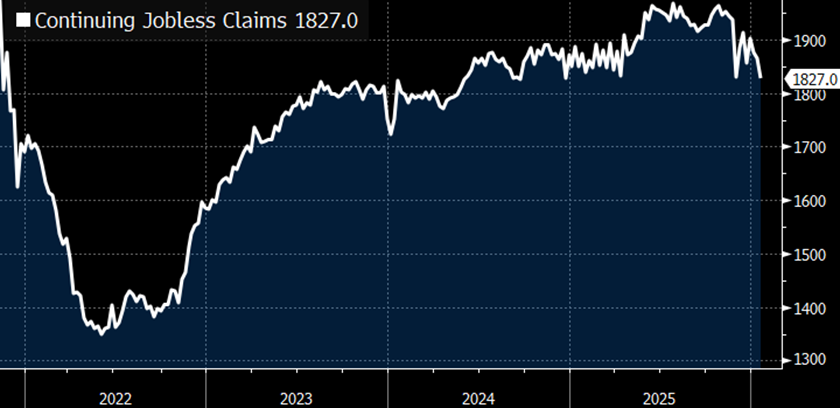

- As for the labor market, the latest weekly jobless claims for January 24 totaled 209,000, a decrease of 1,000 from the previous week’s upwardly revised level. Expectations were for 205.000. The 4-week moving average was 206,250, an increase of 2,250 from the previous week’s average. to 204,000. Continuing Claims registered 1827k in the week of January 17 compared to the 1850k BBG consensus. This is the lowest since September 2024. The prior week was revised up to 1865k from 1849k. Continuing jobless claims decreased 38,000 to 1.827 million for the week ending January 17. This is the lowest level for continuing claims since September 21, 2024, when it was 1,825,000. Thus, the low-hire, low-fire environment persists and plays into the Fed’s desire to pause cuts and wait on further inflation improvement before cutting more.

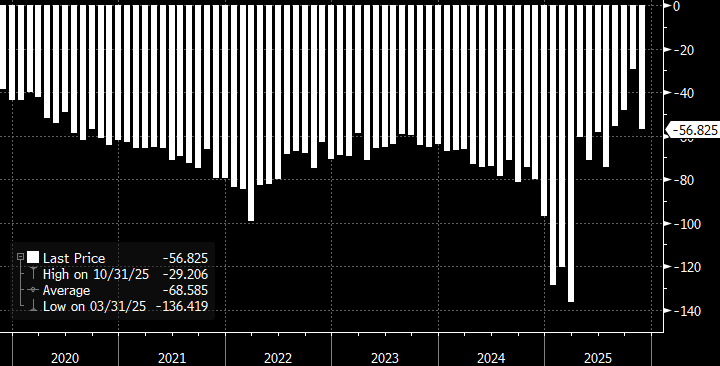

- Finally, the November Trade Deficit widened to -$56.8 billion vs. -$29.2 billion in October and -$44.0 billion expected. This is the widest deficit since July, but the volatility is in keeping with the 2025 theme as market participants adjust purchases based on shifting tariff levels. Exports were down -3.6% MoM vs.+3.0% prior. This is the first time monthly exports have been negative since May. Imports jumped +5.0% MoM vs. -3.0% prior. Imports posted the biggest gain since July with gains in pharmaceuticals and capital goods driving the pick-up.

After Fed Meeting, and Warsh Nomination, Futures Odds See June as Likely Cut Date Source: CME Group

Source: CME Group

December PPI – Hotter Than Expected. Will Weigh on December PCE Source: BLS

Source: BLS

Trade Deficit Widens Again in November as Shifting Tariff Policies/Rates Impact Import Flows Source: Census Bureau

Source: Census Bureau

Continuing Jobless Claims Edging Lower After Peaking in 2025  Source: Dept of Labor

Source: Dept of Labor

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.