Waiting on GDP and PCE

- If you thought after a week that brought you a jobs report, an inflation report, and Retail Sales that this week would be a little less intense, you’re right! Most of what we’ll see this week is second tier and/or somewhat stale and what we do care about will be arriving on Friday. So, market direction, before we see 4th Quarter GDP and December PCE and spending, is likely to come from the equity market more than any shift in economic expectations. Currently, the 10yr is yielding 4.08%, up 2bps, while the 2yr is yielding 3.46%, also up 2bps on the day.

- We’re not quite done with payroll data from January as ADP’s Weekly Pulse Report came in with a decent 10.25 thousand new private sector jobs for the week ending January 31 (moving four-week average). That compares to an upwardly revised 7.75 thousand the prior week and is the highest total since early December (see graph below). The late December/early January weakness in hiring seems to have abated a bit which adds a bit more credence to the BLS January jobs picture that we received last Wednesday and keeps the Fed squarely in pause position.

- Later today we’ll get the minutes from the January FOMC meeting and despite two dissents (Miran and Waller) it’s not likely that the minutes will hold much intrigue. That said, given the lightness in the early week offerings, it will still get some attention when it’s released at 2pm ET. The economic data received since the meeting (namely the jobs and inflation reports) added to the pause case so any commentary in favor of cutting sooner rather than later will get shuffled down in relevance while the hawkish hold talking points will appear prescient.

- This morning, the December preliminary Durable Goods Orders numbers were released with overall orders down -1.4% vs. -2.0% expected. That compares to a 5.4% surge in November orders. Orders ex-transportation rose 0.9% vs. 0.3% expected and 0.4% the prior month. Capital goods orders nondefense ex-air rose 0.6% vs. 0.4% expected and 0.8% in November. Shipments of nondefense ex-air goods rose 0.9% vs. 0.3% expected and 0.2% the prior month. Thus, away from the volatile transportation sector, orders and shipments in December were better than expected and a modest boost from November, another arrow in the quiver for the pause camp.

- The key reports for the week follow tomorrow and Friday. Tomorrow is the Initial Jobless Claims totals and recall last week’s numbers were tame compared to the spike in the prior week. Expectations are for initial claims to tick a bit lower from 227 thousand to 225 thousand with continuing claims nearly unchanged at 1.860 million vs. 1.862 million the prior week. If results come as expected it will continue the low-hire, low-fire trend that’s been in place for the last year.

- On Friday, a pair of reports are the highlight for the week. The first estimate of fourth quarter GDP will be released followed by the December Personal Income and Spending Report. GDP is expected to be solid at 3.0% vs. 4.4% in the third quarter. Personal consumption is expected trend lower to 2.5% vs. 3.5% the prior quarter. Core prices are expected to increase 2.6% vs. 2.9% prior. While the December data from the Personal Income and Spending Report will be a part of GDP, it will give us a feel for trajectories of income, spending, and inflation for December. Core PCE is expected to increase 0.3% for the month with Core PCE YoY at 2.9%. The fact we’ve already received January CPI, means this PCE report will be tainted a bit due to the staleness of the data. The BEA has yet to announce when the January numbers will be released.

- Despite the stale data, we’re also interested in the personal spending numbers due to the earlier weakness of the Retail Sales Report. The spending figures on Friday are more comprehensive than Retail Sales, and inflation-adjusted so it will provide a more fulsome analysis of consumption as we finished the year. With the ongoing volatility in equities, and the possible impact to the wealth effect in the new year, where we left in 2025 is important. Expectations are for spending to increase 0.4% vs. 0.5% in November. Spending net of inflation is expected at 0.1% vs. 0.3% the prior month.

Latest Weekly ADP Shows Highest Job Gains Since Early December

Source: ADP

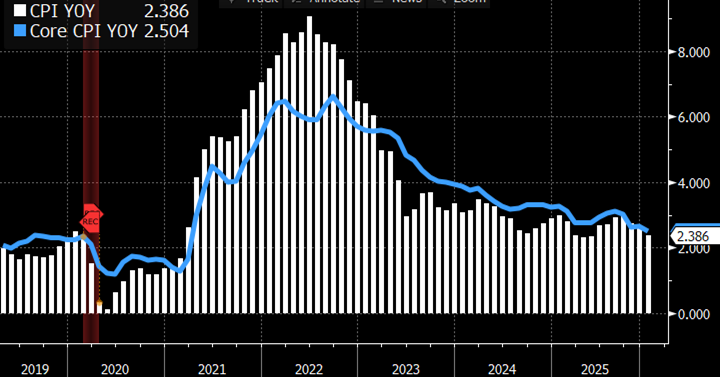

CPI and Core CPI – Well Behaved in January Source: BLS

Source: BLS

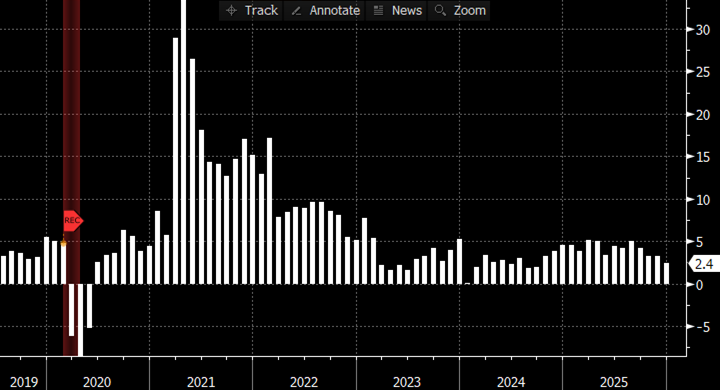

Retail Sales YoY – Trending Lower. Will Personal Spending Trend the Same?

Source: Bloomberg

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.