War Uncertainty Overshadows Inflation News

- Despite a March CPI report on Friday, and February PCE inflation and spending data received on Thursday, war developments drove trading and market sentiment last week, just as it’s likely to do this week. The latest on that front is that President Trump said the US will begin a naval blockade of the Strait of Hormuz—starting at 10 am ET this morning. For its part Iran warned that no port in the Persian Gulf or the Sea of Oman is safe. This comes after talks with Iran in Islamabad ended without progress on issues including Tehran’s nuclear program and control of the waterway. Oil has predictably moved higher with WTI up $7.50 to $104 in early trading. So that’s where things stand as we prepare for yet another week in parsing out when peace may break out in the Middle East, and when traffic will resume flowing in the Strait of Hormuz. Currently, the 10yr is yielding 4.36%, up 4bps on the day, while the 2yr is yielding 3.84% up 3bps on the day.

- As mentioned above, on Friday we received the March CPI data that saw the headline measure surge 0.9% after rising 0.3% in February. Over the last 12 months, the headline index increased 3.3%. In February, the YoY rate was 2.4%. In March, the energy sector rose 10.9%, led by a 21.2% increase for gasoline which accounted for nearly ¾ of the monthly increase in the headline measure. Meanwhile, the core index (all items less food and energy) rose a more docile 0.2% and the YoY pace ticked up a tenth to 2.6%.

- Thus, the inflation move in March was essentially all about the impact of the war on energy costs, specifically gasoline. That relatively isolated impact will spread this month. Expect higher prices for items like food, transportation, fertilizer, and all the other ancillary items that we’ve been hearing about as traffic from the Strait continues to be nearly shut off and the stocks of existing, lower cost, inventory become depleted.

- On that last point, we managed to catch part of the quarterly call from WD40 executives last week where they mentioned their petroleum distillate stockpile would last another quarter or so, then the full impact of restocking at current prices would force either margin compression and/or higher prices for consumers. They speculated that by the fall they would be forced to adjust retail prices higher. A similar story is probably being told/felt across thousands of companies such that the limited price pressure away from energy in March is most likely just the precursor to a series of waves that hit consumers. We can only hope it’s of the softer tariff-like impact, but hope is not a great strategy.

- This week includes more inflation figures with tomorrow’s March PPI Report. Much like the CPI series from last Friday, big jumps in energy-related measures are likely with more in the proverbial pipeline. The wholesale price report will provide analysts with most of the remaining pieces to put together a reasonable PCE inflation estimate with that report due near the end of April. Recall, PCE was already running hotter than CPI (core PCE +0.39% Jan., 0.37% Feb.), so the added impact of higher energy prices will push PCE uncomfortably higher.

- Again, this is not to say the market will be greatly moved by this week’s limited slate of inflation data any more than it was on Friday by the headline leading CPI. It just underlines the degree to which war news has and will continue to be the driving force in trading, and the longer energy prices remain elevated and shipping flows restricted inflation pressure will force itself further into the global economy.

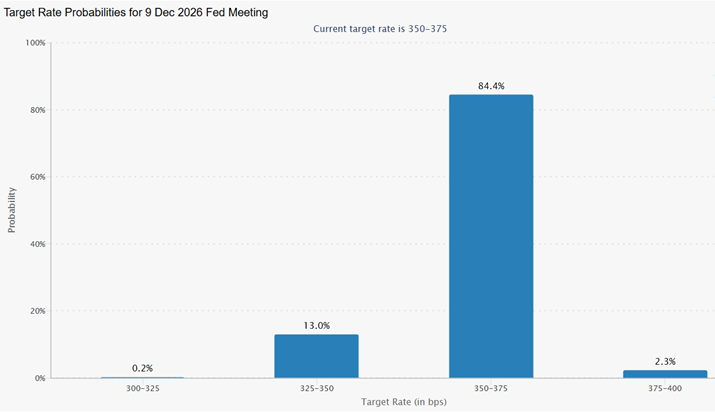

- As uncertainty reigns supreme now, the latest news from the Middle East has hardened futures expectations towards a no-cut-this-year outlook. Below is the December outlook for Fed Funds with a clear majority at 84% pricing no rate move at all this year with small tail risks for either a cut or a hike.

- Thus, until the Iran war is resolved and shipping returns to some type of pre-March normalcy, markets are increasingly expecting no action from the Fed this year. That is probably a safe bet as long as a peace deal remains elusive and shipping remains restricted. What’s more assured, however, the longer this does drag on, higher prices and further erosion in consumer sentiment may finally result in demand destruction resulting in another leg lower for the economy.

Futures See No Rate Cut This Year as Greatest

Source: CME Group

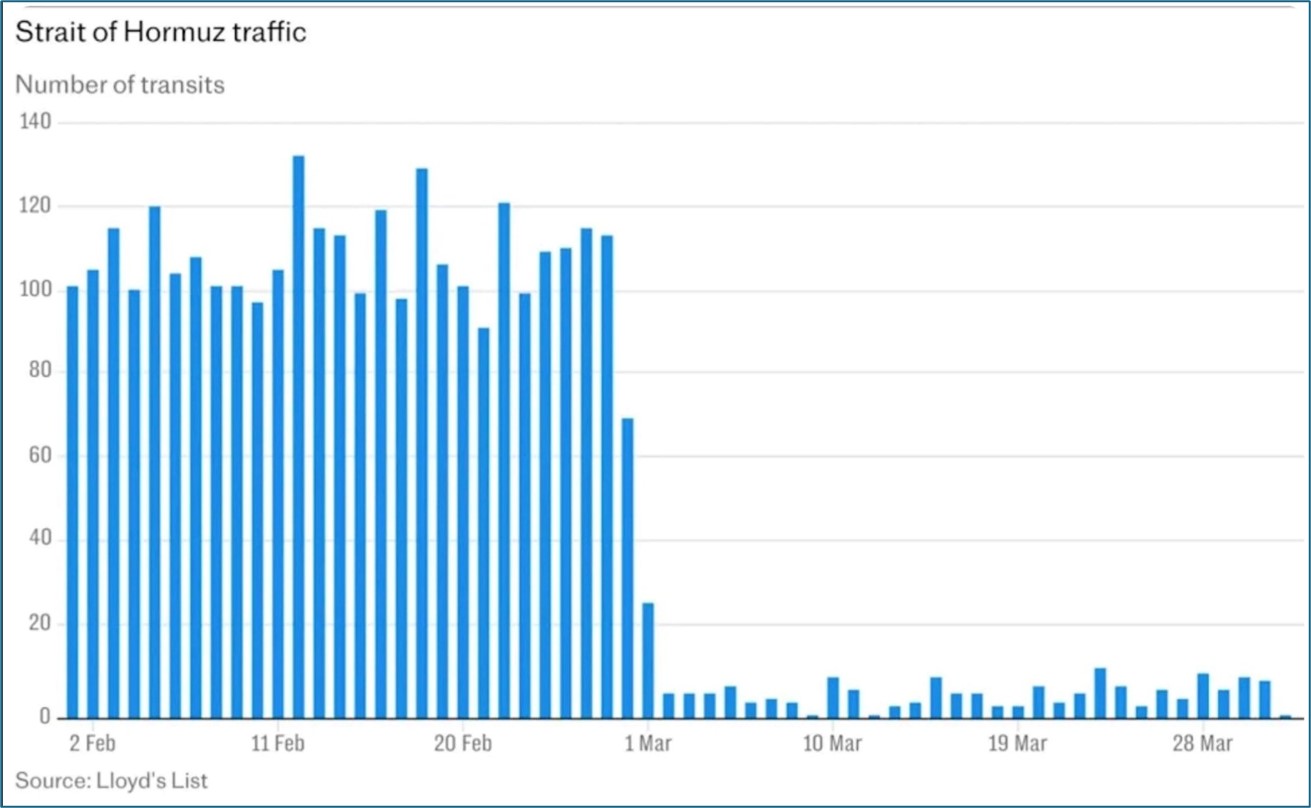

Hormuz Shipping Traffic Remains Mostly Non-Existent

Securities offered through the SouthState | DuncanWilliams 1) are not FDIC insured, 2) not guaranteed by any bank, and 3) may lose value including a possible loss of principal invested. SouthState | DuncanWilliams does not provide legal or tax advice. Recipients should consult with their own legal or tax professionals prior to making any decision with a legal or tax consequence. The information contained in the summary was obtained from various sources that SouthState | DuncanWilliams believes to be reliable, but we do not guarantee its accuracy or completeness. The information contained in the summary speaks only to the dates shown and is subject to change with notice. This summary is for informational purposes only and is not intended to provide a recommendation with respect to any security. In addition, this summary does not take into account the financial position or investment objectives of any specific investor. This is not an offer to sell or buy any securities product, nor should it be construed as investment advice or investment recommendations.